Items that may only interest or educate me ….

TINA meet TARA, Latest US CPI numbers, a golden triangle has appeared…

A new acronym makes its way into the investing world, likely at the expense of another acronym. Following the financial crisis of 2008, central banks lowered the cost to borrow money (interest rates) to restore confidence in the stock markets. With extremely low interest rates and easy access to money, the share prices of public companies took off because the return on bonds and other investments was minimal, leading to the acronym TINA – There Is No Alternative. Investing in stocks was the only way to make any money through investing.

The TINA investing style had a good run until it ran into the high inflation of 2022. As the central banks, such as the Bank of Canada (BoC) and the US Federal Reserve (Fed), battled inflation by raising their respective benchmark interest rates, the pay back on government bonds has once again become a viable alternative. In the US, bonds have seen a net inflow for the last few weeks. While I was unable to find similar data for Canadian based bonds, I suspect it is a comparable situation here in Canada. One option I discovered was TD Market Growth GICs. These GICs (Guaranteed Investment Certificate) provide a minimum 3% and up to a maximum 30% return, for a 3- or 5-year investment, with minimal risk.

As bonds, GICs, and other investment options returned to favour, a new acronym was born – TARA. There is A Reasonable Alternative. I have never been big on bonds or GICs, but with a guaranteed 3% return and the possibility of up to 30% over 3 – 5 years and minimal risk, these are a reasonable alternative. I would have liked to have one of these for 2022. 😊

The December US Consumer Price Index (CPI) came out this past Thursday, meeting analysts’ expectations but not providing many clues on the size of the next increase to the US benchmark interest rate. The US Department of Labor’s December CPI report showed inflation increased 6.5% (analysts expected 6.5%) from December 2021. The good news was the inflation rate was down from 7.1% in November, 2022.

The Core CPI data (CPI less food and fuel prices) showed inflation was 5.7% higher than in December 2021. The data also showed prices had inched higher by 0.3% from November’s Core CPI rate. Not good news, but not bad news as this was what analysts had forecast.

Since the Fed said future changes to the interest rate would be data driven, this mixed information (compared to the previous month, CPI was lower, while the core-CPI was slightly higher) does not provide many clues to the size of the next increase. And yes, there will be an increase. The debate is whether it will be 0.25% or 0.5%. Together, the CPI and Core CPI would indicate the Fed’s series of interest rate hikes has slowed, if not lowered the rate of inflation.

The other bit of news from a separate Department of Labor jobs report was the data showed the jobs market remained strong but the pace of jobs growth has slowed down from the same period in 2021. As well, wage growth continues but at a slower pace.

Judging by the deceleration of inflation, increasing employment levels, and slowing wage growth, the Fed just might thread the needle and lower inflation without damaging the economy.

Before getting too excited, keep in mind the Fed has repeatedly stressed it will keep raising interest rates to bring inflation back down to its 2% target.

On Friday, the TSX triggered a ‘golden cross.’ In the investing world, this is a very good sign. It is a technical indicator of a major trend change indicating an upward trend, or bull market, is coming. In the chart below, on the far right you can see the red 50-day simple moving average line (SMA (50D)) nudged above the grey 200-day simple moving average line (SMA (200D)). The 50-day SMA was 19,849.17 and the 200-day SMA was slightly lower at 19,839.25. That is not much lower, but it is lower. 😊

The red and green vertical bars are the daily closing prices of the TSX. Green bars indicate the market closed higher and the red bars indicate the market ended lower.

While ‘golden cross’ is a good technical signal, it has a cousin known as the ‘death cross.’ As the name implies, it is not a good sign. On the same chart above, you can see the TSX experienced a ‘death cross’ on June 8, 2022. On that day, the red 50-day SMA line dropped below the grey 200-day SMA line.

Let us not worry about the ‘death cross,’ instead, focus on the ‘golden cross’ signifying the start of a bull market for the TSX. The DJIA had its own ‘golden cross’ on December 14, 2022. The S&P is not far away from its own ‘golden cross,’ but the Nasdaq has a long way to go before the 50-day SMA rises above the 200-day SMA.

Two golden crosses and a third one not far away. Not a bad start to 2023. 😊

With the golden cross to lead the way, let’s take a look at the past week…

Weekly Market Review

Monday: The markets got off to a hot start today before fizzling out on news the US Federal Reserve (Fed) suggested the US benchmark interest rates could rise above 5%. At the end of the day, the Toronto Stock Exchange Composite Index (TSX) and the Nasdaq Composite Index (Nasdaq) were able to remain above water while the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA) ended lower.

In Canada, the TSX ended the day at its highest point in four weeks thanks to the Canadian Technology and Energy sectors. Weighing down the TSX were the Canadian Consumer Cyclicals and Telecommunications Services.

In the US, early momentum gave way to ongoing concerns about inflation. Investors are waiting to hear from Fed chair Jerome Powell, who will be part of a panel discussing central bank independence, on Tuesday. Analysts and investors are hoping to gain insights into the Fed’s plan to fight inflation going forward. In trading, the best performing American S&P sectors were the interest rate sensitive Technology and Consumer Cyclicals. The biggest losers were Healthcare and Consumer Staples.

Tuesday: It was a mixed day in the markets as all indexes fell early but all four were able to climb out of the early hole to end the day in positive territory. Oil prices advanced when the US government predicted record global consumption in 2024. In Canada, The TSX was pulled higher by rising gold prices that caused the Canadian Basic Materials sector (mining companies and fertilizer manufacturers) to be the best performing sector for the day. The Utilities and Consumer Staples sectors were the worst performers of the Canadian sectors, holding the TSX back.

In the US, Fed Chair Jerome Powell spoke in his first public appearance of 2023 but avoided any comments about the Fed’s rate policy. In a case of no news is good news, optimistic investors responded favourably, turning all three American indexes green. In the market, it was almost a perfect day for the S&P sectors as only the Consumer Staples sector failed to post a gain. Leading the American indexes higher were the Basic Materials (on gold) and Consumer Cyclicals.

Wednesday: All for major North American Indexes ended the day higher as investors await tomorrow’s key US Consumer Price Index (CPI) report. Investors were optimistic the CPI data would indicate inflation was falling, allowing for the Fed to make a smaller interest rate increase. The price of oil rose on an improved global economic forecast, lifting the Energy sectors in both Canada and the USA.

In Canada, higher oil and gold prices helped lift the TSX higher. Leading the charge upward were the Canadian Utilities and Consumer Cyclicals sectors. The Basic Materials sectors slumped as investors took money off the table after a recent rally in the price of gold. The only other Canadian sector to end the day lower was the Consumer Staples sector.

In the US, investors jumped back on the growth companies’ bandwagon today, as the growth-oriented Consumer Cyclicals and Technology sectors helped lift all three indexes. The only S&P sector to slide down was the Telecommunications sector.

Thursday: Data from the US CPI report suggested inflation was on a downward trend, sending all four indexes higher. The statistics showed inflation had dropped since the November report, but the Core CPI number rose slightly. With the mixed, but generally positive news, investors were optimistic the numbers supported the case for a 0.25% increase rather than 0.5% hike, causing the markets to rise.

In Canada, the TSX rode the news coming out of the US, higher oil, and higher gold prices to end the day firmly in the green. The continuing rise in oil and gold prices helped the Canadian Energy and Basic Materials sectors outperform the rest of the Canadian sectors. The only Canadian sectors to end lower were the Consumer Cyclicals, Utilities, and Industrials sectors.

In the US, the CPI data showed the December consumer prices fell for the first time in over two years. The belief in a 0.25% interest rate increase, along with rising oil prices pushed all three American indexes to extend their winning streaks for another day. In trading, Energy and Telecommunications Services led a strong showing from the American S&P sectors. The Consumer Staples and Utilities were the only S&P sectors to end the day lower.

Friday: All four indexes inched higher today on investor optimism after Thursday’s CPI numbers suggested inflation had started trending downward. Concerns about upcoming earnings reports limited today’s gains.

In Canada, strong gold and other commodities’ prices continue to lift the share prices of the companies found in the Basic Materials sector. In trading, the best performing Canadian sectors were Technology and Industrials, while Consumer Cyclicals was the only sector to end lower.

In the US it was the start of earnings seasons. Leading off were the big American banks that performed well considering the challenges of 2022. Amazon (NASD:AMZN) rose 3% today to close off a good week that saw the company gain 14% for the week, its best since April 2020. In the market, riding the coattails of the big banks, the S&P Financials sector led the way, followed by the Technology sector. The only company to fall back was the Utilities sector.

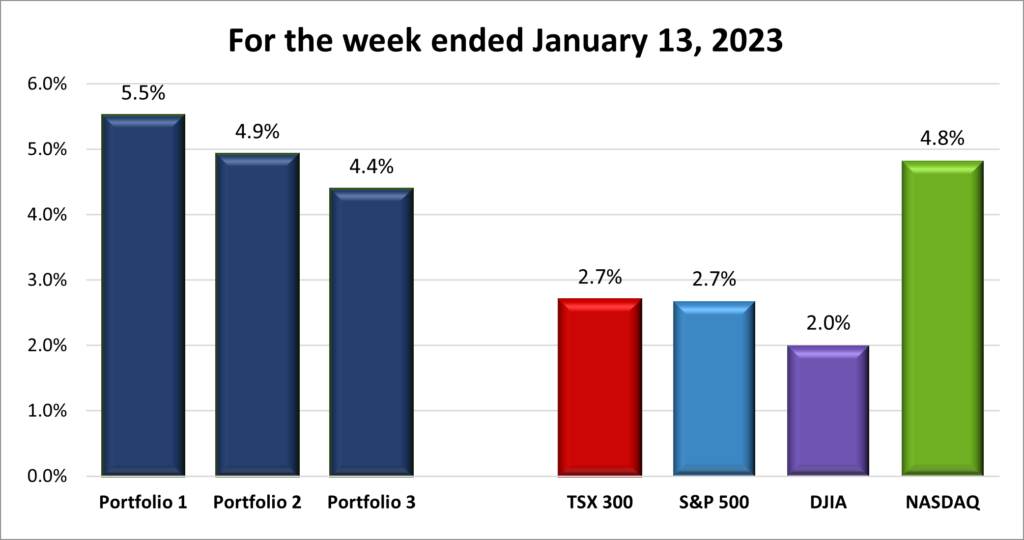

For a second consecutive week all four major North American indexes ended the week higher. For the week, the TSX rose 2.7%, the S&P 500 gained 2.7%, the Dow advanced 2.0% and the Nasdaq jumped 4.8%.

Weekly Portfolio Review

![]()

So far 2023 has been surprisingly good in the North American stock markets, although there are still 50 weeks to go. 😊 Other than the CPI report there was not a lot of news to move the market one way or the other. The CPI report itself was slightly positive, but investors took the decline in inflation as a sign the Fed would be less aggressive with the upcoming interest rate hike. Oil and gold prices continued to rise, lifting the TSX. In the US, as well as oil and gold moving higher, investors moved back into the big, well known technology companies, lifting the Nasdaq and S&P. The DJIA with its thirty big blue-chip companies rode investor optimism to end the week higher as well.

When the rising tide lifts the markets, it lifts all three portfolios. As shown in the chart below, both Portfolio 2 and 3 gained over 4%. Portfolio 2 was propelled upward by great a week from Microsoft (NASD:MSFT) and MongoDB (NASD:MDB), while Portfolio 3 had a solid week all around, with strong performances from Microsoft and the financial companies. With Portfolio 2 & 3 gaining 4% this past week, my first though was what held Portfolio 1 back. In general Portfolio 1 was in line with the gains of the TSX, the S&P and the DJIA. There were no big losers, with many of the companies ending the week higher. And that is fine.

This was a good week but there is a long way to go to get back to where the portfolios were at this time last year. A long way to go.

Companies on the Radar

A few changes to the Radar List this week. First, SmartCentres (TSX:SRU.UN) moves off but remains on the periphery if a defensive company is needed. There is nothing wrong with the company and if there were not already REITs in the Portfolios this would be a strong candidate.

Next, Alvopetro (TSXV:ALV) moves off the list and into Portfolio 3 thanks to a brief drop in the share price. I had a low bid in place and when the share price dropped the order was filled.

Finally, two new companies popped onto the Radar List this past week – DoubleVerify (NYSE:DV) and Griffon Corporation (NYSE:GFF). DoubleVerify is a US based company that helps the world’s largest brands maximize and optimize the effectiveness of their online advertising. While the company did not have the greatest score in the Ratings sections (the first image below), it did very well on the High-Level Financials section (the second image, below). The only negative was that it is share price did not beat the S&P index over five years and that comes with an asterisk since the company went public in April 2021, making it impossible to compare it over five years. 😊 Very few companies put up green across the High-Level Financials section, so I will take a closer look at DoubleVerify.

The other company, Griffon Corporation, is a US based company that provides home building products to consumers and professionals throughout the world. Griffon scored slightly higher than DoubleVerify in the Ratings section but had a lot of red in the High-Level Financials sections, including the Net Income and Long-Term Debt sections. If I learned nothing else in 2022, I learned the importance of companies being Net Income positive and having very little debt. With that in mind, I am not interested in looking further into Griffon.

As well as DoubleVerify and Griffon Corporation, the Radar List included:

- Crew Energy (TSX:CR): A Canadian oil and gas company with interests in British Columbia.

- International Petroleum (TSX:IPCO): A Canadian company with oil and gas assets in Canada, Malaysia, and France.

- Alphabet (NASD:GOOGL): The leading online search engine and advertising company, dominant mobile operating system.

The Radar Check was last updated January 13, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended January 13, 2023: UP ![]()

- Finally, some good news for Tesla (NASD:TSLA) investors. Tesla reported longer wait times in China for its long-range versions of its Model Y vehicle, suggesting its price cuts in China were leading to increased demand. Now to see longer wait times for all models, in all markets. 😊

It worked well in China, so why not globally? Tesla cut prices globally by up to 20% on its vehicles, sacrificing profits to maintain the company’s growth rate. While lower prices did not help Tesla’s share price, it did cause the share prices of its competitors to tumble. General Motors (NYSE:GM) and Rivian (NASD:RIVN) saw their respective share prices fall. The lone exception was Ferrari (NYSE:RACE) which continued its upward trajectory. - To increase its presence in the US, Nuvei, (TSX:NVEI) acquired US based Paya for US$ 1.3 billion. The market reacted favourably to this acquisition.

- Amazon took aim at Shopify’s (NASD:SHOP) ‘Shopify Pay’ service with the roll out of Amazon’s ‘Pay with Prime.’ The service will allow online merchants outside the Amazon ecosystem to use Amazon’s payment and delivery services. The service will be available in the US near the end of January. No word when ‘Pay with Prime’ will be available to Canadian online merchants. Good for Amazon, not so good for Shopify.

- Home Depot (NYSE:HD) is changing its hourly wages policy to pay employees to the nearest minute. In the past, the company rounded up or down to the nearest 15 minutes. Home Depot was facing a lawsuit that the company was purposely rounding down employee wages. This change to their hourly compensation policy makes sense and will prevent future concerns of rounding down to the nearest quarter hour. I do not know why they did not do this sooner. Even if it all worked out over time, I can see employees feeling they were being shortchanged.

- Good news for Trisura (TSX:TSU) as they received two ‘Excellent’ ratings from the AM Best credit rating agency. The ratings reflect Trisura’s very strong Balance Sheet and the company’s “adequate operating performance, neutral business profile and appropriate enterprise risk management.”

- Porsche Automobile (OTC:POAHY) is evaluating fully integrating Google (NASD:GOOGL) software into the cockpit of their vehicles. The integration would allow Porsche drivers to access Google Maps and Google Assistant without going through their smartphones.

- Algonquin Power & Utilities Corp (TSX:AQN) saw its share price almost cut in half after it announced it reduced its dividend by 40%. Not only was the dividend significantly reduced but the dividend re-investment plan was suspended. Algonquin’s share price originally fell on troublesome earnings news in November. The earnings report showed the higher interest rates had taken a toll on the company’s cash flow as more cash was required to service their high level of debt.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX:DIR.UN)

US $

Innovative Industrial Properties Inc (NYSE:IIPR)

Quarterly Reports

Shaw Communications Inc.

All currency listed in millions of Canadian dollars, except per share amounts

Selected highlights from their first quarter 2023 financial results on January 12, 2023

- Revenue of $1,370 for the three months ended November 30, compared to $1,386 for the same period in 2021. A decrease of over 1%.

- Net income of $168 for the three months ended November 30, compared to net income of $196 in the same period in 2021.

- Diluted earnings per ordinary share of $0.34 for the three months ended November 30, compared to $0.39 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended January 13, 2023: UP ![]()

- Guardant Health (NASD:GH) announced preliminary fourth quarter results that not only beat analysts’ estimates for revenue, but it also had US$ 1 billion of cash and cash equivalents.

- Walt Disney Corporation (NYSE:DIS) is facing a challenge to Disney’s Board of Directors leadership group. Activist investor Nelson Peltz is seeking a seat on Disney’s Board to ‘rescue’ Disney from overspending on their streaming business (Disney+), and to help with succession planning amongst other things. It will be an interesting challenge for recently returned CEO Bob Iger.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Telus Corp (TSX:T) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended January 13, 2023: UP ![]()

- Cloudflare (NYSE:NET) added several new email security solutions that can protect employees from phishing, malware, and other security attacks. These new features will enhance Cloudflare’s Zero Trust security platform that protects organizations from cyberattacks.

- Viemed Healthcare (TSX:VMD), a technology-enabled home medical equipment services provider, has partnered with ModoHealth to enhance ModoHelath’s patient management network. ModoHealth will receive a C$ 2-million-dollar investment from Viemed. In exchange, Viemed will be able to utilize Modohealth’s software platform to monitor and improve Viemed’s patients’ results.

Activity

Bought Alvopetro Energy. This is the second purchase of Alvopetro shares. Over the last three years, the company has grown revenue, net income, and earnings per share. They continue to pay down debt, eliminating more than 40% of long-term debt. Finally, the dividend has grown by almost 60% since my original investment in June 2022.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

TD U.S. Equity Index ETF (TSX:TPU)

Alvopetro Energy Ltd (TSXV:ALV)

Brookfield Corp (TSX:BN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.