Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Central banks elsewhere, Electric vehicle charging gets a jolt, ….

Canadian Economic news

Bank of Canada meeting minutes

The minutes from the Bank of Canada’s (BoC) last meeting provided insights into their decision-making process regarding the latest increase to the benchmark interest rate. While there was consideration given to delaying a rate increase, the BoC ultimately decided that raising the rate was necessary to prevent inflation from stalling and continuing to trend downward. They were also prepared to implement further rate increases if deemed necessary.

The BoC was concerned about the ongoing strong demand in the economy and the high level of core inflation, which is measured by the core Consumer Price Index (CPI), which excludes the volatile food and fuel components from the overall CPI. To address this situation, the central bank decided to increase the interest rate, aiming to slow down demand and bring core inflation to a more manageable level.

The minutes revealed the BoC’s future decisions regarding interest rates will be based on an assessment of incoming economic data and the outlook for inflation.

Based on current projections and unless there are unforeseen events, analysts expect the BoC to maintain the benchmark rate at 5.0% for the remainder of the year, as inflation remains at the upper end of the BoC’s target range of 1% to 3%. However, they anticipate a rate cut sometime in the first quarter of 2024 as inflation is expected to moderate.

Gross Domestic product

According to the latest report on Gross Domestic Product (GDP) from Statistics Canada, the Canadian economy showed signs of growth in May. GDP increased by 0.3% during that month, following a 0.1% growth in April. On an annual basis, the GDP for May indicated a positive trend with a 1.9% increase.

In May, certain subsectors experienced notable rebounds. Wholesale trade and public administration subsectors saw significant growth, with the latter attributed to the return of government employees to work.

However, the oil and gas extraction (except oil sands) subsector faced challenges in May, experiencing a substantial decline of 6.6%. This drop was primarily a consequence of forest fires in Alberta, which led to the shutdown of many wells.

Despite the growth in May, early data for June suggests a decrease of 0.2% in real GDP, signaling a potential contraction in the economy for that month.

Looking ahead, analysts predict that the Canadian economy could continue to experience a back-and-forth pattern between growth and contraction for the remainder of 2023. This kind of oscillation may lead to slow overall growth during this period.

US Economic news

The good news is that the bear market that affected the S&P 500 in 2022 has been nearly erased, and investors continue to drive the markets higher. However, the Federal Reserve (Fed) remains concerned about inflation, a concern that has persisted since the start of the bear market.

The Fed raises the rate

In response to these inflation concerns, the Fed’s Federal Open Market Committee (FOMC) raised its benchmark overnight interest rate by 0.25% to the 5.25%-5.50% range. This marked the eleventh increase in the last twelve FOMC meetings and brought borrowing costs to their highest level since January 2001.

Equally significant were the comments made by Fed Chair Jerome Powell during the press conference that followed the FOMC meeting. Mr. Powell and the Fed members felt that the economy was still too strong, and the labor market needed to soften. He stated that reducing inflation would likely require a period of slower growth and some softening in labor market conditions. However, he also noted that future decisions on rate increases would be data dependent and made on a meeting-by-meeting basis, and the impact of rate hikes on the economy. He said no decision had been made regarding a rate increase at their next meeting in September but a rate cut is highly unlikely in 2023.

I hope that this latest rate increase will be the last for a while, even though the Fed continues to stress the importance of seeing inflation continue to decline. Tough talk from the central bank is essential to maintain control over inflationary pressures, as it signals their commitment to addressing the issue. If they were to ease their stance, it could risk reigniting inflationary pressures.

Economic news

The Gross Domestic Product (GDP) for the second quarter demonstrated a positive growth trajectory, increasing at an annualized pace of 2.4%, surpassing both the previous quarter’s 2.0% and analysts’ expectations of 1.8%. This indicates that the world’s largest economy continues to show resilience and strength, with the threat of a recession fading.

Additionally, there were promising signs in the job market, with the Department of Labor reporting the lowest number of jobless claims since February. Only 221,000 people filed jobless claims for the week ending July 22, reflecting a positive trend in the labor market.

On the inflation front, the Fed’s preferred measure, the Personal Consumption Expenditures (PCE) price index for June increased by 0.2%, up from the 0.1% rise in May. The Core PCE, which excludes volatile food and energy components, also rose by 0.2%. With PCE rising 3.0% and Core PCE rising 4.1% on an annual basis, these numbers indicate a slight rise in inflation. For core PCE, the rise was the lowest increase since September 2021.

However, there are some encouraging signs from consumer sentiment data. The University of Michigan’s final Consumer Sentiment Index (CSI) for July showed a reading of 71.6, slightly below the initial reading of 72.6 but still significantly higher than the readings from the previous month and the same period in 2022. Similarly, the Conference Board’s consumer confidence index reached its highest level in two years, with a reading of 117 in July, up from 110.1 in June. Consumers are feeling more optimistic, likely due to a combination of falling inflation and a robust labor market.

While the positive consumer sentiment is great news for economic growth, it also brings up concerns about the potential impact on inflation. If consumers continue to spend and inflation remains above the Fed’s 2% target, the possibility remains that the Fed could raise interest rates again to control inflation and bring it down to the desired level.

Overall, the data paints a positive picture of the American economy, with strong growth, an improving job market, and upbeat consumer sentiment. More data like this could bring an end to the Fed’s interest rate increases. 😊

Central banks elsewhere

In the event you thought the inflation fight was limited to Canada and the Unites States, here are the latest actions by other central banks:

- The Reserve Bank of New Zealand raised its benchmark rate to 5.5% in May, the highest level in 14 years. The bank has been raising rates since October 2021, and analysts believe this is the end of their tightening cycle.

- Australia’s central bank held its key rate at 4.1% in July, the highest level in 11 years. The bank is expected to continue raising rates in the coming months.

- The European Central Bank (ECB) raised its benchmark rate by 0.25% to 3.75% in July, its highest level since 2000. The ECB is expected to raise rates again in September.

- Great Britain’s Bank of England is expected to raise rates at its next meeting on August 3.

- Norway’s Norges Bank raised its benchmark rate by 0.5% to 3.75% in June, a 15-year high. The bank is expected to raise rates again in August.

- Sweden’s Riksbank boosted its interest rate by 0.25% to 3.75% in June and are expected to increase it by another 0.25% in September.

- Switzerland’s Swiss National Bank boosted their key rate to by 0.25% to 1.75% in June. It was the fifth consecutive increase since June 2022 when it was -0.75%. Analysts are divided whether the central bank will increase or lower the rate by 0.25% at their next session in September.

- Japan’s central bank, the Bank of Japan, kept its benchmark interest rate unchanged at -0.1% but announced it would let long term interest rates rise. For years Japan had kept its benchmark interest rate at extremely low levels to stimulate the Japanese economy.

As you can see, central banks around the world are taking aggressive action to lower inflation, but it remains to be seen whether they will be able to bring inflation under control. The global economy continues to face a number of challenges, including the war in Ukraine and supply chain disruptions, which could make it more difficult for central banks to bring inflation down.

Only time will tell whether the central banks’ efforts will be successful. However, they are committed to taking action to beat inflation and protect the global economy.

Electric vehicle charging gets a jolt

The competition in the electric vehicle (EV) charging network space is heating up as a consortium of major EV manufacturers, including BMW (OTCM: BMWYY), GM (NYSE: GM), Honda (NYSE: HMC), Hyundai and Kia (OTCM: HYMTF), Mercedes Benz (OTCM: MBGYY), and Stellantis (NYSE: STLA), have joined forces to create their own charging network. This consortium aims to build a massive network of fast chargers in Canada and the US, capitalizing on government subsidies.

Their ambitious plan is to deploy 30,000 fast chargers across both countries by 2030. They said they will provide charging options for both Tesla’s (NASD: TSLA) supercharger standard and the new North American standard charger. By doing so, they aim to provide greater accessibility and convenience for EV drivers, regardless of their vehicle brand.

This move would have a significant impact on the EV charging landscape, as it brings together major players in the automotive industry, pooling their resources and expertise. As the EV market continues to grow, having a robust and widely accessible charging network will be crucial to support the widespread adoption of electric vehicles and address the issue of range anxiety for potential buyers.

Tesla’s supercharger network has been a key advantage for the company, but with this new consortium’s efforts, there might be increased competition and pressure to improve charging infrastructure across the board. Ultimately, this development will benefit consumers by expanding charging options and promoting the transition to cleaner and more sustainable transportation.

After a busy week of economic data, let’s see what happened this past week….

Weekly Market Review

Monday: The start of a busy week for the North Americans markets ended on a positive note with all four indexes ending in the green. This week the Fed announces their latest decision on US interest rates and many of the big technology companies present their second quarter earnings.

In Canada, the Toronto Stock Exchange Composite Index (TSX) gained on higher oil prices as result of higher demand and tightening supplies. While not as exciting as earnings announcement from the big US technology companies, many big Canadian companies will report their second quarter results later this week. In trading, Energy and Consumer Cyclicals were the best Canadian sectors while Utilities and Telecommunications Services had the biggest declines.

In the US, the Dow Jones Industrial Average (DJIA) notched its eleventh straight positive day, its longest winning streak in six years. Meanwhile the S&P 500 Index (S&P) and the Nasdaq Composite Index (Nasdaq) got back into the win column as investors start to expand into other sectors besides technology. In trading, Energy and Financials were the big winners, while Healthcare and Utilities were the only sectors to end lower.

Tuesday: The three American indexes edged upward while the TSX edged slightly down as investors await the Fed’s decision on the US interest rate. Investors were also waiting for Alphabet’s (NASD: GOOGL) and Microsoft’s (NASD: MSFT) second quarter earnings reports that came out after the markets closed. It will be interesting to see how artificial intelligence (AI) impacts these companies top (sales) and bottom (earnings) lines and if it will offset slumps in their respective cloud businesses.

In Canada, an announcement by the Chinese government that would prop up their economy sent the share prices of many of Canada’s big mining companies higher. However, it was not enough to overcome a downdraft in the Canadian Financials sector. Accordingly, Basic Materials (mining companies and fertilizer manufacturers) was the best performing Canadian sector by a full percentage point, while Telecommunications Services and Financials were the worst performers.

In the US, the DJIA streak stands at twelve and the Nasdaq regained its swagger thanks to gains in Alphabet and Microsoft ahead of their earnings reports. In trading, Basic Materials and Technology were the top gainers, while Financials and Consumer Cyclicals experienced the biggest drops.

Wednesday: The markets yawned after the Fed did as expected, raising the US interest rate 0.25% to 5.5%, ending essentially flat. Investors were more focused on the post session comments indicating no decision had been made on an increase at the next session in September.

In Canada, the TSX ended slightly higher, powered by a rebound in the financial sector after yesterday’s drop. In trading, Healthcare and Industrials gained the most while Consumer Staples and Technology had the biggest declines.

In the US of A, the DJIA ran its streak to thirteen while the other two American indexes ended slightly lower. In trading, the Financials and Industrials sector posted the biggest gains, while Basic Materials and Energy had the biggest drops.

Thursday: The markets got off to a good start following yesterday’s optimistic news out of the Fed, but then fell with a thud as all indexes ended lower. The indexes fell when the latest US GDP came in higher than expected, raising concerns of another interest rate hike. Oil prices rose after growing optimism over increasing Chinese demand, coupled with production cuts by OPEC+ countries.

In Canada, the TSX suffered its biggest loss since early July on concerns the Fed would raise the US interest rate after strong US economic data. In trading on Bay Street, every sector ended lower. Consumer Staples and Financials dropped the least, while Telecommunications Services and Basic Materials had the biggest declines.

In the US, the DJIA’s winning streak came to an end at thirteen. It was the DJIA’s longest winning streak since 1987. In trading on Wall Street, every sector ended lower. The Technology and Consumer Staples sectors had the smallest decline while Utilities and Telecommunications Services fell the furthest.

Friday: The markets ended the week on a positive note that saw all indexes advance. The latest PCE data showed inflation falling, raising investors’ hopes this week’s interest rate hike was the last one. Investors believe the US economy is going through a ‘Goldilocks’ scenario of ebbing consumer prices and strong growth that is considered a healthy sign for stocks. Oil prices rose as analysts believe there will be a combination of strong demand and supply cuts to keep prices high.

In Canada, a strong day on the TSX almost pulled the index out of the red for the week but fell just short. In trading in the Canadian sectors, Technology and Basic Materials led all gainers, while Utilities and Consumer Staples were the only sectors to fall back.

In the US, all three American indexes rebounded after yesterday’s losses. Today’s gains for the Nasdaq enabled the Nasdaq to end the week in the green. With the possibility of a Goldilocks scenario, many investors are moving back into the stock markets and looking outside of the high-flying technology sector. In trading, the higher growth Consumer Cyclicals and Technology sectors advanced the most, while the defensive Utilities sector was the only sector to end in the red.

Weekly Market and Portfolio Review

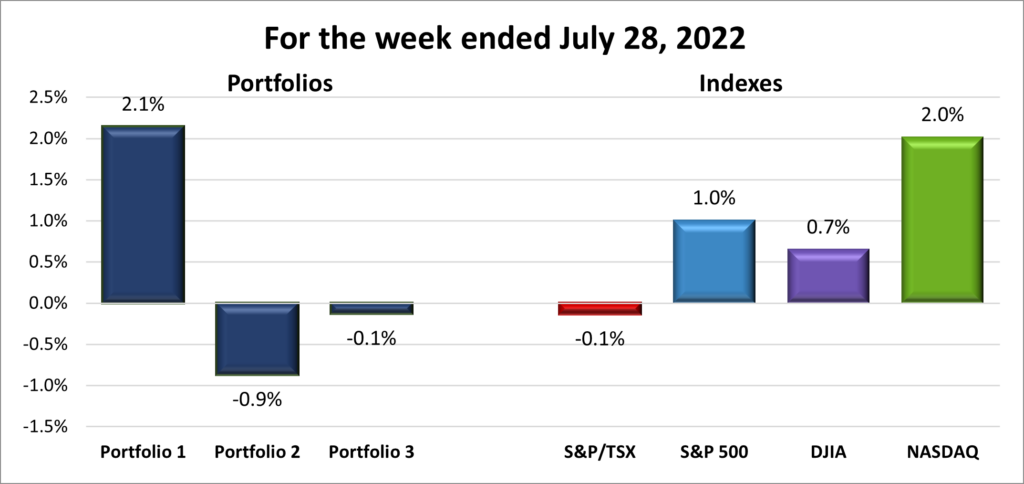

For the week, the TSX (SPTSX) slipped 0.1%, the S&P 500 (SPX) grew 1.0%, the DJIA (INDU) advanced 0.7% and the Nasdaq (CCMP) jumped 2.0%.

![]() As shown in the graph above, the four major North American indexes started the week headed in the right direction, but dipped midweek before rallying on Friday. Solid economic data out of the US, rising consumer sentiment, and renewed investor optimism lifted all four indexes. However, the TSX was the only index unable to end the week in positive territory. The TSX’s underperformance may be attributed to the possibility of another interest rate hike.

As shown in the graph above, the four major North American indexes started the week headed in the right direction, but dipped midweek before rallying on Friday. Solid economic data out of the US, rising consumer sentiment, and renewed investor optimism lifted all four indexes. However, the TSX was the only index unable to end the week in positive territory. The TSX’s underperformance may be attributed to the possibility of another interest rate hike.

![]() The performance of the Portfolios during the past week showed a mix of results, with two portfolios ending lower and one experiencing a positive outcome. As depicted in the chart below, the overall performance of the Portfolios was positive due to the strong showing from Portfolio 1, so I am giving the portfolios a bull for the past week. 😊 Portfolio 1 benefited from robust earnings in the technology sector.

The performance of the Portfolios during the past week showed a mix of results, with two portfolios ending lower and one experiencing a positive outcome. As depicted in the chart below, the overall performance of the Portfolios was positive due to the strong showing from Portfolio 1, so I am giving the portfolios a bull for the past week. 😊 Portfolio 1 benefited from robust earnings in the technology sector.

Portfolio 2 faced challenges as Microsoft’s share price was negatively impacted by investor concerns regarding the costs associated with building up their AI infrastructure. Additionally, TC Energy’s (TSX: TRP) announcement about splitting out the liquids pipelines business likely added to the pressures on Portfolio 2.

Portfolio 3 came close to breaking even but was slightly impacted by the decline in Microsoft’s share price.

Companies on the Radar

This past week two small cap (when the number of shares X the market price of those shares is between $300 million and $2 billion) American semiconductor companies came to my attention. The first is indie semiconductor (NASD: INDI), a developer of semiconductors and software solutions for the growing electric vehicle (EV) market.

This past week two small cap (when the number of shares X the market price of those shares is between $300 million and $2 billion) American semiconductor companies came to my attention. The first is indie semiconductor (NASD: INDI), a developer of semiconductors and software solutions for the growing electric vehicle (EV) market.

The other company is Navitas Semiconductor (NASD: NVTS), a developer of ultra-efficient gallium nitride (GaN) semiconductors. GaN chips provide significantly improved performance over conventional silicon semiconductors. GAN chips allow developers “to create smaller, lighter, faster and greener power conversion and power management solutions” that can be used in a wide variety of growing markets including EVs, solar panels, data centres and others.

Both are small cap companies, so they have plenty of room to grow, plus they are in the hot semiconductor industry. They both sound promising, so I added both to Portfolio 1. 😊

The Radar Check was last updated July 28, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended July 28, 2023: UP ![]()

- Despite increases in revenue and earnings, the share price of General Motors dipped when they announced their profit margins had fallen. As a result of the lower margins, GM plans to lower investment in new products and cut operating expenses to boost their profit margin.

GM announced a quarterly dividend of $0.09. - Alphabet’s second-quarter profit exceeded Wall Street expectations on steady demand for its cloud services, a rebound in advertising, and maintaining their dominant position in online search. Despite an initial stumble with the rollout of their AI products, Google Search was able to withstand competition from archrival Microsoft’s AI powered Bing. While Google has their own chips to handle the computing horsepower required for AI, they expect expenses to increase as they build out the necessary infrastructure (datacentres) to handle the demand for their AI services.

- Not wanting to miss out on the AI boom, Amazon (NASD: AMZN) has quietly rolled out its own AI offerings in its Amazon Web Services unit. Amazon has thousands of its customers testing out its AI services, called Bedrock, and should be generally available “soon.”

Activity

Received interest on TD 1-year cashable GIC.

Bought indie Semiconductor: An automotive semiconductor company that supplies chips to a wide range of vehicle manufacturers. They have positioned themselves well in the growing market for electric vehicles (EVs) and Advanced Driver Assistance Systems (ADAS), which are becoming increasingly important in the automotive industry. They claim one in four new vehicles includes at least one indie device, a testament to their strong presence in the market.

The company’s focus on improving and enhancing the driver and passenger experience through their chips further strengthens their position in the industry. Their founder-led corporate structure and positive culture rating on Glassdoor reflect a strong leadership and company culture, which can contribute to their growth and success.

While the financial numbers are not great now, significant increase in revenues from December 2021 to December 2022 shows promising growth potential. The fact that the losses are decreasing is also a positive sign, indicating that the company is making progress towards profitability.

As a small-cap company, indie Semiconductor does come with higher risks and volatility compared to larger, more established companies. Potential risks include ensuring a reliable supply to customers, maintaining the quality of their products, and facing competition from companies with greater financial resources.

I made an investment in indie Semiconductor because of the increasing demand for their products, which aligns with the tailwinds of the growing EV and ADAS markets. The fact that the four co-founders have a vested interest in the company’s success and have had success in their previous venture adds to my confidence. Overall, as long as indie Semiconductor continues to execute its growth strategies, the share price should follow suit. And I will a happy co-owner. 😊

Bought Navitas Semiconductor: Another small-cap American company. This one specializes in development of gallium nitride (GaN) power semiconductors and silicon carbide (SiC) chips and devices. These innovative chips offer significant improvements in performance and energy efficiency compared to traditional silicon technologies, making them highly sought-after in various high-frequency and high-power applications.

The company’s GaN chips have already found applications in diverse industries such as mobile chargers, consumer electronics, data centers, solar energy, renewable power fields, and electric vehicles (EVs). As technology continues to progress, and manufacturing processes become more refined, GaN chips are expected to penetrate even more markets and emerge as strong competitors to conventional silicon chips.

Navitas Semiconductor is led by a team of four founders, and with insiders holding 35% of the shares, there is a clear alignment of interests with the company’s success. The founders and management’s extensive background in the semiconductor field and startups add credibility to the company’s potential for growth.

From a financial standpoint, Navitas has been demonstrating robust revenue growth and achieved profitability last year. Additionally, the fact that the company has no debt only enhances its positive outlook.

However, there are risks associated with investing in new technology companies. Some of these risks include the potential challenges in gaining widespread adoption of GaN chips in various industries, securing a reliable supply of gallium, the emergence of a superior competing technology, and the entry of larger competitors into the market.

I decided to invest in Navitas because of its an early mover advantage in the next-generation semiconductor field, strong founder-led management, and its involvement in rapidly growing industries. As with any small-cap company that offers higher rewards, there are higher risks and greater share price volatility.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

General Motors Company

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their second quarter 2023 financial results on July 25, 2023

- Revenue of $44,746 for the three months ended June 30, compared to $35,759 for the same period in 2022. An increase of over 25%.

- Net income of $2,566 for the three months ended June 30, compared to net income of $1,692 in the same period in 2022.

- Diluted earnings per ordinary share of $1.83 for the three months ended June 30, compared to earnings of $1.14 per share for the same period in 2022.

- Revenue of $84,732 for the six months ended June 30, compared to $71,738 for the same period in 2022. An increase of over 18%.

- Net earnings of $4,962 for the six months ended June 30, compared to net earnings of $4,631 in the same period in 2022.

- Diluted earnings per ordinary share of $3.52 for the six months ended June 30, compared to earnings of $2.49 per share for the same period in 2022.

Alphabet Inc.

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their second quarter 2023 financial results on July 25, 2023

- Revenue of $74,604 for the three months ended June 30, compared to $69,685 for the same period in 2022. An increase of over 7%.

- Net income of $18,368 for the three months ended June 30, compared to net income of $16,002 in the same period in 2022.

- Diluted earnings per ordinary share of $1.44 for the three months ended June 30, compared to earnings of $1.21 per share for the same period in 2022.

- Revenue of $144,391 for the six months ended June 30, compared to $137,696 for the same period in 2022. An increase of almost 5%.

- Net earnings of $33,419 for the six months ended June 30, compared to net earnings of $32,438 in the same period in 2022.

- Diluted earnings per ordinary share of $2.61 for the six months ended June 30, compared to earnings of $2.44 per share for the same period in 2022.

Visa Inc.

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on July 25, 2023

- Revenue of $8,1238 for the three months ended June 30, compared to $7,275 for the same period in 2022. An increase of almost 12%.

- Net income of $4,156 for the three months ended June 30, compared to net income of $3,411 in the same period in 2022.

- Diluted earnings per ordinary share of $2.00 for the three months ended June 30, compared to earnings of $1.60 per share for the same period in 2022.

- Revenue of $24,044 for the six months ended June 30, compared to $21,523 for the same period in 2022. An increase of almost 12%.

- Net earnings of $12,592 for the six months ended June 30, compared to net earnings of $11,017 in the same period in 2022.

- Diluted earnings per ordinary share of $6.03 for the six months ended June 30, compared to earnings of $5.15 per share for the same period in 2022.

CN Rail Company

All currency listed in millions of Canadian dollars, except for per share data.

Selected highlights from their second quarter 2023 financial results on July 25, 2023

- Revenue of $4,057 for the three months ended June 30, compared to $4,344 for the same period in 2022. A decrease of over 6%.

- Net income of $1,335.8 for the three months ended June 30, compared to net income of $888.2 in the same period in 2022.

- Diluted earnings per ordinary share of $1.76 for the three months ended June 30, compared to earnings of $1.92 per share for the same period in 2022.

- Revenue of $8,370 for the six months ended June 30, compared to $8,052 for the same period in 2022. An increase of almost 4%.

- Net earnings of $2,387 for the six months ended June 30, compared to net earnings of $2,243 in the same period in 2022.

- Diluted earnings per ordinary share of $25.26 for the six months ended June 30, compared to earnings of $12.56 per share for the same period in 2022.

Teladoc Health, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their second quarter 2023 financial results on July 25, 2023

- Revenue of $652,406 for the three months ended June 30, compared to $592,379 for the same period in 2022. An increase of over 10%.

- Net loss of $65,177 for the three months ended June 30, compared to a net loss of $3,101,461 in the same period in 2022.

- Diluted loss per ordinary share of $0.40 for the three months ended June 30, compared to a loss of $19.22 per share for the same period in 2022.

- Revenue of $7,145.2 for the six months ended June 30, compared to $4,126.3 for the same period in 2022. An increase of over 73%.

- Net loss of $134,405 for the six months ended June 30, compared to a net loss of $9,775,984 in the same period in 2022.

- Diluted loss per ordinary share of $0.82 for the six months ended June 30, compared to a loss of $60.72 per share for the same period in 2022.

Roku, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their second quarter 2023 financial results on July 27, 2023

- Revenue of $847,186 for the three months ended June 30, compared to $764,406 for the same period in 2022. An increase of almost 11%.

- Net loss of $107,595 for the three months ended June 30, compared to a net loss of $112,321 in the same period in 2022.

- Diluted loss per ordinary share of $0.76 for the three months ended June 30, compared to a loss of $0.82 per share for the same period in 2022.

- Revenue of $1,588,176 for the six months ended June 30, compared to $1,498,105 for the same period in 2022. An increase of over 6%.

- Net loss of $301,199 for the six months ended June 30, compared to a net loss of $138,627 in the same period in 2022.

- Diluted loss per ordinary share of $2.14 for the six months ended June 30, compared to a loss of $1.02 per share for the same period in 2022.

TMX group Limited

All currency listed in millions of Canadian dollars, except for per share data.

Selected highlights from their second quarter 2023 financial results on July 27, 2023

- Revenue of $306.2 for the three months ended June 30, compared to $285.1 for the same period in 2022. An increase of over 7%.

- Net income of $97.3 for the three months ended June 30, compared to net income of $92.1 in the same period in 2022.

- Diluted earnings per ordinary share of $0.35 for the three months ended June 30, compared to earnings of $0.33 per share for the same period in 2022.

- Revenue of $605.3 for the six months ended June 30, compared to $572.4 for the same period in 2022. An increase of almost 6%.

- Net earnings of $186.3 for the six months ended June 30, compared to net earnings of $379.7 in the same period in 2022.

- Diluted earnings per ordinary share of $0.67 for the six months ended June 30, compared to earnings of $1.28 per share for the same period in 2022.

Portfolio 2

Portfolio 2 for the week ended July 28, 2023: DOWN ![]()

- TC Energy plans to sell its 40% share of Columbia Gas Transmission and Columbia Gulf Transmission pipelines for $3.95 billion to Global Infrastructure Partners (GIP). However, TC Energy will remain involved through a joint venture with GIP, operating the pipelines and sharing in the annual maintenance and system upgrades.

In other TC Energy news, the company plans to split into two companies. One company will deal with natural gas pipelines and power and energy solutions. The other company will focus on the liquids pipelines business. The split is expected to close at the end of 2024. - Telus’s (TSX: T) venture capital firm TELUS Pollinator Fund for Good announced it is making an investment into Dryad, a German startup that uses sensors for early wildfire detection. Dryad plans to deploy 120 million sensors throughout the world by 2030 to protect nearly 4 million hectares of forest The investment will help the startup further scale in Canada and the US.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX: DIR.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Microsoft Corporation

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their fourth quarter 2023 financial results on July 25, 2023

- Revenue of $56,189 for the three months ended June 30, compared to $51,865 for the same period in 2022. An increase of over 8%.

- Net income of $20,081 for the three months ended June 30, compared to net income of $16,740 in the same period in 2022.

- Diluted earnings per ordinary share of $2.69 for the three months ended June 30, compared to earnings of $2.23 per share for the same period in 2022.

- Revenue of $211,915 for the twelve months ended June 30, compared to $198,270 for the same period in 2022. An increase of almost 7%.

- Net earnings of $72,361 for the twelve months ended June 30, compared to net earnings of $72,738 in the same period in 2022.

- Diluted earnings per ordinary share of $9.68 for the twelve months ended June 30, compared to earnings of $9.65 per share for the same period in 2022.

TC Energy Corporation

All currency listed in millions of Canadian dollars, except for per share data.

Selected highlights from their second quarter 2023 financial results on July 28, 2023

- Revenue of $3,830 for the three months ended June 30, compared to $3,637 for the same period in 2022. An increase of over 5%.

- Net income of $250 for the three months ended June 30, compared to net income of $889 in the same period in 2022.

- Diluted earnings per ordinary share of $0.24 for the three months ended June 30, compared to earnings of $0.90 per share for the same period in 2022.

- Revenue of $7,758 for the six months ended June 30, compared to $7,137 for the same period in 2022. An increase of almost 9%.

- Net earnings of $1,563 for the six months ended June 30, compared to net earnings of $1,247 in the same period in 2022.

- Diluted earnings per ordinary share of $1.53 for the six months ended June 30, compared to earnings of $1.27 per share for the same period in 2022.

Portfolio 3

Portfolio 3 for the week ended July 28, 2023: DOWN ![]()

- Microsoft beat second quarter expectations, thanks to growth in its Azure cloud unit. Azure is the most likely part of Microsoft to capitalize on the soaring interest in AI. Despite beating expectations, the share price fell as investors were concerned about the amount of money being spent on AI and the infrastructure to support AI (datacentres).

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Microsoft Corporation

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their fourth quarter 2023 financial results on July 25, 2023

- Revenue of $56,189 for the three months ended June 30, compared to $51,865 for the same period in 2022. An increase of over 8%.

- Net income of $20,081 for the three months ended June 30, compared to net income of $16,740 in the same period in 2022.

- Diluted earnings per ordinary share of $2.69 for the three months ended June 30, compared to earnings of $2.23 per share for the same period in 2022.

- Revenue of $211,915 for the twelve months ended June 30, compared to $198,270 for the same period in 2022. An increase of almost 7%.

- Net earnings of $72,361 for the twelve months ended June 30, compared to net earnings of $72,738 in the same period in 2022.

- Diluted earnings per ordinary share of $9.68 for the twelve months ended June 30, compared to earnings of $9.65 per share for the same period in 2022.

Real Matters Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on July 28, 2023

- Revenue of $45,950 for the three months ended June 30, compared to $78,704 for the same period in 2022. A decrease of almost 42%.

- Net loss of $619 for the three months ended June 30, compared to a net loss of $1,424 in the same period in 2022.

- Diluted loss per ordinary share of $0.01 for the three months ended June 30, compared to a loss of $0.02 per share for the same period in 2022.

- Revenue of $121,725 for the nine months ended June 30, compared to $281,442 for the same period in 2022. A decrease of almost 57%.

- Net loss of $7,818 for the nine months ended June 30, compared to net earnings of $703 in the same period in 2022.

- Diluted loss per ordinary share of $0.11 for the nine months ended June 30, compared to earnings of $0.01 per share for the same period in 2022.