Items that may only interest or educate me ….

Canadian interest rate pauses, Canadian trade surplus, Canadian economy grows, US interest rate concerns, US jobs, US bank fails …

January’s inflation rate was 5.9%, down from December’s 6.3%, and the economy was flat during the fourth quarter (October 1 through December 31). Given this environment, the Bank of Canada (BoC) doesn’t need additional interest rate hikes to keep inflation trending downward. Instead, the BoC plans to maintain the benchmark interest rate at 4.50% for the rest of this year.

At this week’s BoC meeting, the central bank announced it would hold the Canadian benchmark interest rate at 4.5%, making it the first major central bank to pause increases. It was the first time in over a year that the benchmark interest rate remained unchanged after eight consecutive increases. The BoC cited recent data that showed the economy was starting to slow down, a sign that the previous rate hikes were working. In an ideal scenario, inflation would fall back to the BoC’s 1% – 3% target range without any further intervention. However, they also made it clear that they were “prepared to increase the policy rate further if needed to return to the two per cent inflation target.”

One threat to the Canadian borrowing rate is the growing divergence from the US borrowing rate. Currently the Canadian benchmark interest rate is 4.5%, while the American rate is 4.75%. The US Federal Reserve (Fed) indicated they will raise the US benchmark interest rate by 0.25% at least once more, bringing the rate to at least 5.25%. Each time the Fed raises the rate it will likely create a higher exchange rate for American imports making them more expensive for Canadians, possibly triggering inflation by imported goods.

This BoC’s decision to pause rate increases in the face of higher US interest rates has already caused the Canadian dollar to drop to a five-month low against the US dollar. It will be interesting to see how the BoC responds if the Fed keeps raising the key US rate. Does it choose to increase rates to protect the Canadian dollar at the expense of the Canadian economy, or suspend or lower the interest rate, which will hurt the Canadian dollar and possibly trigger another type of inflation?

On the same day the BoC held the line on the interest rate, Statistics Canada reported a C$ 1.9 billion trade surplus in January. Analysts had expected a deficit of C$ 60 million. The December numbers were also revised from a C$ 160 million deficit to C$ 1.2 billion surplus. Total exports increased 4.2% to C$ 67 billion thanks to a wide ranging increase across all types of exports. One notable exception was a decline in energy products. Imports increased for the first time in three months, gaining 3.1% to C$ 65.1 billon. Motor vehicles and industrial equipment both rose more than 10% and were the primary driver for the increase. Trade with countries other than the US was also up, with exports rising 7.2% and imports rising 4.6%.

Statistics Canada reported the country’s February Labour Survey showed the Canadian economy added 21,800 jobs in February, analysts had been expecting an increase 10,000 jobs. The February jobs number was down considerably from 150,000 new jobs in January. Wage growth rose 5.4% in February, on a year over year basis, up from January’s 4.5%. Unemployment remained at 5.0% for the second consecutive month, slightly lower than analysts predictions of 5.1%.

If the Canadian labour market and wages keep growing, the BoC will likely increase Canada’s key interest rate at least once more in 2023 in their battle to bring down inflation. If inflation sticks around and the Fed makes more than one increase, the BoC will almost be forced to raise the interest rate.

The Fed has been signalling for a while now that they plan to raise rates higher and for longer to tame stubborn inflation. Many believed this was just talk. They factored in a 0.25% increase and thought that would be it. This week, Fed Chair Jerome Powell went to Congress and told them what he’s been telling us for a while now – interest rates will likely go higher than they originally predicted, and they may be forced to increase the size of the hikes. The markets reacted as if this was a surprise and immediately sank. Hearing it directly from Mr. Powell was different than inferring it from the various reports.

Mr. Powell said no decision regarding the size of the Fed’s upcoming interest rate hike had been made, but indicated if the data suggested a bigger interest rate hike was required, “we would be prepared to increase the pace of rate hikes.” In other words, a 0.5% increase is possible, and additional rate hikes are likely to continue until the job numbers start to trend lower and the pace of wage increases falls. So now higher for longer has been replaced by higher, faster, longer.

He acknowledged the rate hikes would be painful but explained inflation hurts all Americans and raising interest rates is the only tool the Fed has to get inflation back down to their 2% target. He said the Fed was prepared to “stay the course until the job is done.” One thing for sure, Mr. Powell’s remarks rattled the markets, raising the volatility.

Who knew higher for longer actually meant, higher for longer. Another reason to remember the saying, “Don’t fight the Fed.”

The US Department of Labor reported 311,000 jobs were added to the American economy in February, higher than analysts’ projected 225,000, but a slowdown from January’s 511,000. However, the unemployment rate rose from a 54-year low of 3.4% to 3.6% thanks to more people entering the labour pool. As well, wage growth continued to slow, rising by 0.2% in February, down from January’s 0.3% gains.

The mixed signals of the report calmed investors who were concerned if the jobs report was too strong it would lead to the Fed raising the key interest rate by 0.05%. After this week’s jobs report showing the number of new jobs declined, wages growth slowed and unemployment rose, analysts and investors are now expecting a 0.25% increase. Next week’s CPI and retail sales results should provide investors an indication whether we are in store for the hoped for 0.25% increase or the higher 0.5% increase.

While fears of higher US interests were the talk of investors at the start of the week, the primary topic of conversation turned dramatically Wednesday afternoon when the SVB Financial Group (NASD:SIVB) announced they had lost US$ 1.8 billion on the sale of US$ 21 billion of securities. The sale was necessitated to provide cash to customers who needed to withdraw their money. Once investors got wind of this news they dumped their SIVB shares as fast as they could, sending the share price into a freefall. The share price plunged from US$ 268 late Wednesday afternoon to US$ 106 on Friday morning, before trading was halted by regulators.

Friday morning, California regulators took control of the bank, citing “inadequate liquidity and insolvency.” The Federal Deposit Insurance Corporation (FDIC) was assigned as the receiver. Insured depositors should have access to their money by Monday, while uninsured depositors will receive “an advance dividend within the next week.,” They will also receive a receivership certificate (essentially an IOU for any funds recovered) for the remaining amount of their uninsured funds. The bank is expected to resume its banking activities on Monday. No word if or when shares in SIVB will resume trading.

The collapse of SIVB was dramatically swift but not before concerns of liquidity swept through the American banking system and spread into Canada and other countries. The price of bank shares everywhere were down on Friday.

Back in late 2020, I considered SIVB because it was the banker to many of the high-flying tech stocks. The market, especially the technology sector was on a roll and SIVB had lots of upward momentum. I decided not buy shares for two reasons: I already had banks and other financial sector companies in each of the portfolios; since the 2008 financial crash I’ve been leery of American banks as investments. I believe Canadian banks are much more conservative than American banks and I had very little firsthand experience with American banking system. With memories of the 2008 financial crash in the back of my mind, I felt the risk was too high for me. I’m very glad I decided to stick to the Canadian financial sector.

For more on the Silicon Bank collapse, check out the post “48 hours: The Demise of a bank.”

Besides the demise of a bank, let’s see what other exciting events happened this past week….

Weekly Market Review

Monday: After last week’s late rally, the indexes got off to a good start but faded at lunch before finishing the day either barely above or barely below where they started. In Canada, the resource heavy Toronto Stock Exchange Composite Index (TSX) ended lower after China set a lower-than-expected growth target. Projected softer demand from China dragged down commodity prices. In the Canadian S&P sector, Consumer Staples, Telecommunications Services, and Utilities were the only sectors to end higher, while Basic Materials (miners and fertilizer manufacturers) and Healthcare fell the most.

In the USA, investors were waiting to hear what the Fed chair would say to the US Congress this week. Investors hoped to get an idea about the number and size of upcoming interest rate hikes. The lates jobs report comes out at the end of the week. Investors are hoping to see the number of new jobs is decreasing and wage growth is slowing. In the markets, the S&P 500 Index (S&P) and the Dow Jones Industrial Average (DJIA) edged higher while the Nasdaq Composite Index (Nasdaq) ended slightly lower. In the American S&P sectors, Utilities, Technology and Telecommunications Services were the only sectors to advance. Basic Materials and Consumer Cyclicals dropped the most.

Tuesday: All four indexes plunged when the Fed Chair told the US Congress that interest rates were likely to go higher, and they were prepared to make larger increases if needed. His comments opened the door for a 0.5% increase to the US benchmark rate at the next meeting of the Fed in late March. Analysts and investors had been expecting 0.25% rate increase. Oil prices fell on China’s weak growth forecast.

In Canada, concerns of lower demand from China for commodities combined with news of higher US interest rates to send all Canadian sectors lower except for the defensive Utilities sector. The commodities sectors Basic Materials and Energy took the brunt of the pain, dropping the most.

In the US, fears of a larger increase sent investors scurrying for the exists, causing each American index to fall by more than 1%. In trading, all S&P US sectors ended lower. Telecommunications Services and Technology dropped the least while Basic Materials and Financials dropped the most.

Wednesday: It was a rollercoaster ride for all four indexes. A late rally lifted all four indexes but not enough to get the DJIA above the line to join the other three indexes in the green. Economic data indicated the number of job openings declined, a sign that the American economy was slowing. Oil prices dropped as fears of higher interest rates won the daily tug of war with hopes for higher consumption from China.

In Canada, the TSX closed higher, recouping some of the losses from earlier this week. The main driver was Canadian technology companies rising on the news the BoC left the key Canadian interest rate at 4.5%, as expected. On the trading floor, the Technology sector gained more than three times as much as the Industrials sectors, the second-best performer of the Canadian sectors. The Healthcare and Consumer Cyclicals sectors were the worst performers of a group of four sectors that all ended lower.

In the US, investors considered the Fed Chair’s remarks that there may be a larger than expected interest rate hike, but no decision about the size of the increase had been made. Investors are now waiting for the February jobs report due Friday, and next week’s US Consumer Price Index (CPI) report. On Wall Street, of the S&P American sectors, Basic Materials and Utilities gained the most while Energy and Healthcare dropped the most.

Thursday: All four indexes rose in early morning trading before turning sharply downward to end the day solidly in the red. The main driver was fear tomorrow’s US jobs report could lead to an aggressive interest rate hike by the Fed. Financial companies in Canada and the US took a hit after the American bank SVB Financial launched a capital raise to strengthen its balance sheet. SIVB is one of the most popular bankers for American startup technology and healthcare companies.

In Canada, the TSX fell hard on concerns about job numbers in both countries. The downdraft caused by the US financial sector didn’t help. Every Canadian sector ended in the red with Technology and Utilities dropping the least while Telecommunications Services and Basic Materials fell the furthest.

In the US, problems with SIVB rippled throughout the US financial sector, sending the Financials sector to is biggest one day decline in almost three years. SIVB itself saw its share price fall by more than 60%. In trading, it was a broad-based day of losses in the American markets as all sectors ended the day lower. The defensive sectors Consumer Staples and Utilities fell the least while Financials and Basic Materials faired the worst.

Friday: The week ended on a sour note as all four major North American indexes each lost over 1% today. The failure of SIVB led to an overall drop in bank companies in the US, and Canadian banks were caught in the downdraft. Oil prices fell again on concerns US rate hikes could cause a recession and drive down demand for oil.

In Canada, another higher than expected Canadian jobs report raised concerns the BoC may need to raise Canada’s borrowing rate again to ensure inflation in Canada remains on its downward trajectory. In trading, all Canadian sectors declined with Telecommunications Services and Basic Materials falling the least, while Technology and Financials fell the furthest.

In the US, once again the US jobs report came in better than expected, showing a slowdown from January and that wage growth continued to slow. Normally the jobs report would have been the lead financial item, but it was overshadowed by the uncertainties of the banking system. In the American markets, for the second straight day, no sector was spared. Telecommunications Services and Consumer Staples fell the least while Financials and Industrials dropped the most.

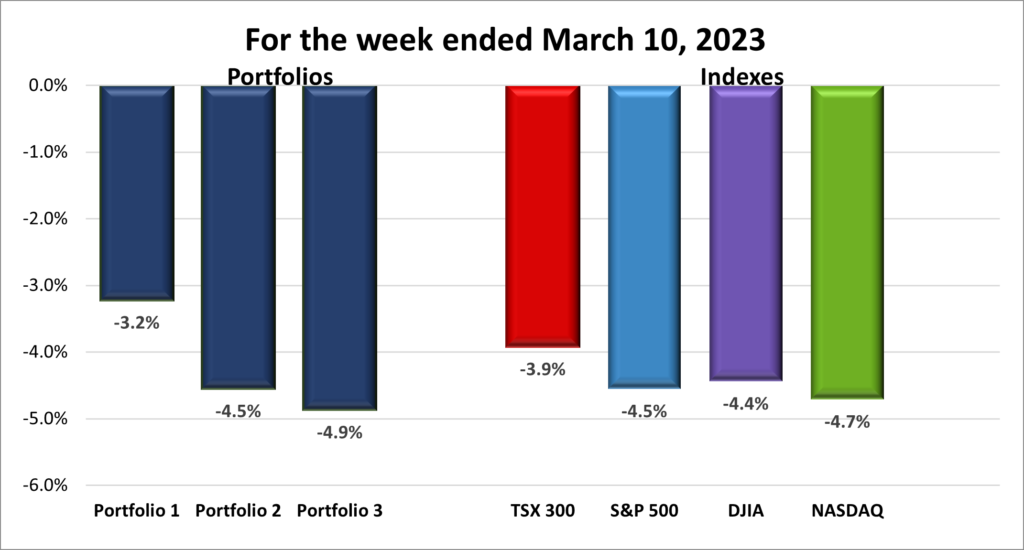

For the week, the TSX dropped 3.9%, the S&P 500 fell 4.5%, the DJIA had it worst week since June 2022, sinking 4.4% and the Nasdaq plunged 4.7%.

Weekly Portfolio Review

![]() A quick look at the chart above and it won’t take much to see it was not a good week in the markets. If it had been a water slide, it would’ve been a fun ride. 😊 Midweek comments from the Fed Chair, mixed data from the February jobs report, and then the meltdown of the SIVB to end the week were the main culprits for the plunge of the three American indexes.

A quick look at the chart above and it won’t take much to see it was not a good week in the markets. If it had been a water slide, it would’ve been a fun ride. 😊 Midweek comments from the Fed Chair, mixed data from the February jobs report, and then the meltdown of the SIVB to end the week were the main culprits for the plunge of the three American indexes.

The TSX suffered its largest weekly decline since September 2022, dragged down by the crisis in the US banking sector. Concerns of higher American interest rates, and the mixed Canadian February jobs report caused speculation that the BoC would raise the Canadian benchmark interest rate, either to protect the Canadian dollar, drive down inflation in Canada, or both.

With the indexes tumbling this past week it was no surprise all three portfolios were lower, as shown below. Each portfolio owns at least one of the big five Canadian banks which were dragged down by the overall global downdraft in financial stocks.

With concerns about the Fed’s upcoming increase to the US interest rate in the next two weeks, and more shake out to come from the Silicon Valley Bank collapse, I am guessing the next few weeks will be quite volatile. Hopefully, losses will be minimal, but the markets are unpredictable, as we experienced this past week.

Companies on the Radar

This past week I dropped Kits Eyecare (TSX:KITS) from my Radar List because it seems too risky given the current financial environment. The other company dropping off the radar was Jabil Inc. (NYSE:JBL). I haven’t decided one way or another after a few weeks of being on the radar so I might as well move it off.

This past week I dropped Kits Eyecare (TSX:KITS) from my Radar List because it seems too risky given the current financial environment. The other company dropping off the radar was Jabil Inc. (NYSE:JBL). I haven’t decided one way or another after a few weeks of being on the radar so I might as well move it off.

Joining the three holdovers from last week (listed below) are Airbnb (NASD:ABNB), Vale (NYSE:VALE) and Smartcentres Real Estate Investment Trust (TSX:SRU.UN). Airbnb is the online platform allowing people to book private residences for short term stays. The company has grown considerably in popularity and financially the last few years. The share price was knocked down significantly in 2022 so this might be a good time to invest.

Vale is a global mining company that extracts and sells various metals and rare earth elements such as nickel, cobalt, gold, copper, and the traditional iron ore. Many of the metals are used in the growing electric vehicles industry and electrical charging systems. As long as there is demand for electric vehicles, there should be demand for at least one of the metals this company produces. The company also provides a 4% dividend.

Smartcentres owns and manages a number of income producing malls and retails spaces across Canada, with Walmart Canada as one of their principal tenants. The company plans to develop their existing malls into mixed residential, office and retail spaces. This should provide a good mix of income producing properties, all in one company. The monthly dividend is currently close to 7%.

On a side note, companies on the radar are companies not owned in any of the three portfolios. When it comes to investing in a company, it may be from the list below or a company in one of the Portfolios.

- Intact Financial (TSX:IFC): a mid size insurance company supplying home, car and business insurance in Canada, the US, and the UK.

- Hammond Power Solutions (TSX:HPS.A): a Canadian company manufacturing transformers used throughout the world in a wide variety of industries.

- Supremex (TSX:SXP): a small cap company selling packing solutions throughout Canada and the USA.

The Radar Check was last updated March 10, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended March 10, 2023: DOWN ![]()

- Tesla (NASD:TSLA) has again lowered prices on their electric vehicles. This time it was the Plaid (higher performance) versions of the Model S (4%) and Model X (9%). The lower prices are part of Tesla’s strategy to drive demand through lower prices.

Separately, National Highway Traffic Safety Administration (NHTSA) has started an investigation to determine if steering wheels in the 2023 Model Y were not properly secured to the steering column. There have been two reports of the steering wheel coming off while the vehicles were being driven.

Tesla also announced the plain to eliminate the use of rare earth elements (REE) from the next generation of their electric vehicles. They plan to redesign their motors to eliminate REE in favour of other alternatives such as ferrite. One reason for the switch is many of the REE used in the vehicles come from China. Tesla, and other car companies, have a strong desire to wean themselves from volatile Chinese based supply chains. I suspect if a western friendly nation can supply the REE needed by the EV there won’t be as much urgency to become REE free. - One of the biggest buyers of Nvidia’s (NASD:NVDA) semiconductors is China’s Huawei. Unfortunately for Nvidia, Huawei is one of many Chinese companies on the US government’s blacklist. Under current US law, American companies cannot sell advanced technologies, like semiconductors, to Chinese companies. Under a proposed amendment, the US government will further restrict sales to Huawei which will have a negative impact on Nvidia sales.

- As part of efforts to reduce cost, GM (NYSE:GM) has offered buyouts to salaried employees in the US with five or more years of service and global employees with at least two years of service. GM expects to take this US$ 1.5 billion charge in the first half of 2023.

- For the third straight year, Lattice Semiconductor (NASD:LSCC) has won a Cybersecurity Excellence Award. Their Lattice Sentry and Lattice SupplyGuard were rated the best in North America in the embedded security and endpoint security product/service categories.

Activity

Bought Trisura Group (TSX:TSU). I mentioned in the February 24 Weekly Update, I sold some shares in Trisura when I found out it had pushed back its earnings announcement. The earnings report came out last week and the share price jumped to higher than I had sold it. This was looking like a case of shooting myself in the foot if I wanted to buy back the shares. However, I put in a limited Buy bid, good until March 10, for approximately $1 less than I had sold it, hoping the share price would fall to that level. Fortunately, this week Trisura’s share price temporarily dropped far enough that my bid was hit. I am back to the number of shares I originally had, and after transaction fees, I made a few bucks. 😊

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

TMX Group Ltd (TSX:X)

US $

No US$ dividends this past week.

Quarterly Reports

Cargojet Inc.

All currency listed in millions of Canadian dollars.

Selected highlights from their fourth quarter 2022 financial results on March 6, 2023

- Revenue of $267 for the three months ended December 31, compared to $235.9 for the same period in 2021. An increase of over 13%.

- Net income of $2.6 for the three months ended December 31, compared to net income of $102 in the same period in 2021.

- Diluted earnings per ordinary share of $0.15 for the three months ended December 31, compared to earnings per share of $5.70 for the same period in 2021.

- Revenue of $979.9 for the year ended December 31, compared to $757.8 for the same period in 2021. An increase of over 29%.

- Net earnings of $190.6 for the year ended December 31, compared to net earnings of $167.4 in the same period in 2021.

- Diluted earnings per ordinary share of $10.15 for the year ended December 31, compared to earnings per share of $9.51 for the same period in 2021.

Crowdstrike Holdings, Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 7, 2023

- Revenue of $637,367 for the three months ended December 31, compared to $431,010 for the same period in 2021. An increase of almost 48%.

- Net loss of $48,932 for the three months ended December 31, compared to a net loss of $41,739 in the same period in 2021.

- Diluted loss per ordinary share of $0.20 for the three months ended December 31, compared to a loss per share of $0.18 for the same period in 2021.

- Revenue of $2,241,236 for the year ended December 31, compared to $1,451,594 for the same period in 2021. An increase of over 54%.

- Net loss of $182,285 for the year ended December 31, compared to a net loss of $232,378 in the same period in 2021.

- Diluted loss per ordinary share of $0.79 for the year ended December 31, compared to a loss per share of $1.03 for the same period in 2021.

SE Limited

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 7, 2023

- Revenue of $3451,584 for the three months ended December 31, compared to $3,222,114 for the same period in 2021. An increase of over 7%.

- Net income of $422,838 for the three months ended December 31, compared to a net loss of $616,289 in the same period in 2021.

- Diluted earnings per ordinary share of $0.72 for the three months ended December 31, compared to a loss per share of $1.12 for the same period in 2021.

- Revenue of $12,449,705 for the year ended December 31, compared to $9,955,190 for the same period in 2021. An increase of over 25%.

- Net loss of $1,657,772 for the year ended December 31, compared to a net loss of $2,043,030 in the same period in 2021.

- Diluted loss per ordinary share of $2.96 for the year ended December 31, compared to a loss per share of $3.84 for the same period in 2021.

Nuvei Corporation

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 8, 2023

- Revenue of $220,339 for the three months ended December 31, compared to $211,875 for the same period in 2021. An increase of almost 4%.

- Net income of $9,352 for the three months ended December 31, compared to net income of $12,339 in the same period in 2021.

- Diluted earnings per ordinary share of $0.06 for the three months ended December 31, compared to earnings per share of $0.07 for the same period in 2021.

- Revenue of $843,323 for the year ended December 31, compared to $724,526 for the same period in 2021. An increase of over 16%.

- Net earnings of $61,955 for the year ended December 31, compared to net earnings of $107,045 in the same period in 2021.

- Diluted earnings per ordinary share of $0.39 for the year ended December 31, compared to earnings per share of $0.71 for the same period in 2021.

Docusign, Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 9, 2023

- Revenue of $659,576 for the three months ended January 31, compared to $580,828 for the same period in 2022. An increase of over 13%.

- Net income of $4,863 for the three months ended January 31, compared to a net loss of $30,445 in the same period in 2022.

- Diluted earnings per ordinary share of $0.02 for the three months ended January 31, compared to a loss per share of $0.15 for the same period in 2022.

- Revenue of $2,515,915 for the year ended January 31, compared to $2,107,213 for the same period in 2022. An increase of over 19%.

- Net loss of $97,454 for the year ended January 31, compared to a net loss of $69,976 in the same period in 2022.

- Diluted loss per ordinary share of $0.49 for the year ended January 31, compared to a loss per share of $0.36 for the same period in 2022.

Nano-X Imaging Ltd.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 9, 2023

- Revenue of $2,132 for the three months ended December 31, compared to $1,304 for the same period in 2021. An increase of almost 64%.

- Net loss of $44,837 for the three months ended December 31, compared to a net loss of $22,035 in the same period in 2021.

- Diluted loss per ordinary share of $0.86 for the three months ended December 31, compared to a loss per share of $0.44 for the same period in 2021.

- Revenue of $8,579 for the year ended December 31, compared to $1,304 for the same period in 2021. An increase of over 660%.

- Net loss of $105,243 for the year ended December 31, compared to a net loss of $61,798 in the same period in 2021.

- Diluted earnings per ordinary share of $2.01 for the year ended December 31, compared to earnings per share of $1.28 for the same period in 2021.

Docebo Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 9, 2023

- Revenue of $38,955 for the three months ended December 31, compared to $29,801 for the same period in 2021. An increase of almost 31%.

- Net income of $1,600 for the three months ended December 31, compared to a net loss of $1,428 in the same period in 2021.

- Diluted earnings per ordinary share of $0.05 for the three months ended December 31, compared to a loss per share of $0.04 for the same period in 2021.

- Revenue of $142,912 for the year ended December 31, compared to $104,242 for the same period in 2021. An increase of over 37%.

- Net earnings of $7,018 for the year ended December 31, compared to a net loss of $13,601 in the same period in 2021.

- Diluted earnings per ordinary share of $0.21 for the year ended December 31, compared to a loss per share of $0.41 for the same period in 2021.

Crew Energy Inc.

All currency listed in thousands of Canadian dollars.

Selected highlights from their fourth quarter 2022 financial results on March 8, 2023

- Revenue of $136,948 for the three months ended December 31, compared to $103,153 for the same period in 2021. An increase of almost 33%.

- Net income of $71,383 for the three months ended December 31, compared to net income of $50,901 in the same period in 2021.

- Diluted earnings per ordinary share of $0.44 for the three months ended December 31, compared to earnings per share of $0.31 for the same period in 2021.

- Revenue of $598,569 for the year ended December 31, compared to $332,848 for the same period in 2021. An increase of almost 80%.

- Net earnings of $264,359 for the year ended December 31, compared to net earnings of $205,299 in the same period in 2021.

- Diluted earnings per ordinary share of $1.63 for the year ended December 31, compared to earnings per share of $1.27 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended March 10, 2023: DOWN ![]()

- A new oversight board that controls the Disney World (NYSE:DIS) special taxing district, handpicked by the Governor of Florida, will be examining “all of the needed actions to get back on track.” Disney World has been an autonomous tax district since inception so it will be interesting what impacts this new oversight board has on the ‘Happiest place on Earth.’

- Guardant Health and Sermonix Pharmaceuticals, announced the start of a phase 3 ELAINE-3 study of lasofoxifene. They study will use Guardant’s Guardant360 CDx blood test to identify patients who have an ESR1 mutation after first-line therapy. The Guardant360 CDx liquid biopsy is a next-generation sequencing-based test that detects genomic alterations using circulating tumor DNA from the blood. Lasofoxifene is used for certain metastatic breast cancer patients who are resistant to existing endocrine therapies.

In a separate announcement, Guardant submitted the premarket approval application for its Shield blood test to the US Food and Drug Administration. Shield is the company’s blood test to screen for colorectal cancer.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

Microsoft Corp. (NASD:MSFT)

Quarterly Reports

MongoDB, Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 8, 2023

- Revenue of $361,312 for the three months ended January 31, compared to $266,494 for the same period in 2021. An increase of almost 36%.

- Net loss of $64,398 for the three months ended January 31, compared to a net loss of $84,448 in the same period in 2021.

- Diluted loss per ordinary share of $0.93 for the three months ended January 31, compared to a loss per share of $1.26 for the same period in 2021.

- Revenue of $1,284,040 for the year ended January 31, compared to $837,782 for the same period in 2021. An increase of almost 47%.

- Net loss of $345,398 for the year ended January 31, compared to a net loss of $306,866 in the same period in 2021.

- Diluted loss per ordinary share of $5.03 for the year ended January 31, compared to a loss per share of $4.75 for the same period in 2021.

Crew Energy Inc.

All currency listed in thousands of Canadian dollars.

Selected highlights from their fourth quarter 2022 financial results on March 8, 2023

- Revenue of $136,948 for the three months ended December 31, compared to $103,153 for the same period in 2021. An increase of almost 33%.

- Net income of $71,383 for the three months ended December 31, compared to net income of $50,901 in the same period in 2021.

- Diluted earnings per ordinary share of $0.44 for the three months ended December 31, compared to earnings per share of $0.31 for the same period in 2021.

- Revenue of $598,569 for the year ended December 31, compared to $332,848 for the same period in 2021. An increase of almost 80%.

- Net earnings of $264,359 for the year ended December 31, compared to net earnings of $205,299 in the same period in 2021.

- Diluted earnings per ordinary share of $1.63 for the year ended December 31, compared to earnings per share of $1.27 for the same period in 2021.

Portfolio 3

Portfolio 3 for the week ended March 10, 2023, 2023: DOWN ![]()

- The Australian Competition and Consumer Commission (ACCC) is launching a probe into the various digital platforms offered by companies such as Microsoft (NASD:MSFT) and Alphabet (NASD:GOOGL). The probe will examine expansion strategies, the interoperability of the platforms and products, and the collection of personal data. Given how much data these tech giants collect, it would be interesting to see what the ACCC discovers.

In an attempt to address anti competition concerns expressed by Britain’s Competition and Markets Authority (CMA) Microsoft said it would license Activision Blizzard (NASD:ATVI) games to Sony (NYSE:SONY) for 10 years. This arrangement is similar to the one recently signed by Nvidia and Nintendo (OTCM:NTDOY). The CMA and Sony have suggested Microsoft needs to sell Activision’s top selling game, Call of Duty.

Microsoft is working with GM to investigate the possibilities of integrating Microsoft’s ChatGPT artificial intelligence into GM’s vehicles. The bot could be used to help owners with vehicle features that are usually outlined in owner’s manuals.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Royal bank of Canada (TSX:RY)

US $

Microsoft Corp. (NASD:MSFT)

Quarterly Reports

Enghouse

All currency listed in thousands of Canadian dollars.

Selected highlights from their first quarter 2023 financial results on March 9, 2023

- Revenue of $106,435 for the three months ended January 31, compared to $111,102 for the same period in 2021. A decrease of over 4%.

- Net income of $17,023 for the three months ended January 31, compared to net income of $21,597 in the same period in 2021.

- Diluted earnings per ordinary share of $0.31 for the three months ended January 31, compared to earnings per share of $0.39 for the same period in 2021.