This past week, the US Federal Open Market Committee (FOMC) convened to set monetary policy, most notably the US benchmark interest rate. These decisions have a profound influence on investors in both Canada and the United States. Generally, lower interest rates can lead to higher stock prices and a calmer market environment, and happier investors 😊. Conversely, higher rates can introduce volatility and encourage a shift towards more conservative investments.

Beyond investor sentiment, the FOMC’s decisions on the US benchmark interest rate can significantly influence the actions of the Bank of Canada (BoC) with regards to Canada’s interest rate. The relationship between these rates is critical because a substantial difference can have several repercussions on the Canadian economy.

For instance, if Canadian rates fall significantly below US rates, the Canadian dollar could weaken. This depreciation makes US imports—coming from Canada’s largest trading partner—more expensive, potentially driving up inflation in Canada, which is exactly what the BoC aims to prevent. Additionally, a wider interest rate gap might encourage investors to shift their money to the US in search of better returns, which could further weaken the Canadian dollar.

Given these dynamics, the BoC must approach rate adjustments with caution. They might lower the rate as early as June, then pause in July to assess whether inflation continues to decrease. Depending on economic indicators, further cuts could be considered, or rates might remain unchanged until inflation resumes its downward path.

Just as it is important to understand what the BoC decides about Canada’s interest rates, it is equally important to keep an eye on what the Fed does with American interest rates. Understanding these interactions can help you grasp how international economic policies influence markets and investment decisions.

So, let’s see what the Fed decided to do, how the markets reacted, and what else happened this past week….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, What are stocks, actually?, .…

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Gross Domestic Product (GDP)

Statistics Canada reported that GDP grew by 0.2% in February, a decrease from the revised growth of 0.5% in January and below analyst predictions of 0.3% growth. Over the past year, the Canadian economy has expanded by 0.8%.

In February, services-producing industries saw a growth of 0.2%, led by a 0.5% increase in ‘Accommodation and food services,’ while the ‘Transportation and warehousing’ sector showed significant annual increase of 4.9%. The goods-producing sectors, however, were flat for the month, with gains in ‘Mining, quarrying, and oil and gas extraction’ (up 2.5%) offset by declines in ‘Utilities’ (down 2.6%). Annually, goods-producing industries contracted by 1.6%, with the largest decline noted in the ‘Construction’ sector (down 3.3%).

The preliminary estimate for GDP growth in March remained unchanged at 0.2%, leading to an advanced estimate of 0.6% growth for the first quarter. Analysts are forecasting a yearly growth rate of 2.5%, with official estimates for March and the first quarter due on May 31.

With the economy slowing and inflation declining, market analysts anticipate a potential interest rate cut by the BoC in June. However, a strong American economy may delay adjustments to US rates. A widening gap between Canadian and American interest rates could lead to a depreciation of the Canadian dollar, raising import costs and potentially driving inflation higher. This scenario could also encourage capital to flow from Canada to the US in search of higher returns. While a weaker Canadian dollar might enhance export competitiveness, it could also increase the cost of imports, adding to inflation pressures. The BoC must carefully balance these factors to stabilize the currency, manage inflation, and support economic growth.

GDP, the total value of all goods and services produced within a country, is a crucial indicator of economic health. An increasing GDP typically signals growing wealth and opportunities, improving living standards, while a declining GDP may indicate economic difficulties such as rising unemployment or reduced consumer spending.

Canadian market volatility

Over the past week, Canada’s Volatility Index (VIXC), measured by the TSX 60 VIX, dropped from 13.67 to 12.64. This decrease in volatility is likely due to a combination of factors, including continued strong corporate earnings, easing tensions in the Middle East, and increased chances that the BoC will lower interest rates in June.

Often referred to as Canada’s ‘fear gauge,’ the VIXC provides insights into expected volatility within the Canadian stock markets. Typically, readings above 20 signify high volatility, while those below 20 indicate lower levels. With the current reading at 12.64, it suggests that the market remains well below the threshold for high volatility.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open Market Committee (FOMC)

In a unanimous decision, the Fed announced after its two-day FOMC meeting that it would maintain the current interest rate at 5.5%, marking the sixth consecutive hold since July 2023.

Recent data has consistently shown that the economy, job market, and consumer spending are all holding up well, while unemployment remains low. While these factors indicate a positive economic outlook, they are also contributing to persistent inflation, which remains above the committee’s 2% target. In the post meeting press conference, Fed Chair Jerome Powell said, “there has been a lack of further progress towards the committee’s 2% inflation objective,” signalling interest rates would remain higher for longer.

He downplayed recent speculation about a potential rate hike, suggesting it is “unlikely” to be the next policy move. Given the strong economic fundamentals, the Fed seems willing to wait for inflation to cool naturally rather than force it down with aggressive rate increases. However, Mr. Powell cautioned that it will likely take “longer than previously expected” for inflation to reach the target, revising his initial projections for the year. While he expects inflation to decrease by year-end, he expressed less confidence than earlier in 2024. The Fed Chair did not commit to a rate cut this year, emphasizing that future decisions would be based on incoming economic data.

Labour data

Each month, three labour market reports provide a snapshot of the current state of the American economy. Analyzing the latest data from the Job Openings and Labor Turnover Survey (JOLTS), ADP National Employment Report, and the Employment Situation Report (ESR) provides a comprehensive view of the US labour market and reveals key trends in employment, and wage growth that can influence future economic policy.

Department of Labor’s Job Openings and Labor Turnover Survey (JOLTS)

The latest JOLTS report from the Department of Labor shows a decline in job openings, down to 8.5 million in March from an upwardly revised 8.8 million in February, falling short of the 8.6 million analysts had forecasted. The job openings rate, which measures openings as a percentage of total employment plus openings, decreased to 5.1% in March after holding steady at 5.3% since December. Compared to the same month last year, when the rate was 5.8%, this year’s rate reflects a decrease to 5.1%.

The continued decline in job openings to a three-year low stems from factors such as businesses filling open positions or a downturn in labour demand, potentially indicating an economic slowdown or a reduction in business activities, thus signaling a cooling economy.

ADP Employment Report

The ADP National Employment report for April showed that private payrolls rose by 192,000, slowing down from an upwardly revised 208,000 in March. Analysts had forecast an additional 175,000 jobs. Pay increases remained steady at 5% for those who remained in the same job, although wage growth for job changers dipped slightly, from 10.1% in March to 9.3%, although it remained higher than at the start of 2024. The higher-than-expected private sector employment suggests the job market remains strong, potentially contributing to persistent inflation.

Bureau of Labor Statistics’ Employment Situation Report (ESR).

The Labor Department’s April ESR revealed that nonfarm payrolls increased by 175,000, a decrease from the 303,000 jobs added in March and significantly below analysts’ expectations of 243,000. This marks the smallest job growth in six months. The unemployment rate rose slightly to 3.9% from March’s 3.8%, surpassing analysts’ forecasts of remaining steady at 3.8%. Average hourly earnings in April increased by 0.2% on a monthly basis, consistent with March’s growth. Annually, the average monthly nonfarm payroll additions shrunk by 37% compared to April 2023’s figure of 278,000. Meanwhile, the unemployment rate rose by 0.1% year-over-year, and wages grew by 3.9%.

This report indicates a slowing job market, a slight increase in unemployment, and stable wage growth, which could reassure the Fed that the economy is cooling without overheating. These trends suggest that inflationary pressures are easing, potentially supporting a case for a future interest rate cut by the Fed.

Conclusion

A strong labour market often indicates a growing economy, which can lead to a positive cycle of consumer spending, business investment, and overall economic activity. When people are employed and feel secure in their jobs, they tend to be more confident about spending money. This can boost consumer spending, a major driver of economic growth. However, a strong labour market can also contribute to inflationary pressures because businesses must pay more to attract and retain workers. The higher labour costs are be passed on to consumers in the form of higher prices.

These three labour reports suggest that job openings and hirings are slowing, leading to a possible slowdown of the economy. The slowing wage growth is the likely result of employees having less leverage to negotiate for higher pay due to a potentially growing pool of unemployed individuals.

Overall, these trends collectively suggest that the labour market is cooling, which might relieve inflationary pressures. For the Fed, these conditions could justify contemplating rate cuts if the cooling trend continues and becomes more pronounced.

American market volatility

The CBOE Volatility Index (VIX), often referred to as the market’s fear gauge, ended the week at 13.49, down 10% from the previous week’s reading of 15.03, and its lowest level in over a month. This reduction in the VIX has been influenced by lower tensions in the Middle East, strong corporate earnings, and a slowing labour market, which could signal falling inflation. Typically, the VIX ranges from 10 to 20, with readings above 20 often associated with heightened volatility. While the current lower VIX suggests reduced investor anxiety in the near term, future economic data and global events could cause the VIX to fluctuate.

Consumer Confidence Index (CCI)

The Conference Board reported that the CCI for April unexpectedly fell to 97.0, down from a downwardly revised 103.1 in March. That was the third consecutive decline in consumer confidence, falling well below analysts’ expectations of 104.0.

The CCI consists of two components: the Present Situation Index (PSI) and the Expectations Index (EI). This month, the PSI saw a slight decrease, dropping to 142.9 from 146.8 in March. Meanwhile, the EI experienced a more significant fall, declining from 74.0 to 66.4. Notably, an EI below 80 often signals a potential recession on the horizon.

While consumers’ confidence in their current situation remains relatively stable, concerns about a slowing labour market and persistent inflation are raising concerns about the future economic climate.

The CCI is an important measure of economic sentiment, influencing the Fed’s interest rate decisions and market movements. Its components provide insights into the public’s perception of economic health, with the PSI highlighting current conditions and the EI offering a forward-looking perspective.

What are stocks, actually?

Stocks, commonly referred to as shares, represent ownership in a corporation. When you buy a stock, you’re buying a piece of that company, entitling you to a fraction of its assets and profits proportional to the amount of stock you own.

Corporations can raise capital in two primary ways: by issuing stocks or by borrowing money through bonds or loans. Each unit of stock is referred to as a “share.” While the terms ‘stocks’ and ‘shares’ are often used interchangeably, ‘stock’ can refer to overall ownership in one or more companies, whereas a ‘share’ signifies the smallest unit of that ownership.

Shares are primarily bought and sold on stock exchanges, such as the Toronto Stock Exchange, the New York Stock Exchange, or NASDAQ. Trading on these regulated exchanges ensures transparency and reduces the risk of fraudulent practices, safeguarding investor interests.

When you buy or sell shares, whether through a brokerage or a direct investing account, you will receive confirmation of the transaction. This confirmation details the number of shares you bought or sold and the price per share. It’s worth noting that today, it’s rare to receive a physical stock certificate as evidence of ownership since most records are kept electronically.

Shares of public companies like TD Bank (TSE: TD) and Apple (NASD: AAPL) are integral to many investors’ portfolios, representing a tangible link between personal finance and the broader economic landscape.

The Walt Disney Company (NYSE: DIS) stock certificates were once among the most sought-after because of their colorful designs featuring beloved Disney characters. These certificates were not only investments but also popular gifts from parents and grandparents eager to introduce children to the world of investing. On October 16, 2013, Disney ceased issuing these decorative paper stock certificates to shareholders. Although no longer available, Disney now offers ‘certificates of acquisition’ upon request, which carry no monetary value but maintain the tradition for collectors and fans.

Weekly Market Review

Monday: all four indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – got off to a good start, ending the day in the green. Investors are bracing for a week with more earnings reports, the latest interest rate from the Fed, and US labour data. Oil prices fell as tensions cooled in the mid east, easing supply concerns. More importantly, demand also fell as the latest data showed the Chinese economy, the world’s second largest, remained sluggish, and investors’ fear of higher for longer US interest rates. Lower rates would stimulate economic growth and demand for oil.

In Canada, the TSX was lifted by higher commodity prices. In trading, Utilities and Basic Materials (miners and fertilizer manufacturers) had the biggest gains, while Industrials and Financials were the only two sectors to end lower.

In the US, investors are bracing for what the Fed has to say about future rate cuts and how deep the cuts will be. In trading, Utilities and Consumer Cyclicals advanced the most, while Technology was the only sector to end lower.

Tuesday: it was a red wave across the markets today as all four indexes ended sharply lower. The US Employment Cost Index report showed higher than expected wages and benefits for the first quarter of 2024. Rising wages tend to keep upward pressure on inflation as consumers have more money to spend.

In Canada, lower commodity prices and concerns the Fed will delay rate cuts drove the TSX lower. In trading, Healthcare and Telecommunications were the only sectors to end in the green. Basic Materials and Energy suffered the steepest declines.

In the USA, consumer confidence fell to its lowest point since July 2022 as consumers grew more concerned about future business conditions. All three indexes were sharply lower, complete with a last-minute plunge that saw the Nasdaq end the day 2% lower than it started. The DJIA and S&P were only slightly better, down 1.49% and 1.57%, respectively. In trading, it was a sea of red with all sectors losing ground. Healthcare and Consumer Cyclicals lost the least while Energy and Basic Materials lost the most.

Wednesday: after being down all morning, the markets surged after the Fed’s latest rate announcement, before falling back in the final hour. As well as maintaining the US rate at 5.5%, Fed Chair Powell indicated more work needed to be done to bring inflation lower. Oil prices plunged on news of an unexpected rise in US inventories.

In Canada, the TSX ended the day in the green, boosted by news from the Fed that the next rate decision will likely be a cut. In trading, the Telecommunications Services and Technology gained the most, while Healthcare and Energy suffered the biggest drops.

In the US, the more interest sensitive S&P and Nasdaq both ended in the red, while the DJIA was able to stay in the green. As well, the number of job openings fell to a three-year low, suggesting the labour market was cooling. In trading, Utilities and Healthcare rose the most, while the Energy and Technology sectors fell the farthest.

Thursday: after yesterday’s roller coaster like ride, the markets rallied with all four indexes ending firmly higher. Investors were feeling upbeat after the Fed’s less hawkish guidance on interest rates, feeling that rates cuts this year are still a possibility.

In Canada, overall investor sentiment and the growing likelihood the BoC will lower the interest rate in June lifted the TSX into the green. In trading, Industrials and Consumer Staples posted the biggest gains, while Healthcare and Telecommunications Services ended the deepest in the red.

In the USA, all three indexes ended in the green as investors await tomorrow’s jobs report to get an idea how the American economy is doing. It was a good day in trading, led by the Consumer Cyclicals and Technology sectors. Healthcare and Telecommunications Services were the only two sectors to end in the red.

Friday: the indexes all rose after a weaker than expected US labour report raised hopes for a cut to the US benchmark interest rate. Oil prices were down sharply on concerns delayed interest rate cuts could hamper consumer demand. Oil prices posted their worst weekly loss in three months.

In Canada, the TSX was lifted by investor optimism resulting from the good news out of the US. In trading on Bay Street, it was a day of broad-based gains led by the Technology and Telecommunications Services sectors. The Healthcare and Consumer Cyclicals were the only sector to end in the red.

In the USA, following today’s labour report, all three indexes gained at least 1% today. Investors are now speculating that the Fed could lower rates as soon as September, with possibly two cuts this year. In trading on Wall Street, all sectors ended higher, led by the Technology and Utilities sectors. Trailing the pack were Energy and Healthcare.

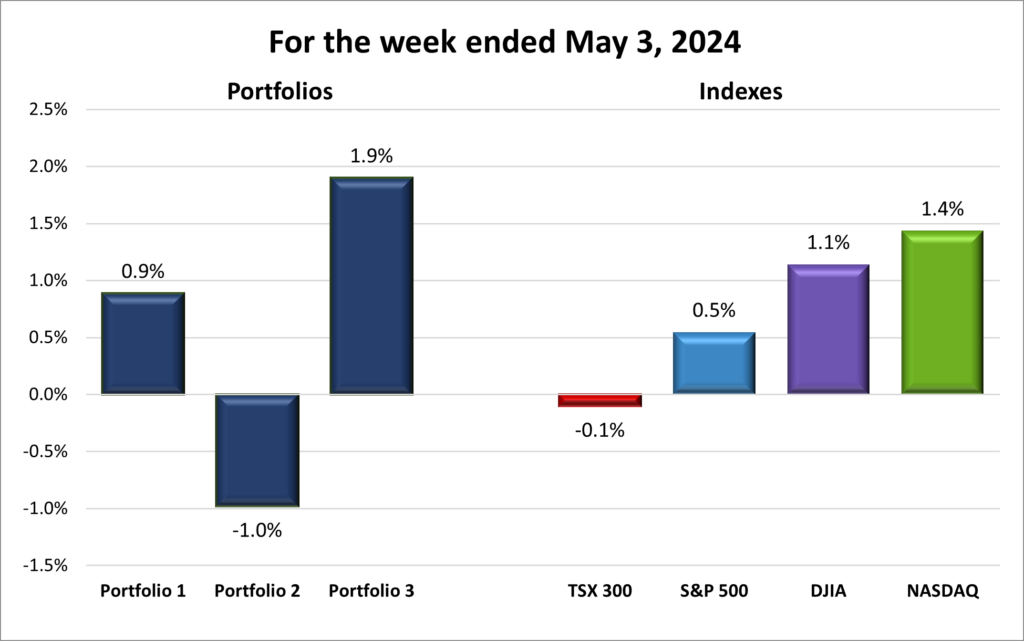

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) slipped 0.1%, the S&P 500 (SPX) added 0.5%, the DJIA (INDU) advanced 1.1% and the Nasdaq (CCMP) surged 1.4%.

| Index | Weekly Streak |

| TSX: | 1 – week losing streak |

| S&P: | 2 – week winning streak |

| DJIA: | 3 – week winning streak |

| Nasdaq: | 2 – week winning streak |

![]() Another positive week unfolded for markets, at least the American markets, buoyed by strong earnings and a rise in investor sentiment. Despite a rocky start due to diminished hopes for a rate cut this year—a stark reversal from earlier expectations—the markets rebounded impressively by week’s end. Initially, a rise in US labour costs, which might prompt the Fed to maintain higher interest rates to combat inflation, rattled investors. These concerns were compounded by data showing robust wage growth and a strong economy, seemingly reducing the justification for the anticipated rate cuts.

Another positive week unfolded for markets, at least the American markets, buoyed by strong earnings and a rise in investor sentiment. Despite a rocky start due to diminished hopes for a rate cut this year—a stark reversal from earlier expectations—the markets rebounded impressively by week’s end. Initially, a rise in US labour costs, which might prompt the Fed to maintain higher interest rates to combat inflation, rattled investors. These concerns were compounded by data showing robust wage growth and a strong economy, seemingly reducing the justification for the anticipated rate cuts.

Mid-week developments shifted market sentiment. During the FOMC meeting, the Fed announced they were holding the US benchmark interest rate at 5.5% to ensure inflation kept moving downwards to their 2% target. This marked the sixth consecutive hold on the rates. However, it was Fed Chair Jerome Powell’s indication that further rate hikes were less likely, stating, “it is unlikely the next policy move will be a hike,” that spurred a market rally, propelling the major American indexes into positive territory for the week, with the TSX just narrowly missing out.

At the end of the week, US labour data for April revealed signs of a cooling labour market, with fewer job openings and a slight increase in unemployment. This slowdown might be unwelcome news for workers, but it provides a glimmer of hope for those anticipating potential interest rate cuts in the third quarter.

In Canada, the TSX stumbled at the start of the week amid falling commodity prices. However, following the Fed’s announcement, which reduced the likelihood of a US rate hike, there was an increased probability that the BoC might lower its rate at their next meeting in June. The Fed holding the rate at the current level, and possibly lowering the rate in September, would allow the BoC to lower the Canadian rate without diverging too far from the US rate.

Overall, the week ended on a positive note. The three American indexes closed the week higher and all four major North American indexes ended the week with upward momentum. Hopefully, that momentum will carry forward through next week, though no one ever knows what can influence the markets. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week winning streak |

| Portfolio 2: | 1 – week losing streak |

| Portfolio 3: | 2 – week winning streak |

![]() If you take a look at the chart below, you can see it was a mixed week for my three portfolios. Portfolios 1 and 3 successfully extended their respective winning streaks, while Portfolio 2 was unable to join them in the win column this past week.

If you take a look at the chart below, you can see it was a mixed week for my three portfolios. Portfolios 1 and 3 successfully extended their respective winning streaks, while Portfolio 2 was unable to join them in the win column this past week.

Portfolio 1 saw a modest net gain, despite mixed individual performances. Fortunately, significant (over 10%) gains from Pinterest (NYSE: PINS) up 18%, Decisive Dividend Corp (TSEV: DE) up 11%, and Innovative Industrial Properties (NYSE: IIPR) up 10% compensated for the significant losses recorded by Cloudflare (NYSE: NET) down 16%, and Skyworks Solutions (NASD: SWKS) down 12%.

Portfolio 2 experienced an overall decline, despite most companies showing minor gains. A standout 19% increase in Brookfield Renewable Corp (TSE: BEPC) was overshadowed by a 23% fall in Hammond Power Solutions (TSE: HPS.A). With no specific news to explain the steep decline, it appears to be a pullback after a recent post-earnings run-up, possibly as investors took profits.

Portfolio 3 had a strong week, outperforming both the other portfolios and all four indexes. While most stocks hovered around the baseline, significant gains in Brookfield Renewable Corp and Brookfield Renewable Partners LP (TSE: BEP.UN), both up 19%, amply offset the sharp drop in Cloudflare.

This past week was not as good as the previous week when all three portfolios increased in value, but as Meatloaf used to sing, “Two out of three ain’t bad.” 😊

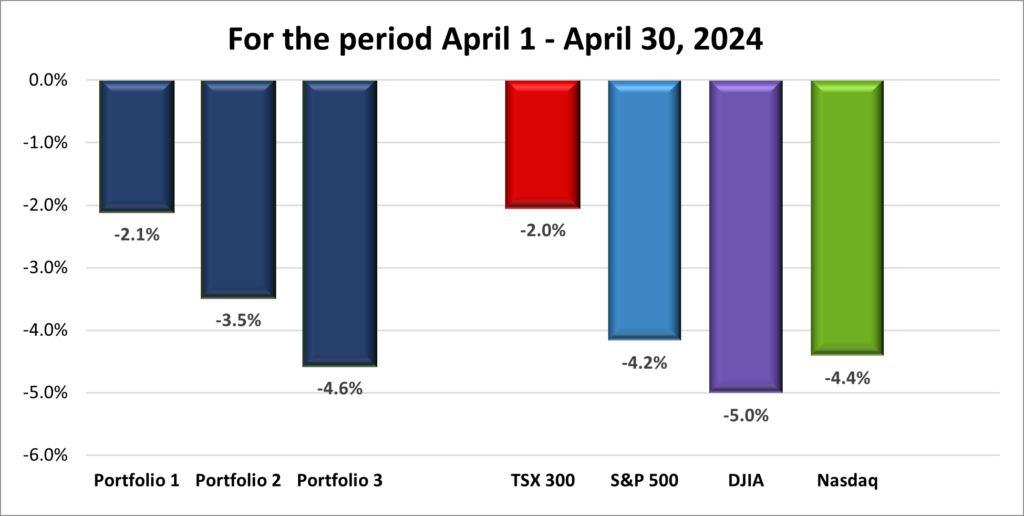

Monthly Market and Portfolio Review

For the month, the TSX (SPTSX) fell 2.0%, the S&P 500 (SPX) declined 4.2%, the DJIA (INDU) plunged 5.0% and the Nasdaq (CCMP) dropped 4.4%.

![]() At the end of March, I optimistically predicted that April could kick off a bull run. I could not have been more off the mark! Once again, the markets reminded me of the folly in forecasting their movements.

At the end of March, I optimistically predicted that April could kick off a bull run. I could not have been more off the mark! Once again, the markets reminded me of the folly in forecasting their movements.

April turned out to be the most challenging month of 2024 so far. Despite the promising momentum from the first quarter, the indexes started a downward trajectory right from the start of April, with only a brief rebound last week. As shown in the accompanying chart, the downtrend was persistent through most of the month.

In the US, strong economic and labour market data for March and April was great for workers but complicated the Fed’s efforts to bring inflation down to their 2% target. Persistent inflation heightened investor anxieties, overshadowing an otherwise strong earnings season. At the year’s start, there was chatter about imminent rate cuts and a potential ‘soft landing’—an economic slowdown where inflation targets are met without triggering a recession. By the end of April, with inflation stubbornly sticking around 3% due to a strong labour market fueling consumer spending, the narrative shifted dramatically. Talk of ‘higher-for-longer’ interest rates resumed, with speculation on when the Fed might begin to lower rates.

In Canada, the economic picture was mixed. Inflation hovered just below 3%, and a weakening job market led the BoC to state that a June rate cut might be possible. However, a potential rate cut and rising commodity and oil prices this were not enough to offset the economic news from the US, causing the TSX to snap a five-month streak of monthly gains.

At the end of the month, strong quarterly earnings helped all four indexes post a weekly gain simultaneously for the only time in April. Unfortunately, not all months can be bullish months for the markets, and April was certainly one of those months. ☹

![]() April saw few highlights, with all three portfolios declining in value as shown in the chart below. Apart from the last full week of the month, the portfolios mostly recorded weekly losses.

April saw few highlights, with all three portfolios declining in value as shown in the chart below. Apart from the last full week of the month, the portfolios mostly recorded weekly losses.

Portfolio 1 was the best performer of the three, though it still lost over 2%. Nvidia (NASD: NVDA) had a volatile month, ending with a 4% loss. Given its significant weight—over 40% at the beginning of the month—the movements in Nvidia’s share price had a major impact on the portfolio. Semiconductor stocks, in general, faced a tough month.

Portfolio 2 had a lone bright spot with its energy companies performing well amidst the overall downturn.

April was a dismal month for Portfolio 3, dropping more than the others, but it still outperformed the DJIA. 😊 The standout here was Alvopetro Energy (TSEV: ALV), which surged over 18%.

Companies on the Radar

This past week, no new companies caught my attention. For now, I am content with the four companies listed below.

This past week, no new companies caught my attention. For now, I am content with the four companies listed below.

- Equitable Bank (TSE: EQB), a mid sized Canadian bank, considered Canada’s 7th bank, that provides financial services to consumers and businesses.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies, and then strengthens and grows those companies.

- LVMH Moët Hennessy – Louis Vuitton, Société Européenne (OTCM: LVMUY), commonly known as LVMH, is a French multinational conglomerate specializing in luxury goods. It is the world’s largest luxury goods company.

- Evolution AB (OTCM: EVVTY), a Swedish company that provides live casino solutions for global gaming operators.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated May 3, 2024.

NOTE: Morningstar and Thomson-Reuters analysis is unavailable for Evolution and LVMH from my usual sources because the company’s home stock exchange is in Europe. While it is possible to invest in both companies through the Over-the-Counter Market, I do not have access to analysis similar to the data available for companies traded on the major North American stock exchanges (Toronto Stock Exchange, New York Stock Exchange, and Nasdaq Stock market). The Analysts Rating and Price Target for these two companies are from Yahoo! Finance, under the Analysis tab once you have searched for the ticker.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended May 3, 2024: UP ![]()

- Apple’s iPad operating system, iPadOS, has been designated a ‘gatekeeper’ by the European Union’s (EU) anti trust regulator, the European Commission (EC). The EC defines a ‘gatekeeper’ as a platform that acts as an important ‘gateway’ between businesses and consumers in the EU. This means they have a dominant position that could potentially restrict competition.

At Apple’s quarterly earnings report, the company announced a 4% increase to their dividend, and added US$ 110 billion to their share buyback program. Both are shareholder friendly actions and take the sting out of a weak earnings report. - Alphabet’s (NASD: GOOGL) Google plans to invest a total of US$ 3 billion to build a data centre in Indiana and expand existing facilities in Virgina. The build out is to support the increasing demand for artificial intelligence (AI) services on their Google Cloud cloud computing platform.

- CrowdStrike (NASD: CRWD) announced the had been named the overall leader in cybersecurity threat protection in the KuppingerCole’s Leadership Compass, Identity Threat Detection and Response (ITDR) 2024 report. Always good to see a company you invested in to be considered the best in its field. 😊

CrowdStrike and Amazon (NASD: AMZN) announced Amazon has consolidated its cybersecurity protection on CrowdStrike’s platform to protect Amazon Web Services platforms and data. In return, CrowdStrike will increase its use of AI and other services on AWS’s platform. - Walmart (NYSE: WMT) announced a new private label food brand called ‘bettergoods’ that would see most products sell for under US$ 5.00. Products under this new brand would include dairy products, snacks, soups, and other basic food items across 50 categories.

- Carnival Cruise Lines (NYSE: CCL) announced their Princess’s fleet has revised the routes and itineraries of its two planned global cruises. Due to geopolitical uncertainties in the Middle East the ships will no longer visit that region, instead they will visit go around South Africa rather than through the Suez Canal.

- Cameco (TSX: CCO) projects a growing demand for clean energy as a result of the growing demands from the growth of power-hungry data centres and an increasing number of electric vehicles (EV) on the roads. Nuclear energy could be a major source of dependable, carbon free energy to meet the growing demands.

- Rivian Automotive (NASD: RIVN) received an incentive laden cash deal from the state of Illinois to expand its production capabilities at its Normal, IL factory. Rivian produces its electric vans and their new R2 SUV at this location.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Toronto-Dominion Bank (TSE: TD) DRIP

Bank of Nova Scotia (TSE: BNS) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Lattice Semiconductor Corporation

First quarter 2024 financial results on April 29, 2024

Pinterest, Inc.

First quarter 2024 financial results on April 30, 2024

Skyworks Solutions, Inc.

Second quarter 2024 financial results on April 30, 2024

Cameco Corporation

First quarter 2024 financial results on April 30, 2024

PayPal Holdings, Inc.

First quarter 2024 financial results on April 30, 2024

Amazon.com, Inc.

First quarter 2024 financial results on April 30, 2024

Andlauer Healthcare Group Inc.

First quarter 2024 financial results on May 2, 2024

TMX Group Limited

First quarter 2024 financial results on May 2, 2024

BCE Inc.

First quarter 2024 financial results on May 2, 2024

Apple Inc.

Second quarter 2024 financial results on May 2, 2024

Trisura Group Ltd.

First quarter 2024 financial results on May 2, 2024

Cloudflare, Inc.

First quarter 2024 financial results on May 2, 2024

Portfolio 2

Portfolio 2 for the week ended May 3, 2024: DOWN ![]()

- The bank of Nova Scotia (TSE: BNS) announced Travis Machen as the CEO and group head of its global banking and markets unit. He will be responsible for expanding the bank’s products and services and increasing high value clients.

- At its MongoDB.local developer conference, MongoDB, Inc. (NASD: MDB) announced the general availability of MongoDB Atlas Vector Search on Knowledge Bases for Amazon Bedrock. This new offering allows organizations to build generative AI application features using fully managed foundation models more easily.

- Canadian Natural Resources (TSE: CNQ) announced they are seeking opportunities to substantially increase the crude oil output at their primary oil sands mine in northern Alberta.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Bank of Nova Scotia (TSE: BNS) DRIP

TC Energy Corp (TSE: TRP)

Dollarama Inc. (TSE: DOL)

US $

No US$ dividends this past week.

Quarterly Reports

Fortis Inc.

First quarter 2024 financial results on May 1, 2024

Canadian Natural Resources Limited

First quarter 2024 financial results on May 2, 2024

Brookfield Renewable Partners L.P.

First quarter 2024 financial results on May 3, 2024

TC Energy Corporation

First quarter 2024 financial results on May 3, 2024

Portfolio 3

Portfolio 3 for the week ended May 3, 2024: UP ![]()

- Microsoft (NASD: MSFT) announced they plan to spend US$ 1.7 billion over the next four years in Indonesia as part of building out their infrastructure to support the expansion of their cloud computing and AI services.

- Brookfield Asset Management (TSX: BAM), Brookfield Renewable and Microsoft jointly announced a global renewable energy framework agreement. For Microsoft, they have secured a tremendous amount of renewable energy at a time when it is in short supply. The deal will help Microsoft achieve its goal of reaching zero carbon energy emissions by 2030 as it meets the growing energy demands for its expanding cloud computing and AI infrastructure. For Brookfield, the benefit is that Microsoft is committing to buying the 10.5 gigawatts of renewable energy capacity this project will eventually produce at the prevailing market prices. Brookfield Renewables can now make the necessary investments without worrying about having to sell the energy.

- TD Bank was fined C$ 9.2 million by the Canada’s anti-money laundering agency – Financial Transactions and Reports Analysis Centre of Canada (FINTRAC). The agency said it discovered non-compliance of anti – money laundering regulations. If that was not bad enough, the US Department of Justice is investigating how Chinese drug traffickers used TD to launder the proceeds from the sale of fentanyl. As well as significant fines, up to US$ 1 billion, TD could face regulatory limitations on its business activities. Ouch! ☹

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Toronto-Dominion Bank (TSE: TD)

US $

No US$ dividends this past week.

Quarterly Reports

Cloudflare, Inc.

See report under Portfolio 1.

Brookfield Renewable Partners L.P.

See report under Portfolio 2.