Will October be Trick or Treat for Investors?

After an unusually strong September, we’re stepping into the witching month – a time with a well-earned reputation for market drama. October has long carried a spooky aura on Wall Street, and for good reason. It’s seen some of the biggest market crashes in history. The Great Crash of 1929 kicked off the Great Depression after years of speculation and margin buying came undone, sending the Dow Jones Industrial Average (DJIA) tumbling nearly 90% from its peak and taking 25 years to fully recover. In 1987, “Black Monday” struck when computer-driven trading and panic selling triggered a record one-day drop of 22.6%, though markets managed to rebound within two years. It remains one of the worst single-day declines in Canadian market history. And in 2008, the collapse of the American housing market and the global credit freeze sent the S&P 500 (S&P) plunging 57% and the Toronto Stock Exchange (TSX) dropped about 16%, with a full recovery taking about four years.

Yet despite those infamous moments, October isn’t the market villain it’s often made out to be. Historically, it’s been more of a turning point – a month when markets often rebound after September’s weakness. Some even call it the “bear killer,” since several recoveries have started right around this time. But when September’s been strong, like this year, October tends to act more like a pause button than a launchpad, as investors catch their breath before the final stretch of the year.

For Canadian investors, the story isn’t much different. The TSX has often followed the same seasonal rhythm as American markets – sluggish through September, then stronger into year-end – though swings in energy and materials prices can make the ride bumpier. When oil prices firm up heading into winter, the TSX has historically gotten an extra lift, especially from its heavyweight energy and mining names.

Looking past October, the fourth quarter has traditionally been one of the best stretches for investors. Strong holiday spending, year-end portfolio rebalancing, and a generally upbeat mood have helped make the fourth quarter the most consistently positive period for the S&P, averaging gains of about 4% to 5% over time. So, while October’s history may raise eyebrows thanks to a few dramatic moments, both October and the fourth quarter have been kind to investors overall. Seasonality isn’t guaranteed, of course – but history still leans in favour of the bulls as we head toward year-end. Let’s hope that trend continues. 😊

So, with all that history in mind, how did markets actually behave this past week? After a strong September, investors were watching closely to see whether the momentum would continue, or if October would live up to its scary reputation. Let’s take a closer look at how the witching month has kicked off for markets so far.

Items that may only interest or educate me ….

The Bull Turns 3, Canadian Economic news, US Economic news ….

The Bull Turns 3

October 12, 2025, marks the third anniversary of the current bull market – a milestone that might surprise anyone who remembers how gloomy things felt back in 2022. I still remember that bear market (when stocks fell more than 20% from their highs), watching my portfolios drop week after week was not fun. A bull market, by contrast, means stocks have been rising for an extended period, usually by 20% or more from their lows.

The market hit rock bottom on October 12, 2022, when the S&P sank to its lowest point after months of surging inflation, soaring interest rates, and recession fears. From that low, the market has come roaring back, with the S&P surging nearly 90% and the TSX climbing almost 64% over the past three years.

Much of that rally has been driven by the heavyweight technology companies – the “Magnificent 7” – and the explosive growth of artificial intelligence (AI). What started as a niche tech story has become a full-blown market catalyst, drawing in investors and sending share prices soaring. Not bad for a bull market that began when optimism was in short supply. 😊

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Labour Force Survey (LFS)

According to Statistics Canada, the Canadian economy added 60,400 mostly full-time jobs in September, far exceeding expectations for just 5,000 and nearly offsetting August’s loss of 65,500. The unemployment rate held steady at 7.1%, defying forecasts for a small uptick to 7.2%, which suggests more people are entering the workforce rather than leaving it.

The biggest job gains came from the agriculture industry, which jumped 6.1% for the month, while wholesale and retail trade, along with transportation and warehousing, saw declines of 0.7%. On a year-over-year basis, employment in utilities surged 10.4%, while business, building, and other support services dropped 3.5%.

Wage growth remains moderate, with average hourly earnings rising 3.3% from a year ago, slightly higher than August’s 3.2%. Youth unemployment, however, climbed to 14.7%, showing younger workers are still having a tough time landing steady jobs.

All in all, September’s report showed surprising strength in Canada’s labour market, signalling resilience despite broader economic headwinds. But with rising wages and uneven job growth across sectors, the BoC will likely stay cautious as it weighs inflation risks going forward.

Canadian Market Volatility

Canada’s volatility gauge, the S&P/TSX 60 Volatility Index (VIXC), opened the week at 11.50 and stayed mostly calm, hovering around the 12 mark. But on Friday, it spiked as high as 19.25 after a stronger-than-expected labour report, confirmation that sector-specific US tariffs will remain in place, and, most importantly, renewed US threats of a massive tariff hike on China, which was the main driver of the late-week jump. The index later eased to finish the week at 11.55 as markets shook off the initial shock from the China tariff news.

For anyone new to it, the VIXC is basically a barometer of investor nerves in Canada. When it’s in the single digits or low teens, markets are calm. But once it moves into the mid-teens or higher, it signals growing unease and the potential for choppier trading ahead. Even with Friday’s spike, the index ended near the lower end of its normal range – suggesting that, for now, Bay Street remains more relaxed than rattled.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

The shutdown, which began on October 1, has delayed several key government economic data releases. Among the data delayed is this week’s Bureau of Labor Statistics’ Employment Situation Report, more commonly known as the monthly jobs report. Updates will start again when the Federal government resumes operations.

Federal Open Market Committee (FOMC) minutes

The Fed released the minutes from its September 16–17 meeting this week, giving investors a closer look at what policymakers were thinking when they decided to cut interest rates by a quarter point. Most members supported the move, though a few preferred a larger 0.5% cut. Others were more cautious, still concerned that inflation hadn’t cooled enough to justify moving too quickly. The split shows that while the Fed is leaning toward more rate cuts, it’s not in a hurry to rush down that path.

The minutes also revealed growing concern about the labour market. Officials noted that hiring has slowed, job gains have come in weaker than expected, and the risks to employment are starting to tilt to the downside. That cooling job market is one of the main reasons the Fed opted to cut rates in the first place – lower borrowing costs can help keep businesses investing and hiring.

Inflation, however, is still a sticking point. While some members felt price pressures had begun to ease, others warned that risks haven’t gone away, especially with higher input costs and tariffs still in play. This ongoing tug-of-war between inflation and slowing growth has left the Fed in a tough spot – trying to support the economy without reigniting price pressures.

For us investors, the takeaway is that the Fed remains cautious but open to adjusting rates as needed. The committee sees room for further cuts if the economy weakens, but with inflation still hovering above their 2% target and key data delayed by the government shutdown, the path forward is uncertain. Markets will likely see a few more twists and turns before the Fed’s next move comes into focus.

Consumer Sentiment Index (CSI)

The University of Michigan’s preliminary October CSI came in at 55.0, just a touch above expectations (54.2) and virtually unchanged from September’s final reading of 55.1. Compared to a year ago, though, sentiment has dropped 22%, showing how much confidence has cooled over the past year.

The Current Economic Conditions Index, which reflects how people feel about their job security and personal finances, ticked up 1.0% month over month to 61.0, though it’s still down 6.0% from a year ago. Meanwhile, the Expectations Index, which looks six months ahead, slipped 1.0% to 51.2, down a hefty 30.9% year over year.

On the inflation front, short-term expectations (one year ahead) eased slightly to 4.6% from 4.7%, while the five-year outlook held steady around 3.7%.

Consumer sentiment offers a glimpse into how everyday Americans feel about the economy, and that can shape spending, borrowing, and corporate earnings. This month’s steady reading suggests confidence isn’t improving, but it’s not falling off a cliff either. The small dip in inflation expectations gives the Fed a bit of breathing room, though worries about prices, wages, and the job market still linger.

In short, despite the US government shutdown entering its second week, consumers’ views didn’t shift much. Sentiment remains cautious – neither a big win nor a major warning sign – but Americans clearly haven’t shaken off their economic worries just yet.

American Market Volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” opened the week at 16.74 and stayed relatively calm through Thursday, hovering between 16 and 17. But it spiked above 22.2 after President Trump threatened massive new tariffs on Chinese goods following China added new port fees on American ships, launched an antitrust investigation into American technology company Qualcomm (NASD: QCOM), and slowed exports of rare earth minerals to the US. The VIX stayed above 20 for the rest of the day and ended the week at 21.66.

Think of the VIX as a market mood ring. When it’s in the 12–20 range, investors are generally calm. Once it climbs higher, it signals growing unease and the possibility of bumpier trading ahead. A rising VIX doesn’t always mean panic, but it does show caution creeping back into the market.

Weekly Market and Portfolio Review

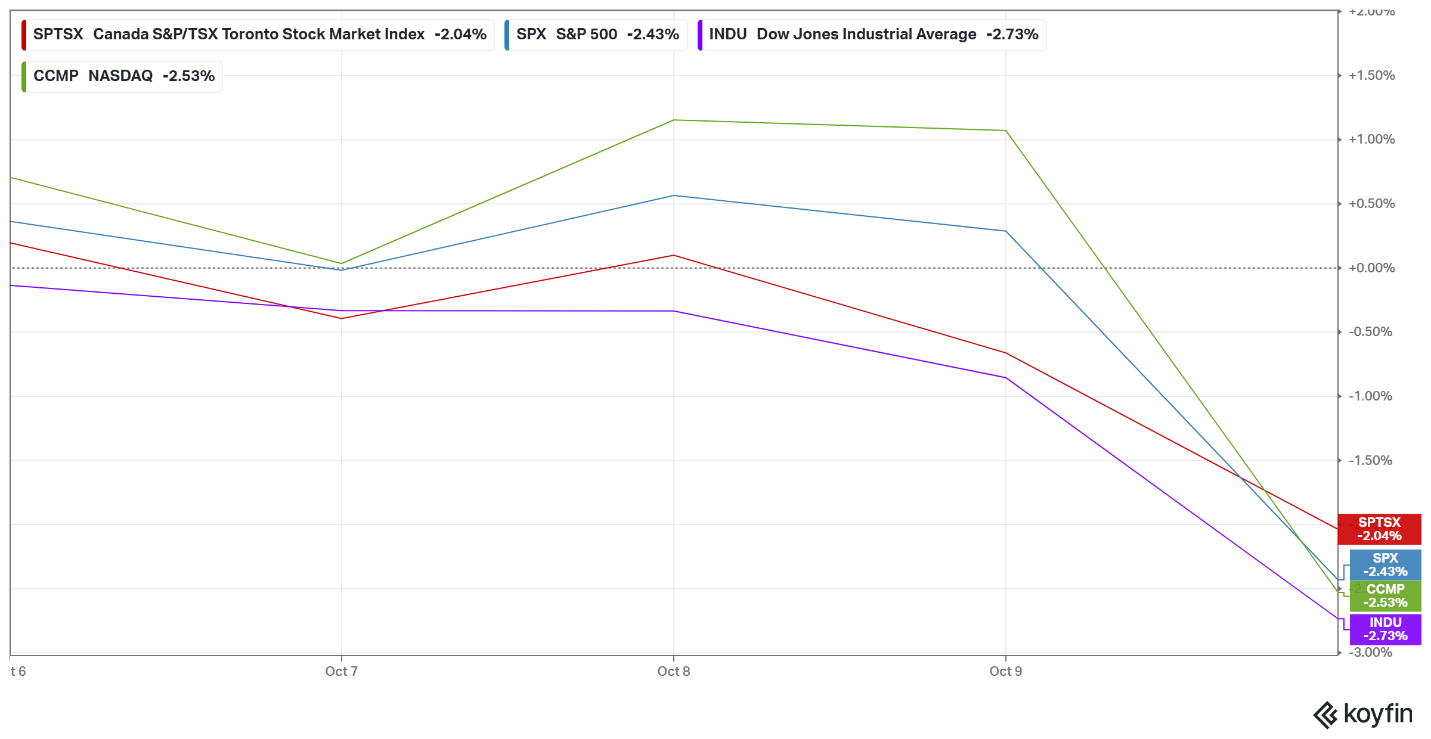

For the week, the TSX (SPTSX) lost 2.0%, the S&P (SPX) dropped 2.4%, the DJIA (INDU) fell 2.7% and the Nasdaq (CCMP) sank 2.5%.

| Index | Weekly Streak |

| TSX: | 1 – week losing streak |

| S&P: | 1 – week losing streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 1 – week losing streak |

![]() With no fresh economic data and earnings season about to kick off, investors spent most of the week in “wait and see” mode. Markets rode a rollercoaster, swinging between optimism and doubt before a last-minute plunge sent all four major indexes into negative territory for the week.

With no fresh economic data and earnings season about to kick off, investors spent most of the week in “wait and see” mode. Markets rode a rollercoaster, swinging between optimism and doubt before a last-minute plunge sent all four major indexes into negative territory for the week.

At the start of the week, the TSX, the S&P, and the Nasdaq Composite (Nasdaq) all extended their daily win streaks to seven before running into a wall of doubt over AI’s profitability. From there, the indexes seesawed between gains and losses – and, like any good rollercoaster, ended with a steep drop. The TSX, S&P, and Nasdaq each logged their biggest single-day declines since April. On a weekly basis, the S&P posted its sharpest loss since May, while both the TSX and Nasdaq saw their steepest declines since April. And in case you thought the DJIA escaped the pain, it finished lower every day of the week and plunged more than 800 points, or 1.9%, on Friday alone. Ouch!

Among the biggest market drivers were the mega-cap tech companies riding the ongoing AI boom, the release of the FOMC meeting minutes, anticipation for next week’s earnings reports, and trade tariffs. Early in the week, chipmaker AMD (NASD: AMD) lit up the markets after announcing a multiyear deal with OpenAI – the maker of ChatGPT – to supply advanced AI chips. The agreement, expected to bring in tens of billions in annual revenue, also gives OpenAI the option to purchase up to 10% of AMD, fueling hopes that the AI rally still has momentum.

That optimism faded midweek after a report raised doubts about the profitability of renting out AI computing power. The news cooled enthusiasm and reignited concerns that the rapid run-up in AI stocks could be forming a bubble. With that uncertainty, investors turned their attention back to the Fed for guidance.

With the US government shutdown, into its tenth day (at the time of this post), the release of the FOMC minutes took centre stage. Markets initially rallied after learning most members felt it “would be appropriate to ease policy further over the remainder of this year,” with nearly half expecting three rate cuts in 2025 (the first came in September). With fresh data limited, investors are now eyeing earnings season for clues on the economy, while some have shifted toward safe-haven assets like gold.

On the trade front, for most of the week there wasn’t much news beyond President Trump announcing a new 25% tariff on all foreign-made medium and heavy-duty trucks. The calmness was shattered when Trump rattled markets by threatening a “massive increase” in tariffs on Chinese imports, responding to Beijing’s recent export controls on rare earth elements, the addition of new port fees on American ships, and launching an antitrust investigation into American technology giant Qualcomm. The escalation marks a major setback in trade relations between the world’s two largest economies, raising fears of renewed tensions, disrupted supply chains, and higher costs for consumers and businesses. The markets’ tumble underscores how sensitive investors remain to trade uncertainty and unexpected social media announcements.

In Canada, the TSX followed a similar ride – starting strong thanks to firm commodity prices (especially gold) and some spillover from the US AI rally, but losing steam later in the week. Canada’s merchandise trade deficit widened sharply in August to C$6.3 billion, the second largest on record, as exports fell about 3% and imports inched up nearly 1%. The data points to global headwinds and ongoing US tariffs weighing on Canadian exports, suggesting trade could remain a weak spot heading into fall.

Adding to the mix, Canada’s labour market surprised on the upside in September, with 60,000 mostly full-time jobs added and the unemployment rate holding steady at 7.1%. The strong report shows the job market remains resilient, though younger workers are still facing challenges. The surprising strength also dims the chances of a near-term BoC rate cut, as solid employment suggests the economy is holding up better than expected.

Finally, Statistics Canada warned it may have to delay its upcoming international trade report if the American government shutdown continues. Since roughly 70% of Canadian exports go to the US, missing American data would make it difficult to get a clear picture of how Canada’s trade story is really shaping up.

Investors started the week cautiously optimistic, keeping a close eye on the US economy and the kickoff of third-quarter earnings for clues about another potential Fed rate cut — but when trade tensions flared up, that optimism faded fast. In Canada, strong job gains were a bright spot, even as trade challenges lingered. With earnings season ramping up and uncertainty over the US outlook still hanging in the air, this market rollercoaster could keep rolling for a few more weeks. Still, with that sharp drop to end the week, some buying opportunities might just pop up next week. 😊

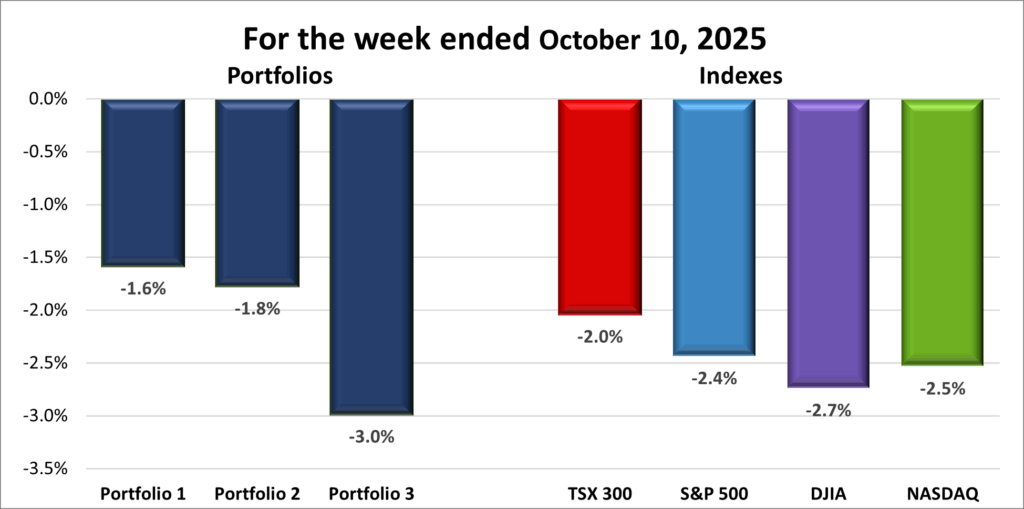

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week losing streak |

| Portfolio 2: | 1 – week losing streak |

| Portfolio 3: | 1 – week losing streak |

![]() As markets plunged late in the week, my three portfolios followed suit. Heading into Friday, Portfolios 1 and 3 were comfortably in the green, while Portfolio 2 was down just 0.5% — not bad considering the mixed performance across indexes. But when markets tanked on news that President Trump was threatening major new tariffs on China, the selloff pulled all three portfolios into the red. The decline was broad-based, with most holdings finishing the week lower.

As markets plunged late in the week, my three portfolios followed suit. Heading into Friday, Portfolios 1 and 3 were comfortably in the green, while Portfolio 2 was down just 0.5% — not bad considering the mixed performance across indexes. But when markets tanked on news that President Trump was threatening major new tariffs on China, the selloff pulled all three portfolios into the red. The decline was broad-based, with most holdings finishing the week lower.

Portfolio 1 held up the best, losing only 1.6% of its value. About a quarter of its holdings managed to post gains. There weren’t any standout winners, but there were a few sharp drops – Ferrari (NYSE: RACE) slid 20% after disappointing guidance pointed to slower growth ahead, while Magnite (NASD: MGNI) and Skyworks Solutions (NYSE: SWKS) dropped 13% and 10%, respectively. Before Friday’s selloff, though, Formula 1 Group (NASD: FWONK), Shopify (TSE: SHOP), and Cameco (TSE: CCO) all hit record highs, offering a nice reminder of the strength beneath the surface.

Portfolio 2 slipped 1.8%, enough to snap its nine week win streak. Only 18% of holdings posted weekly gains, but there were no major moves in either direction, which helped limit the damage. iA Financial (TSE: IAG) was a bright spot, touching a record high during the week.

Portfolio 3 had the roughest ride, plunging from up 1.4% on Thursday to a 3.0% loss by Friday’s close. Only 10% of its holdings ended the week higher, including Vertiv Holdings (NYSE: VRT), which reached another record high. Despite ending lower on the week, Shopify managed to set a record high before tailing off. Offsetting that strength were steep drops from Lithium Americas (TSE: LAC), down 19% after a strong two-week rally, and Magnite, which fell 13%.

As a result of the last-minute sell-off, there wasn’t a lot of good news, and the week ended on a shaky note. Sure, the markets threw a curveball at the end, but some of the holdings still managed to shine. Several hit record highs, showing pockets of strength and resilience. Volatility is just part of the ride, and weeks like this keep investing, uh, interesting. Yeah, that’s the word: interesting. 😊 Let’s see what surprises next week has in store – hopefully all three portfolios get back on the winning track! 😊

Companies on the Radar

No new companies came across my radar this past week, as I spent most of the time doing some housekeeping for Portfolio 3. I trimmed a long-term underperformer that hadn’t lived up to expectations, making room to focus on stronger prospects ahead, and increased my position in two exiting holdings. For now, the six companies below are still on my radar:

No new companies came across my radar this past week, as I spent most of the time doing some housekeeping for Portfolio 3. I trimmed a long-term underperformer that hadn’t lived up to expectations, making room to focus on stronger prospects ahead, and increased my position in two exiting holdings. For now, the six companies below are still on my radar:

- Mainstreet Equity Corp. (TSE: MEQ): a Calgary-based real estate company focused on mid-market apartment buildings – typically under 100 units – across Western Canada. It buys underperforming properties at below-market prices, renovates them, and increases rental income through improved operations. With strong demand for rental housing, a repeatable value-add strategy, and a solid balance sheet, Mainstreet offers a compelling mix of income and growth. Shares currently trade below net asset value, giving investors a margin of safety alongside steady cash flow and long-term upside.

- Napco Security Technologies, Inc. (NASD: NSSC): a small American owner/operator security firm that provides electronic locks, intrusion and fire alarms, access control systems, and video surveillance solutions for homes, businesses, and institutions. With a broad network of distributors and installers, growing recurring service revenue, and smart home integrations, the company has several avenues for growth. The company is riding the tailwind of an increasing demand for security products.

- XPEL, Inc. (NASD: XPEL): a growing American founder run company that produces high-quality protective films, coatings, and related products, primarily for cars but increasingly for architectural and other applications, such as paint protection film (PPF), window tint, and ceramic coatings. The company sells through multiple channels giving it both reach and control.

- Tornado Infrastructure Equipment Ltd. (TSEV: TGH): a small Canadian industrial company that designs, builds, and sells hydrovac trucks across North America, while also generating recurring revenue through rentals, parts, and maintenance – making it more than just a pure equipment play.

- Arista Networks (NYSE: ANET): an American company that designs and sells advanced networking hardware and software, with a focus on high-speed, low-latency switches for its key markets: data centres, AI, cloud computing, and financial trading. The company has been riding the AI tailwind with solid demand from its core markets, especially in AI and cloud data centres. It also has a hefty share buyback program and increasing investments from some of the top institutional investment companies.

- Corning Incorporated (NYSE: GLW): a large cap American company that is a leader in specialty glass, optical fiber, environmental technology, life sciences, and other specialty glasses. They have been the supplier of the glass used in Apple’s iPhones since 2007, and they are riding the tailwind of an AI-driven fiber optic boom.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated October 10, 2025.

Portfolio Updates

Portfolio 3

Brookfield Corporation (TSX: BN) and Brookfield Wealth Solutions (TSX: BNT) split on a 3-for-2 basis. While I will get one extra share of each company for every two I already hold, my ownership in both companies is still very, very, very small. 😊

Bought: Brookfield Corp. I picked up a few more shares of Brookfield, often called the Berkshire Hathaway (NYSE: BRK.B) of Canada, and for good reason. Like Warren Buffett’s empire, Brookfield is a collection of high-quality businesses spanning infrastructure, real estate, renewable power, and private equity. CEO Bruce Flatt, sometimes nicknamed “Canada’s Warren Buffett,” has built a reputation for disciplined, long-term investing and smart capital allocation.

Brookfield’s structure mirrors Berkshire’s, with the parent company holding large stakes in several strong, independently run subsidiaries including: Brookfield Renewables (TSE: BEP.UN), Brookfield Asset Management (TSE: BAM), Brookfield Infrastructure (TSE: BIP.UN), and Brookfield Wealth Solutions. By reinvesting steady cash flows and focusing on compounding value over time, Brookfield has grown into one of Canada’s most globally recognized companies – a go-to name for investors seeking exposure to real assets without having to pick individual winners.

Its diverse mix of businesses gives it resilience through market cycles, while a growing base of fee-related earnings provides reliable, recurring cash flow – something us long-term investors can really appreciate. With a strong management team, meaningful insider ownership, and ongoing share buybacks, Brookfield continues to earn my confidence in its ability to create lasting shareholder value.

The stock still trades around fair value, and following Warren Buffett’s timeless advice – “It’s better to buy a great company at a fair price than a fair company at a great price” – I decided to top up my position. Instead of trying to guess which Brookfield arm might outperform, I’d rather own the parent and get a piece of them all. 😊

Bought: Brookfield Wealth Solutions I added a few more shares of Brookfield Wealth Solutions, to get more direct exposure to the company which has quietly been building a strong presence in the insurance and annuity space. Its expanding pension risk transfer and annuity business provides steady, long-term cash flow, the kind of dependable income that helps smooth out portfolio volatility. With a growing global footprint, including its recent move into the United Kingdom market through the Just Group PLC (LSE: JUST) acquisition, BNT looks well-positioned for continued growth. Management has also shown discipline with its balance sheet and a clear commitment to shareholder returns through consistent distributions.

All in all, it felt like a good time to top up my position in this quietly powerful member of the Brookfield family. Together with my purchase of more Brookfield Corporation, discussed above, both moves felt like smart, steady additions – doubling down on a proven, globally diversified platform built for long-term compounding.

Sold: Adyen N.V. (OTCM: ADYEY) Adyen is a Dutch fintech company offering a global payments platform for online, mobile, and point-of-sale transactions. I invested in the company back in December 2020, and the share price is still well below my purchase price. Recently, the stock has struggled due to slowing sales growth – the company reported its slowest growth ever – rising competition in key markets, and regulatory challenges, including US tariffs. With these headwinds and no sign the share price will surpass my entry point any time soon, I decided it was a good time to exit my position and reallocate the capital to more promising opportunities.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!