Trade Tensions Flare, Again

Since President Trump returned to office in January, his administration has been trying to reshape global trade in America’s favour. One of his earliest targets was China, the world’s second largest economy, trailing only the US. Since both sides have recently began ratcheting up the trade tension again, with new tariffs, export controls, and tit-for-tat sanctions making headlines, I thought it would be a good time to review the situation and what it could mean for investors everywhere – including here in Canada.

Where we were: After a few months of cautious détente, the US–China relationship had felt like a pause rather than a solution – both sides had signalled they wanted to avoid open conflict, but big structural disputes over technology, supply chains and rare earths never went away.

Quick timeline (how we got here):

- Oct 9–12: China tightened rules on rare-earth exports and related technology – critical for chips, electric vehicles, and defense supply chains.

- Oct 10: The US threatened sweeping tariffs on Chinese goods, including an additional 100% tariff on top of existing tariffs, increasing market volatility.

- Oct 12–14: China defended its export curbs and introduced retaliatory measures; both sides implemented tit-for-tat port/ship fees and targeted sanctions, expanding the dispute beyond tariffs and technology into shipping and logistics.

Impact on the Canadian economy:

Canada is closely tied to both the US and global supply chains, so trade disruptions between the world’s two largest economies could quickly ripple north. If Chinese demand for US goods drops, US manufacturers may scale back production, reducing their need for Canadian raw materials and components. At the same time, if China retaliates against US exports, Canada may see temporary opportunities to fill gaps, but uncertainty around commodity prices and trade flows will rise. Energy, mining, manufacturing, and forestry could all feel the impact, and the Canadian dollar may weaken as investors seek safe-haven currencies like the US dollar.

What this means for investors:

The renewed tension increases market uncertainty, and, markets hate uncertainty. Volatility is likely, particularly in sectors tied to global supply chains: semiconductors, autos, industrials, and any business reliant on rare-earth materials. Higher shipping costs and restricted inputs can squeeze margins, slow earnings growth, and put pressure on stock prices. Conversely, safe-haven assets like gold and high-quality bonds often benefit during these types of shocks.

Implications for Canadian investors:

For Canadian investors, the effects will be uneven. Some exporters may benefit if they can fill gaps left by disrupted US-China trade, while companies closely tied to global supply chains or reliant on exports could face headwinds. Sectors like autos, industrials, and mining are likely to experience the biggest swings. For long-term investors, the key is to focus on high-quality companies with strong balance sheets and diversified markets, which are usually more resilient during geopolitical or trade-related uncertainty.

All of this shows why it pays to keep an eye on the bigger picture, especially if you own companies tied to global trade, technology, or commodities – which most of us do. Let’s now take a look at how these trade tensions, along with the start of third-quarter earnings season, shaped the markets and my portfolios this past week.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Canadian Market Volatility

Canada’s volatility gauge, the S&P/TSX 60 Volatility Index (VIXC), jumped to 20.18 at the start of the week as renewed China–US trade tensions rattled investors. It then eased into a calmer range between 16.4 and 17.75 for most of the week, but worries resurfaced late in the week after disappointing results from US regional banks pushed the index back above 18 on Thursday, before it closed at 18.81.

For anyone new to it, the VIXC is basically a barometer of investor nerves in Canada. When it’s in the single digits or low teens, markets are calm. Once it climbs into the high teens or beyond, it shows investors are getting uneasy and bracing for more swings ahead. With the index ending just above 18, it suggests that while there’s some tension in the air, Bay Street isn’t panicking – just staying alert.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

The shutdown, which began on October 1, has delayed several key government economic data releases. Among the data delayed is this week’s Consumer Price Index and Retail Trade reports. Updates will start again when the Federal government resumes operations.

American Market Volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” started the week at 19.45 and bounced between 18.50 and 22.50 as renewed trade tensions with China pushed it above 20. Strong earnings from major US banks helped calm nerves and hinted that the economy was still on solid footing. That relief didn’t last, though – weak results from regional banks reignited worries and sent the fear gauge surging past 25 on Thursday, then above 28 on Friday, its highest level since May, before settling at 20.78.

Think of the VIX as the market’s mood ring. With readings now hovering above 20, it shows that investors are getting uneasy and bracing for more volatility. While it’s not a sign of panic, it does suggest that caution and uncertainty are starting to creep back into the market.

Weekly Market and Portfolio Review

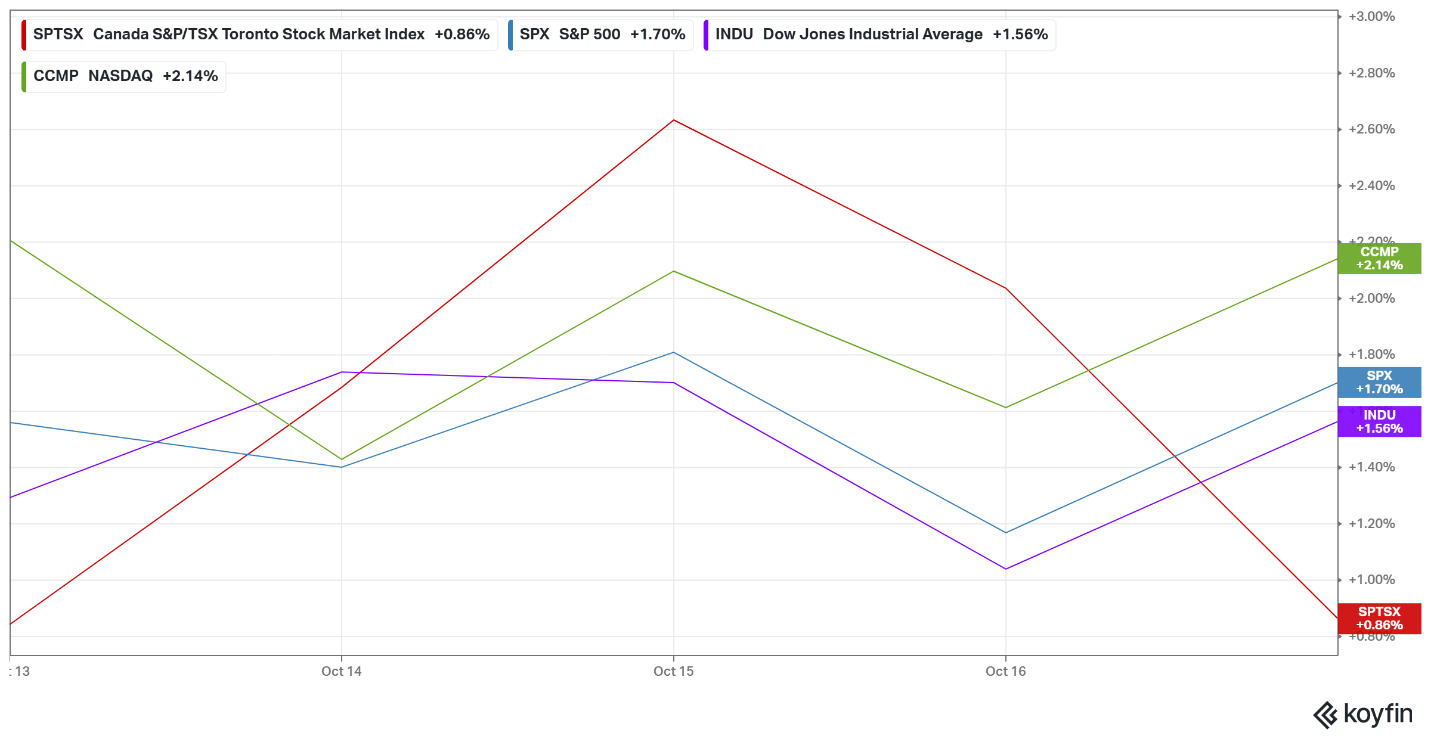

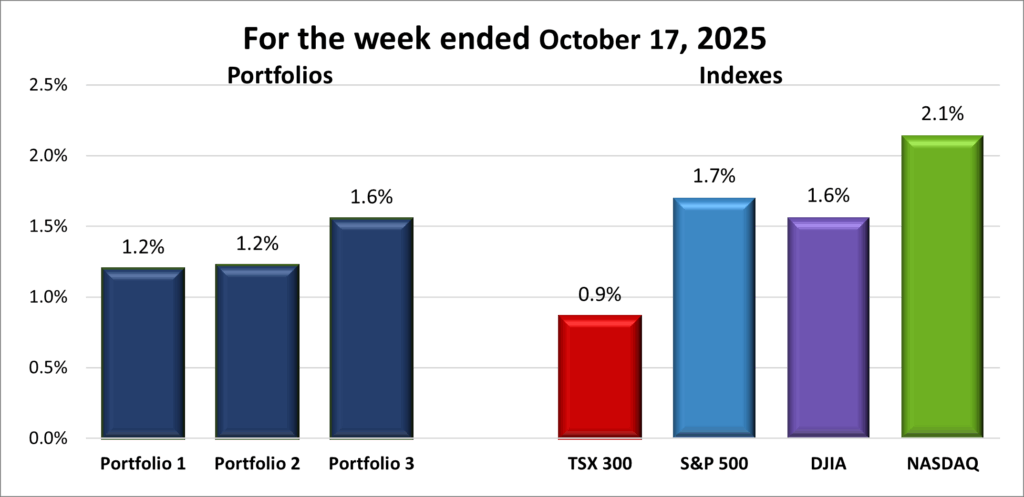

For the week, the TSX (SPTSX) rose 0.9%, the S&P 500 (SPX) climbed 1.7%, the DJIA (INDU) advanced 1.6% and the Nasdaq (CCMP) jumped 2.1%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() The rollercoaster continued for the major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – as they started strong, dipped midweek, and then clawed back gains to finish higher. The TSX posted the smallest weekly gain, but still managed to notch another record high before pulling back at the end of the week.

The rollercoaster continued for the major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – as they started strong, dipped midweek, and then clawed back gains to finish higher. The TSX posted the smallest weekly gain, but still managed to notch another record high before pulling back at the end of the week.

Markets spent the week reacting to a mix of trade headlines, artificial intelligence (AI) excitement, and early earnings reports. After last Friday’s selloff, US markets rebounded sharply on Monday when President Trump reassured investors with his “Don’t worry about China — it’ll all be fine!” comment. The optimism faded quickly, though, after the US announced plans to impose an additional 100% tariff on top of existing duties on Chinese imports starting November 1, while also tightening export controls on key software. China hit back with sanctions on US -linked firms, defended its rare-earth export curbs, and matched new American port fees on Chinese vessels with new port fees of their own on American vessels. The dispute has now spilled from technology and manufacturing into shipping and raw materials – a reminder that when the world’s two largest economies clash, no one wins in trade wars. Fortunately, tensions eased by week’s end after Trump said talks with China were progressing well and admitted that a 100% tariff on top of existing duties would be unsustainable for both sides.

The ongoing US government shutdown, now in its third week and the third longest in history, delayed the release of key economic reports, including the Consumer Price Index scheduled for this week. With limited fresh data, the Fed faces added uncertainty heading into its October 28–29 meeting, making earnings reports even more closely watched for clues on the economy. Strong results from major American banks early in the week lifted sentiment, suggesting resilience in consumer spending and business activity. But later in the week, weak results from two regional banks warning about higher loan losses reignited concerns over credit quality, dragging down the financial sector and broader markets. Rising loan losses often hint that borrowers are struggling to keep up with debt payments, which can point to tightening financial conditions or a slowing economy. Investors also worry that problems in smaller banks could spread to larger institutions, reducing credit availability and shaking confidence across the financial system. Fortunately, sentiment improved at week’s end after several other regional banks posted solid earnings, helping calm investor jitters and lift markets heading into the weekend.

AI optimism remained a steady tailwind for technology companies, helping lift the Nasdaq to its best day since late May after OpenAI, the developer of ChatGPT, announced a major new partnership with chipmaker Broadcom (NASD: AVGO). The deal includes plans to build custom AI chips and the massive data-centre systems that will power them. OpenAI will design the chips and system architecture, while Broadcom will handle manufacturing and networking – essentially building the infrastructure that ties it all together.

In Canada, the TSX had a strong week, climbing to a record high. Expectations of potential rate cuts, fueled by dovish US Fed commentary, lifted hopes that borrowing costs could ease sooner than expected. Rising metal and gold prices gave the index extra support, with resource-heavy sectors leading the way. Weaker oil, a softer loonie, and the renewed US–China trade tensions tempered some of those gains. Corporate earnings added another layer to the market’s mood – strong results from major banks initially lifted sentiment, while weaker reports from regional banks reminded investors that uncertainty is far from over.

Overall, the week showed how quickly market sentiment can shift with every trade headline and earnings surprise. Optimism around AI and strong bank results lifted stocks early on but worries about regional banks and US–China tensions kept investors cautious. By week’s end, easing trade tensions and reassuring results from regional banks helped steady nerves and sent investors into the weekend in a more upbeat mood. With earnings season picking up and key economic data still delayed, next week should bring more clues about where the economy and markets are headed.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 1 – week winning streak |

| Portfolio 3: | 1 – week winning streak |

![]() This week turned out to be a pleasant surprise after all three portfolios lost ground the previous week. Only Portfolio 2 had more than half its holdings finish higher, but all three managed to post gains.

This week turned out to be a pleasant surprise after all three portfolios lost ground the previous week. Only Portfolio 2 had more than half its holdings finish higher, but all three managed to post gains.

Portfolio 1 rose 1.2%, with 42% of holdings ending the week in the green. Celestica ((TSE: CLS) and Walmart (NYSE: WMT) both hit record highs, while Cameco (TSE: CCO) briefly reached a new peak before slipping to finish lower for the week. Navitas Semiconductor (NASD: NVTS) gave the portfolio a big lift, soaring 69% after launching a new chip designed to support Nvidia’s next-generation AI systems. Offsetting some of those gains was an 11% drop from Sea Limited (NYSE: SE).

Portfolio 2 got back in the win column with a 1.2% weekly gain. It was the only portfolio with a majority of holdings advancing, as 59% of its stocks moved higher. There were no standout winners or laggards – just broad-based participation that nudged the portfolio back into the weekly win column, making it ten weekly gains in the last eleven weeks.

Portfolio 3 was the biggest surprise. Only 30% of its holdings finished higher, yet it still managed a 1.6% gain. Even its two largest positions ended slightly lower. It’s baffling, but I’ll take it. 😊

Overall, the week turned out better than expected. It would’ve been nice to see broader participation, but any time portfolios post gains, especially after a down week, I’m more than happy to take the win. 😊

Companies on the Radar

No new companies popped up on my radar this past week, but I did remove one. While running my Quick Test on Tornado Infrastructure Equipment Ltd. (TSEV: TGH) – a small Canadian builder of hydrovac trucks – I found out it’s being bought by The Toro Company (NYSE: TTC) for C$1.92 per share, with the deal expected to close in early 2026. Since TGH is trading at C$1.89, there’s very little upside left before it’s absorbed by TTC. It would’ve been a dumb move to buy in now, but it’s a good reminder to always do your due diligence before investing your hard-earned money. 😊

No new companies popped up on my radar this past week, but I did remove one. While running my Quick Test on Tornado Infrastructure Equipment Ltd. (TSEV: TGH) – a small Canadian builder of hydrovac trucks – I found out it’s being bought by The Toro Company (NYSE: TTC) for C$1.92 per share, with the deal expected to close in early 2026. Since TGH is trading at C$1.89, there’s very little upside left before it’s absorbed by TTC. It would’ve been a dumb move to buy in now, but it’s a good reminder to always do your due diligence before investing your hard-earned money. 😊

Meanwhile, I’m still trimming long-time underperformers from my portfolios to build cash that I can put to work in stronger opportunities – possibly some of the five holdovers listed below.

- Mainstreet Equity Corp. (TSE: MEQ): a Calgary-based real estate company focused on mid-market apartment buildings – typically under 100 units – across Western Canada. It buys underperforming properties at below-market prices, renovates them, and increases rental income through improved operations. With strong demand for rental housing, a repeatable value-add strategy, and a solid balance sheet, Mainstreet offers a compelling mix of income and growth. Shares currently trade below net asset value, giving investors a margin of safety alongside steady cash flow and long-term upside.

- Napco Security Technologies, Inc. (NASD: NSSC): a small American owner/operator security firm that provides electronic locks, intrusion and fire alarms, access control systems, and video surveillance solutions for homes, businesses, and institutions. With a broad network of distributors and installers, growing recurring service revenue, and smart home integrations, the company has several avenues for growth. The company is riding the tailwind of an increasing demand for security products.

- Arista Networks (NYSE: ANET): an American company that designs and sells advanced networking hardware and software, with a focus on high-speed, low-latency switches for its key markets: data centres, AI, cloud computing, and financial trading. The company has been riding the AI tailwind with solid demand from its core markets, especially in AI and cloud data centres. It also has a hefty share buyback program and increasing investments from some of the top institutional investment companies.

- Corning Incorporated (NYSE: GLW): a large cap American company that is a leader in specialty glass, optical fiber, environmental technology, life sciences, and other specialty glasses. They have been the supplier of the glass used in Apple’s iPhones since 2007, and they are riding the tailwind of an AI-driven fiber optic boom.

- XPEL, Inc. (NASD: XPEL): a growing American founder run company that produces high-quality protective films, coatings, and related products, primarily for cars but increasingly for architectural and other applications, such as paint protection film (PPF), window tint, and ceramic coatings. The company sells through multiple channels giving it both reach and control.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated October 17, 2025.

Portfolio Update

Portfolio 1

Sold: Indie Semiconductor (NASD: INDI) After holding shares in the company for two years, I decided it was time to move on. When I first invested, I thought Indie Semiconductor had an exciting opportunity – supplying chips for cars and driver-assistance systems – but the results just haven’t lived up to expectations. Revenue has been growing, but the company is still unprofitable, and frequent share issuances have made it harder for investors to see meaningful progress in the stock price.

INDI has also struggled to build steady momentum in a competitive market where larger chipmakers hold a clear advantage. Rather than waiting years for a potential turnaround, I chose to sell my shares and put that money to work in more promising opportunities.

Portfolio 3

Sold: Real Matters (TSE: REAL) After five years, I lost patience with Real Matters, the mortgage appraisal and title services company. When I invested in the company in January 2020, the business looked like it was gaining real traction – and it did for a while. The stock surged to around $32 by August 2020, but the momentum didn’t last. Within a year, it had fallen below $15, and today it trades just above $7, about 20% below the price I paid. ☹

Real Matters’ performance is still closely tied to housing and refinancing volumes, and higher interest rates have weighed heavily on both. Growth and profitability have been inconsistent, and the company hasn’t shown the steady growth or competitive edge I was hoping for. At this point, I’ve decided to move on and redeploy that capital into companies with stronger momentum, and a better chance of immediate or near-term growth.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!