Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Fear gauges, Nvidia knocks it out of the park…

Canadian Economic news

Canada’s Retail Sales: What It Means for Interest Rates

Canada’s retail sales in June rose 0.1% from May, surpassing expectations of it remaining unchanged. While an increase in sales may sound like bad news for investors who are concerned about an interest rate hike, the increase was primarily driven by vehicle and vehicle parts sales. Excluding these sectors, core retail sales actually declined by 0.9% on a monthly basis.

On an annual basis, the picture is reversed, with total retail sales down 0.6% but core retail sales up 1.2%.

The Bank of Canada (BoC) will be closely monitoring retail sales in the coming months to assess the health of the economy and make decisions about interest rates. The June retail sales data is mixed, with total sales up, yet core sales down. This could be a sign that the economy is slowing down, which could lead the BoC to hold off on raising interest rates.

The combination of inflation unexpectedly higher in July, up 3.3%, lower employment numbers and this mixed retail sales report could be enough to tilt the odds towards the BoC maintaining the benchmark interest rate at 5.0%.

Canadian budget update

The Canadian finance ministry reported a budget surplus of C$ 3.62 billion for the first quarter (April through June) of the 2023-2024 fiscal year. That was well below the C$ 10.2 billion surplus posted in the same period last year. For the month of June, Canada had a surplus of C$ 2.11 billion, compared to a C$ 4.88 billion surplus a year ago.

Revenues were up thanks to money collected from income tax, higher interest rates, and higher Employment Insurance premium revenues. However, the increase in revenues was not enough to offset the rise in expenses which were higher due to increases in government program expenses, such as healthcare and social assistance. Higher interest rates also meant higher interest payments on government debt.

The budget surplus is the difference between government revenues (your tax dollars) and expenses (your tax dollars at work). A budget surplus means that the government is taking in more money than it is spending. A budget deficit means that the government is spending more money than it is taking in.

US Economic news

Consumer sentiment

The University of Michigan’s final consumer sentiment (CSI) results for August dropped slightly to 69.5 from 71.6 in July but above 58.2 recorded in the prior year. Analysts had been expecting 71.2.

This was the second highest reading in twenty-one months. The current reading is 39% above the all-time low set in June 2022 and the second highest since December 2021. The historic average is 86. Concerns about higher interest rates for longer and a slowdown in the drop of inflation slightly cooled consumer sentiment.

Fear gauges

Both the Canadian and American volatility indexes (VIX) are currently showing relatively stable levels, reflecting the market sentiment in each country. The Canadian VIX (VIXC) stands at 11.32, while the American VIX registers at 15.7. Both are on a scale of 0 to 100. VIX readings in the mid teens typically indicate a moderate level of investor confidence and a relatively stable market environment. When the VIX is in this range, it suggests that investors are not perceiving significant levels of near-term volatility or uncertainty in the market.

These indices are tools that can be used by investors to gain insights into market expectations over the next 30 days. The American VIX, often referred to as the ‘fear gauge’, gauges the expected volatility, rather than actual volatility, within the S&P 500 stock market index over the upcoming 30 days. While the Canadian VIX may not be as widely recognized as its American counterpart, it serves the same purpose in assessing the anticipated volatility in the S&P/TSX 60 stock market index. Both typically hover around 20. Below 20 indicates investor confidence in the market’s future performance. Conversely, readings above 20 signal heightened investor apprehension. Both the Canadian VIXC and the American VIX, fluctuate in real time, capturing market volatility as it evolves throughout the day.

Nvidia knocks it out of the park

Nvidia’s (NASD: NVDA) stock price has surged this year thanks to strong demand for its semiconductors, especially in the rapidly expanding artificial intelligence (AI) market where Nvidia is the dominant player. The company’s sales have been growing at an unprecedented rate. After their first quarter earnings report in May, Nvidia increased its sales forecast for the second quarter from US$ 7.2 billion to US$ 11 billion (an impressive 53% increase), which triggered an AI-focused rally throughout June and July.

Their second quarter earnings report was highly anticipated and influenced the markets even before Nvidia released its report. Leading up to the announcement, all four major North American indexes rallied, propelled by the expectations of Nvidia’s earnings. The surge in Nvidia’s performance also boosted other AI-oriented companies, sparking a rally in the stock market (although it turned out to be short lived).

In this latest report, Nvidia not only delivered on their May forecast, but they blew past the analysts’ estimate of US$ 11 billion in revenues, coming in at US$ 13.5 billon. This earnings report suggests that the growth caused by AI in the first quarter was not a momentary spike, but rather the start of a sustained period of growth for Nvidia’s AI offerings.

Following the announcement, Nvidia’s shares experienced a surge of over 9% in after-hours trading, reaching an all-time high of US$ 512 per share before retreating slightly. Much of Nvidia’s performance has been driven by the rapidly growing demand for its highly advanced processors required to train the latest artificial intelligence models such as OpenAI’s ChatGPT and Google’s (NASD: GOOGL) Bard.

This increase in share price propelled Nvidia’s market capitalization to an impressive US$ 1.27 trillion, solidifying its position as the leading semiconductor manufacturer in the world. With this latest earnings report and Nvidia’s third quarter forecast of US$ 16 billion in revenues, any lingering doubts about Nvidia’s supremacy in the emerging AI sector should be dispelled.

Finally, the company unveiled a US$ 25 billion stock buyback plan, adding to the share price’s upward momentum. Given the tremendous growth of the share price in 2023 already, it would be great if the shares are underpriced. 😊

Quite the earnings report, indeed! The AI market is still in its early stages, and Nvidia is the leading player in this growing market. I am very excited to be an owner of a fine company that is in the right industry and the right time. 😊

Finally! For the first time this month an overall positive week in the markets. Let’s see how that happened ….

Weekly Market Review

Monday: A rally in technology companies, outweighing concerns of higher interest rates, spurred a rebound in the Nasdaq Composite Index (Nasdaq) and the S&P 500 Index (S&P). On the losing side, lower oil prices dragged the Toronto Stock Exchange Composite Index (TSX) and the Dow Jones Industrial Average (DJIA) lower. China maintained it benchmark interest rate, passing on an opportunity to further stimulate their economy through lower interest rates. This caused analysts to lower expectations for growth in the world’s second largest economy. Lower growth would lead to lower demand for oil, causing oil prices to fall.

In Canada, in trading on the TSX, Technology and Basic Materials (miners and fertilizer manufacturers) were the only Canadian sectors to post gains, while Utilities and Financials had the steepest declines.

In the US, with today’s advance, the Nasdaq broke a four-day losing streak. Investors are also looking forward to Friday’s speech by Federal Reserve Chair Jerome Powell at an annual global gathering of central bankers. They are hoping for clues on the Fed’s path for interest rates for the rest of the year. Investors are also keenly awaiting Nvidia’s (NASD: NVDA) earnings report on Wednesday to see if the Nvidia led AI bull run still has legs. In trading, Technology and Consumer Cyclicals lead all gainers, while Utilities and Consumer Staples fell the furthest.

Tuesday: The Nasdaq was the only one of the four major North American indexes to end in the green, but just barely. The Nasdaq was pushed higher in anticipation of a strong earnings report from Nvidia tomorrow. The other three were weighed down by rising bond yields that are caused by the higher interest rates and expectations they will remain high for longer. With decent bond yields (4% and higher), investors are moving their money to less risky bonds.

In Canada, the TSX was weighed down by the financial sector where financial institutions are having to raise their bond rates to compete with safer government bonds. In the Canadian sectors, Basic Materials, Utilities, and Technology were the only sectors to advance, while Financials and Energy suffered the biggest losses.

In the US, credit ratings agency S&P Global joined fellow global credit agencies by lowering the credit rating of several US regional banks. The agency said funding risks and lower profits could push the limits of the financial sector’s strength. The lower credit rating will make it more costly for those banks to borrow money. In trading, Consumer Cyclicals, Utilities and Basic Materials were the only sector to end in the green. Among the sectors that declined, Financials and Energy dropped the most.

Wednesday: Finally, a day where all four indexes finished sharply higher. The Nasdaq and S&P were driven higher by a rally in Nvidia shares when the company easily beat analysts’ projections. Otherwise, investors are waiting to hear from Fed Chair Jerome Powell on Friday when he gives the keynote speech at a gathering of global bankers. Investors hope he will provide insight into when and how the Fed plans to end their battle with inflation.

In Canada, the TSX was led higher by a surge in the Canadian Technology sector, and solid gains in the Basic Materials sector. The Canadian Energy sector was the only sector to end in the red.

In the US, investors were betting a strong earnings report from Nvidia would prolong the AI inspired technology rally that has lifted the markets through most of 2023. In trading, the Technology and Financials sectors posted the largest gains, while the US Energy sector was the only sector to end lower.

Thursday: After a brief morning rally spurred by Nvidia’s blowout earnings report on Wednesday, all four indexes reversed course to end sharply lower. The markets’ decline began when a Fed official said it was “extremely likely” interest rates will need to remain high “for a substantial amount of time” to bring inflation down to their 2% target. Investors now await to see if Fed Chair Jerome Powell echoes those sentiments in his speech tomorrow.

In Canada, mixed results for two of Canada’s big six banks weighed on the TSX. In trading, the Telecommunications Services and Consumer Staples sectors were the only two sectors to advance, while Technology and Healthcare had the biggest drops.

In the US, the DJIA had its worst day since March despite the upward momentum from yesterday. In trading, all sectors ended lower today. Financials and Telecommunications Services fell the least while the interest sensitive sectors Technology and Consumer Staples suffered the largest declines.

Friday: All four indexes ended the day in the green, ending the week on a positive note. In today’s keynote speech, Fed Chair Powell delivered a balanced message, acknowledging inflation had come down but the Fed was still “prepared to raise rates further” to get it down to their 2% target. He said the Fed remains data driven but will proceed with caution. Investors took a glass half full approach to the news and pushed the markets higher. Oil prices rose, driven largely by a sharp increase in the price of diesel fuel caused concerns of a diesel shortage as refineries go into maintenance mode and the outbreak of a fire at a refinery.

In Canada, the TSX climbed on the higher oil prices, causing the Energy sector to be the best performer in the Canadian sectors, followed by the Technology sector. At the other end of the spectrum, Financials and Basic Materials were the only sectors to lose ground.

In the US, despite the possibility of another interest rate hike, the three American indexes all advanced. In trading, Consumer Cyclicals and Energy were the biggest gainers while Telecommunications Services was the only American sector to end lower.

Weekly Market and Portfolio Review

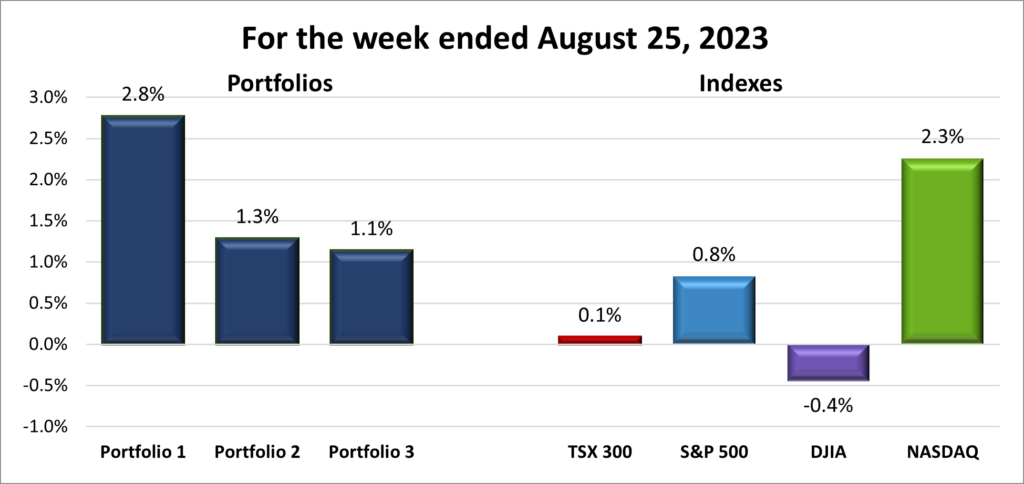

For the week, the TSX (SPTSX) inched up 0.1%, the S&P 500 (SPX) rose 0.8%, the DJIA (INDU) slipped 0.4% and the Nasdaq (CCMP) jumped 2.8%.

![]() Looking at the chart above, it was not until Friday that it became clear three of the four major North American indexes would post a weekly gain. While the TSX’s increase was modest, a gain is always a positive sign. 😊 The week’s market movements were primarily driven by two key factors: Nvidia’s earnings report and statements from Fed.

Looking at the chart above, it was not until Friday that it became clear three of the four major North American indexes would post a weekly gain. While the TSX’s increase was modest, a gain is always a positive sign. 😊 The week’s market movements were primarily driven by two key factors: Nvidia’s earnings report and statements from Fed.

You can see the midweek bump the Nvidia report provided all of the indexes. As the week progressed, investors’ focus shifted to Fed Chair Powell’s speech on Friday. Initially, there was a negative reaction when he suggested the possibility of higher interest rates. However, a closer examination of his speech revealed a reassuring aspect: the Fed’s commitment to a cautious approach. Powell stated that the Fed would “proceed carefully as we decide whether to tighten further or, instead, to hold the policy rate constant and await further data.” Essentially, this implies that if data continues to indicate declining inflation, they will stay the course.

This aspect of his speech caught the attention of investors, boosting the rate-sensitive Nasdaq and S&P indexes, and it also contributed to limiting the weekly losses in the DJIA. As for the TSX, higher oil prices and the potential that the Fed may not need to raise interest rates provided a boost to Canada’s main index, helping it over the line into positive territory.

![]() Finally all three Portfolios were able to post a weekly gain in August, thanks to a strong week from American technology companies. As you can see in the chart below, Portfolio 1 had the biggest gains of all the portfolios and indexes, thanks to a 6.3% gain from Nvidia. Portfolio 2 rose on the strength of a good week from Microsoft (NASD: MSFT) and a few other companies. Aside from Disney (NYSE: DIS) which continues to struggle, no company in the portfolio experienced a sizable drop this past week. Portfolio 3 was lifted by Microsoft and Shopify (TSX: SHOP) but gains were limited by drops in its two Canadian bank stocks. Despite a strong week from the technology sector, Adyen (OTCM: ADYEY), the payment processor, continued last weeks slide.

Finally all three Portfolios were able to post a weekly gain in August, thanks to a strong week from American technology companies. As you can see in the chart below, Portfolio 1 had the biggest gains of all the portfolios and indexes, thanks to a 6.3% gain from Nvidia. Portfolio 2 rose on the strength of a good week from Microsoft (NASD: MSFT) and a few other companies. Aside from Disney (NYSE: DIS) which continues to struggle, no company in the portfolio experienced a sizable drop this past week. Portfolio 3 was lifted by Microsoft and Shopify (TSX: SHOP) but gains were limited by drops in its two Canadian bank stocks. Despite a strong week from the technology sector, Adyen (OTCM: ADYEY), the payment processor, continued last weeks slide.

Overall, a good week for the markets and the indexes. After a rough start to August its good to see all three portfolios post weekly gains.

Companies on the Radar

Medpace Holdings, Inc. (NASD: MEDP) and Snowflake, Inc. (NYSE: SNOW) have been dropped from the Radar List, but not forgotten. 😊

Medpace Holdings, Inc. (NASD: MEDP) and Snowflake, Inc. (NYSE: SNOW) have been dropped from the Radar List, but not forgotten. 😊

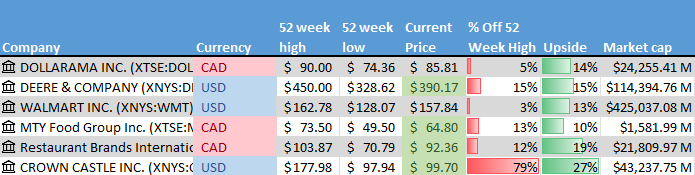

New to the list are Dollarama (TSX: DOL), a large Canadian company that operates dollar stores across Canada; Deere & Company (NYSE: DE), a large American company that manufactures and sell agricultural equipment worldwide; and Walmart (NYSE: WMT), a big American retail and wholesale company that operates globally. All are well-known companies, pay less than a 1.5% dividend and score well on the Radar Test, as seen in the tables below.

These companies will join the holdovers from last week:

- MTY Food Group Inc. (TSE: MTY): A small cap Canadian consumer cyclical company that operates and franchises quick service and casual dining restaurants throughout North America and internationally.

- Restaurant Brands International Inc. (TSE: QSR): A large cap Canadian consumer cyclical company that operates in the North American quick serve restaurant industry. The company owns Tim Horton’s, Burger King, and Popeye’s Louisiana Kitchen among others.

- Crown Castle Inc. (NYSE: CCI), a large cap American company that owns and operates cell towers throughout America

The Radar Check was last updated August 25, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended August 25, 2023: UP ![]()

- Tesla (NASD: TSLA) has lowered their output of electric vehicles (EV) at their German production facility to 4,350 vehicles. The company had hit a high of 5,000 EVs per week in March but has since slowed down and plans to slow production further.

- Cloudflare (NASD: NET) partnered with SpaceX to improve the performance of SpaceX’s Starlink satellite internet service. The two companies are working together to increase the number of mini data centres around the world and to improve network speeds to end users.

- Progeny (NASD: PGNY) announced that through their partnership with Amazon (NASD: AMZN), they have helped over 30,000 Amazon employees with their “family building journeys.” In 2019, Progeny partnered with Amazon to help Amazon employees with fertility benefits and family building.

Activity

Received interest on TD 1-year cashable GIC.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Pulse Seismic Inc (TSX: PSD) Consisting of a regular quarterly dividend of $0.01375 per share and a special dividend of $0.15 per share.

TMX Group Ltd (TSX: X)

US $

No US$ dividends this past week.

Quarterly Reports

Nvidia Corporation

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their second quarter 2024 financial results on August 23, 2023

- Revenue of $13,507 for the three months ended July 31, compared to $6,704 for the same period in 2022. An increase of over 101%.

- Net income of $6,188 for the three months ended July 31, compared to net income of $656 in the same period in 2022.

- Diluted earnings per ordinary share of $2.48 for the three months ended July 31, compared to earnings of $0.26 per share for the same period in 2022.

- Revenue of $20,699 for the six months ended July 31, compared to $14,992 for the same period in 2022. An increase of over 38%.

- Net earnings of $8,232 for the six months ended July 31, compared to net earnings of $2,274 in the same period in 2022.

- Diluted earnings per ordinary share of $3.30 for the six months ended July 31, compared to earnings of $0.90 per share for the same period in 2022.

TD Bank Group

All currency listed in millions of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2024 financial results on August 24, 2023

- Revenue of $20,935 for the three months ended June 30, compared to $10,782 for the same period in 2022. An increase of over 94%.

- Net income of $2,889 for the three months ended June 30, compared to net income of $3,171 in the same period in 2022.

- Diluted earnings per ordinary share of $1.57 for the three months ended June 30, compared to earnings of $1.75 per share for the same period in 2022.

- Revenue of $58,298 for the nine months ended June 30, compared to $26,333 for the same period in 2021. An increase of over 121%.

- Net earnings of $7,896 for the nine months ended June 30, compared to net earnings of $10,758 in the same period in 2021.

- Diluted earnings per ordinary share of $4.11 for the nine months ended June 30, compared to earnings of $5.85 per share for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended August 25, 2023: UP ![]()

- Microsoft announced that in order to get the approval of the British anti trust regulator for their acquisition of Activision Blizzard (NASD: ATVI), it would sell the non-European streaming rights of Activision games to French rival Ubisoft Entertainment.

- Telus (TSX: T) announced they were making an initial donation of C$ 5 million, made up of cash donations and in-kind contributions. The money will go to local charities and organizations supporting relief efforts and first responders battling the wildfires in BC.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX: DIR.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended August 25, 2023: UP ![]()

- Canada’s largest bank, the Royal Bank (TSX: RY) beat analysts’ earnings per share (EPS) estimates for the third quarter, however, the bank plans to reduce costs by up to 2% as it prepares for a slowing Canadian economy.

- The news wasn’t so good for Canada’s second largest bank, the Toronto – Dominion Bank (TSX: TD) missed analysts’ EPS estimates due to higher expenses, a slowdown in the US side of its operations and the need to set aside more cash for unpaid loans.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Royal Bank of Canada

All currency listed in millions of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2024 financial results on August 24, 2023

- Revenue of $22,834 for the three months ended June 30, compared to $10,737 for the same period in 2022. An increase of almost 113%.

- Net income of $3,872 for the three months ended June 30, compared to net income of $3,577 in the same period in 2022.

- Diluted earnings per ordinary share of $2.73 for the three months ended June 30, compared to earnings of $2.51 per share for the same period in 2022.

- Revenue of $62,489 for the nine months ended June 30, compared to $25,873 for the same period in 2021. An increase of over 141%.

- Net earnings of $10,735 for the nine months ended June 30, compared to net earnings of $11,925 in the same period in 2021.

- Diluted earnings per ordinary share of $7.60 for the nine months ended June 30, compared to earnings of $8.31 per share for the same period in 2021.

TD Bank Group

See report under Portfolio 1.