AI Disrupters

For the past few years, anything connected to artificial intelligence (AI) felt unstoppable. Investors poured money into AI-related companies, pushing valuations higher as excitement around the technology grew. There were concerns about the massive capital expenditures required to build AI infrastructure, but the dominant narrative was simple: invest now, dominate later.

This year, that tailwind has started to feel more like a headwind. Investors shifted from asking, “Who benefits from AI?” to “When will companies start seeing a return on all that investment?” – and now, “Who gets disrupted by it?” That change in mindset helped trigger the recent meltdowns.

Once the focus turned to disruption, the ripple effects spread quickly. AI is no longer just a technology story – it’s an economy-wide force reshaping cost structures, pricing power, and competitive advantages across multiple industries.

The initial selling hit software companies, where investors worried that AI could reduce demand for traditional coding tools and enterprise software. But it didn’t stop there. The fear quickly spread to industries vulnerable to automation, cost compression, or outright business model disruption.

Wealth management firms faced concerns that AI-driven portfolio tools and robo-advisors could lower fees and reduce the need for human advisors, squeezing margins for firms slow to adapt. Transportation and logistics stocks slid as investors focused on autonomous trucks and AI-optimized routing systems that could make labour-heavy models uncompetitive.

Legal services also came under pressure. AI can now handle routine research and contract review in minutes — work once billed by the hour. If clients resist paying traditional rates for machine-assisted work, the billing model itself comes under strain. Customer support providers face similar risks as AI systems reduce the need for large front-line teams.

Even insurers, private credit firms, real estate brokers, and data analytics companies felt the pressure as AI improves risk modelling, automates transactions, and enables firms to bring capabilities in-house.

The concern isn’t that these industries disappear overnight. It’s that AI gradually compresses margins, erodes pricing power, and separates leaders from laggards.

Markets react quickly to that possibility. Stocks don’t move on today’s earnings alone – they move on expectations of what profits might look like years from now. When investors believe AI could permanently reshape revenue or costs, stock prices move fast.

The sector meltdowns over the past few weeks are a reminder: disruption doesn’t show up all at once in financial statements. It first shows up in expectations.

AI isn’t just creating new winners – it’s reshaping the competitive landscape. It’s no longer only about opportunity; it’s about disruption. As investors try to sort out who benefits and who gets left behind, that uncertainty has fueled the recent market meltdowns. Markets can handle change. What they struggle with is uncertainty about how it unfolds.

Now that we’ve discussed one of the biggest drivers of recent market moves, let’s look at what else shaped the week – and how it impacted my three portfolios. It was a busy stretch, with no shortage of headlines. As Daenerys Targaryen said at the start of her quest for the throne, “Let’s begin.” 😊

Items that may only interest or educate me ….

Supreme Court Limits Presidential Tariff Powers, Canadian Economic news, US Economic news, …

Supreme Court Limits Presidential Tariff Powers

In a major ruling, the US Supreme Court struck down former President Donald Trump’s sweeping global tariffs, finding he exceeded his legal authority by imposing them under an emergency-powers law that does not explicitly grant tariff powers. In a 6–3 decision, the Court ruled that only Congress has the constitutional authority to levy broad tariffs and that the 1977 International Emergency Economic Powers Act (IEEPA) did not provide sufficient legal basis for the measures.

The decision invalidates most of the so-called “reciprocal” tariffs imposed on trading partners including Canada. While the ruling does not automatically trigger refunds for tariffs already collected, it may open the door to legal challenges and repayment claims from affected businesses.

President Trump called the decision “deeply disappointing” and indicated he may pursue alternative trade statutes to implement targeted duties, including a proposed temporary 10% global tariff. The ruling is significant because it places limits on unilateral executive authority over trade policy and reinforces Congress’s role in major tariff decisions.

For Canada, the direct economic impact is expected to be modest. Most Canadian exports were already exempt under CUSMA (Canada-US-Mexico Agreement) rules of origin, and the ruling does not affect existing sector-specific tariffs on metals, lumber, or automobiles. It also does little to eliminate broader trade-policy uncertainty.

For investors, the ruling helped calm fears that trade tensions could escalate further, at least for now. That provided some short-term support to stocks. However, the situation isn’t fully resolved. Because the decision doesn’t block future tariffs under different laws, trade policy uncertainty could remain a source of market volatility in the months ahead.

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index (CPI)

Inflation cooled slightly in January. According to Statistics Canada, the annual CPI came in at 2.3%, down from 2.4% in December and just below expectations. Lower gasoline prices were once again the main reason for the softer reading. On a monthly basis, overall CPI was unchanged from December.

Looking closer, the picture was mixed. Food prices, especially restaurant meals, rose 7.3% year-over-year, while gasoline prices plunged 16.7%. From December to January, prices for alcohol, tobacco, and recreational cannabis increased 0.6%, while transportation costs fell 1.4%. Shelter costs, which include rent and mortgage interest, were up 1.7% from a year ago but slipped 0.1% in January. That’s the lowest annual shelter inflation in nearly five years, a sign that rent pressures are finally easing.

The BoC’s preferred inflation measure, Core CPI – which strips out food and energy to better capture underlying trends – fell for a fourth straight month. Core CPI edged down to 2.4% year-over-year from 2.5% in December and declined 0.2% on the month.

Inflation remains within the BoC’s 1%–3% target range, but the steady cooling – especially in core measures – adds to expectations that the Bank could shift its focus toward supporting economic growth. In practical terms, the Bank is now more likely to hold rates steady or eventually lower them, rather than raise them to fight inflation.

Retail Sales

Canada’s consumer spending cooled at the very end of 2025. According to Statistics Canada, retail sales fell 0.4% in December, slightly better than the expected 0.5% decline and a clear slowdown from November’s solid 1.3% gain. On a year-over-year basis, sales were flat, a sharp deceleration from the 3.1% growth recorded the month before.

The weakness wasn’t widespread, but it was noticeable. Three of the nine retail subsectors declined. Gasoline stations posted the strongest monthly increase, up 2.8%, while building material and garden equipment stores fell 4.0%. Compared with a year ago, sporting goods, hobby, musical instrument, book, and miscellaneous retailers rose 6.6%, while motor vehicle and parts dealers saw sales drop 5.2%.

Core retail sales, which exclude gasoline and auto dealers to provide a clearer view of underlying spending trends, slipped 0.3% in December after rising a revised lower 1.2% in November. On an annual basis, core sales growth slowed to 2.7% from 6.3% the previous month. That cooling suggests consumers may be becoming more cautious after a relatively resilient year.

One softer month doesn’t rewrite the story. Retail sales still rose roughly 4% for all of 2025, showing Canadian consumers remained resilient even with borrowing costs higher than many had grown used to. There’s also an early estimate suggesting sales could rebound by about 1.5% in January. If that holds, December may turn out to be more of a breather than the start of a sustained slowdown.

For the BoC, a single report like this won’t trigger immediate action. But it does add to the growing evidence that economic momentum may be cooling. If consumer spending continues to soften in the months ahead, it would strengthen the case for further rate cuts. For now, though, this looks more like a gradual easing in activity rather than a sharp downturn, which likely means BoC official will stay patient and wait for clearer signals before making their next move.

Canadian Market Volatility

Canada’s “fear gauge,” the VIXC (tracked by the VIXI), opened Monday at 16.94 before spiking toward 19 as lingering AI concerns and stronger-than-expected inflation dashed hopes of another rate cut. The gauge then eased back to the 16 level, only to climb above 17.5 amid renewed worries over US–Iran tensions. After the US Supreme Court struck down President Trump’s tariff policies, the fear gauge settled back to 16.35 by week’s end.

Readings in the mid- to high teens indicate caution rather than panic. The midweek jump reflected investors turning defensive as AI-related risks flared, while the pullback by Friday suggested those fears had eased.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open Market Committee (FOMC) Minutes

This week the Fed released the minutes from its January 27–28 meeting, where FOMC members held interest rates steady in the 3.50%–3.75% range. The decision was not unanimous and marked a pause after three rate cuts in 2025.

Inflation has been cooling, but officials made it clear they’re not convinced it’s fully under control yet. Their target for inflation is 2%, and while it is now just under 3%, that final stretch back to target is proving stubborn. At the same time, most members agreed the job market appears to have stabilized after unemployment ticked up late last year. AI was briefly discussed and was viewed as a potential source of economic uncertainty, because its long-term impact on productivity, inflation, and the labour market is still unclear.

For now, the Fed is pressing pause and adopting a wait-and-see approach. Rather than rushing into another rate cut, Fed officials want more evidence that inflation is steadily moving toward 2% before acting again. The minutes also included something we haven’t heard in a while: if inflation were to remain sticky, a rate hike could be back on the table. That’s not the base case – but it was enough to remind markets that the Fed isn’t declaring victory over inflation just yet.

In short, the Fed remains cautious. Inflation is improving, but not convincingly enough. The labour market is steady, but not weak enough to force cuts. Officials are watching the data closely and keeping their options open.

For consumers, this suggests interest rate relief may not be coming as quickly as hoped. For investors, it means markets will likely remain sensitive to upcoming inflation and jobs reports, as each new data point could shift expectations around the Fed’s next move.

Personal Consumption Expenditures (PCE)

The Bureau of Economic Analysis (BEA) reported that inflation picked up at the end of 2025. The PCE price index – the Fed’s preferred inflation gauge – rose 0.4% in December, above the expected 0.3% and up from 0.2% in November. On a year-over-year basis, headline inflation climbed to 2.9%, slightly higher than November’s 2.8% and above analysts’ expectations.

Core PCE, which strips out the more volatile food and energy categories, also gained 0.4% in December after a 0.2% rise in November. On an annual basis, the core index jumped to 3.0%, the highest rate in nearly a year and above the expected 2.9%.

The December report which was delayed due to the October–November 2025 government shutdown, shows that inflation is still above the Fed’s 2% target, particularly on the core measure the Fed watches more closely. The stronger-than-expected readings suggest price pressures are sticking around, which could keep officials cautious about cutting interest rates anytime soon.

Gross Domestic Product (GDP)

The latest GDP data from the BEA showed the US economy grew much more slowly than expected in the fourth quarter of 2025. GDP rose just 1.4%, roughly half of the 3.0% analysts had forecast and well down from 4.4% in the third quarter, marking a notable slowdown. This report was originally scheduled for January 29, 2026, but was delayed due to the October–November 2025 government shutdown.

Consumer spending and business investment still contributed positively, but big drops in government spending – partly due to the late-year government shutdown – and weaker exports weighed heavily. Many analysts point out that a lot of this slowdown comes from temporary, technical factors rather than a collapse in demand, and early estimates suggest growth could rebound in the first quarter of 2026.

In short, the economy is slowing, not contracting. Slower growth eases some inflation pressures because businesses have less pricing power and consumers may pull back slightly. That leans dovish for the Fed, reducing the case for rate hikes and keeping the door open for potential cuts later in the year. For now, though, the Fed is likely to stick with a “wait and see” approach, watching for clearer signs before making any moves.

Consumer Sentiment Index (CSI)

The latest reading from the University of Michigan’s CSI report shows Americans are feeling only slightly better about the economy. The index inched up to 56.6 in February from 56.4 in January, falling short of expectations for 57.3. Compared with a year ago, sentiment is still down 12.5%, which suggests confidence remains fairly fragile.

To put that number in perspective, readings in the 50s are historically associated with low confidence, well below pre-inflation surge levels. So while February brought a small improvement, it wasn’t enough to change the broader mood.

Looking at the present and future expectations, the details were mixed. The Current Economic Conditions Index, which reflects how people feel about their finances and job security today, rose 2.2% month over month to 56.6, though it is still nearly 14% lower than a year ago. Meanwhile, the Expectations Index, which looks ahead six months, slipped to 56.6 from 57.0 and is down 11.6% year over year. In other words, consumers feel slightly steadier about the present, but not necessarily more optimistic about what’s coming next.

Confidence also continues to split along income lines. Higher-income households and stockholders reported a somewhat brighter outlook, likely helped by stronger income growth and portfolio gains. Lower-income households were more cautious, with many respondents still pointing to high prices as a key strain on their finances.

Overall, this report fits the broader economic theme we’ve been seeing. The consumer isn’t collapsing, but enthusiasm is clearly muted. For markets, that kind of cautious tone can help keep inflation pressures contained and supports the idea that the Fed will stay patient. Still, optimism hasn’t returned in any meaningful way, which keeps the outlook balanced rather than bullish.

American Market Volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” opened the week at 21.70 before dipping as low as 18.50 midweek as AI concerns eased. Rising tensions between Iran and the US, along with the latest economic data, pushed the VIX back above 21. Following the US Supreme Court ruling on President Trump’s tariffs, investor anxiety eased and the index closed the week at 19.09.

Think of the VIX as the market’s pulse – readings above 20 usually signal heightened caution. This week showed how quickly sentiment can swing: AI disruption and interest rate worries pushed volatility higher, but the Supreme Court decision helped calm nerves. Investors aren’t panicking, but they’re clearly keeping a closer eye on risk.

Weekly Market and Portfolio Review

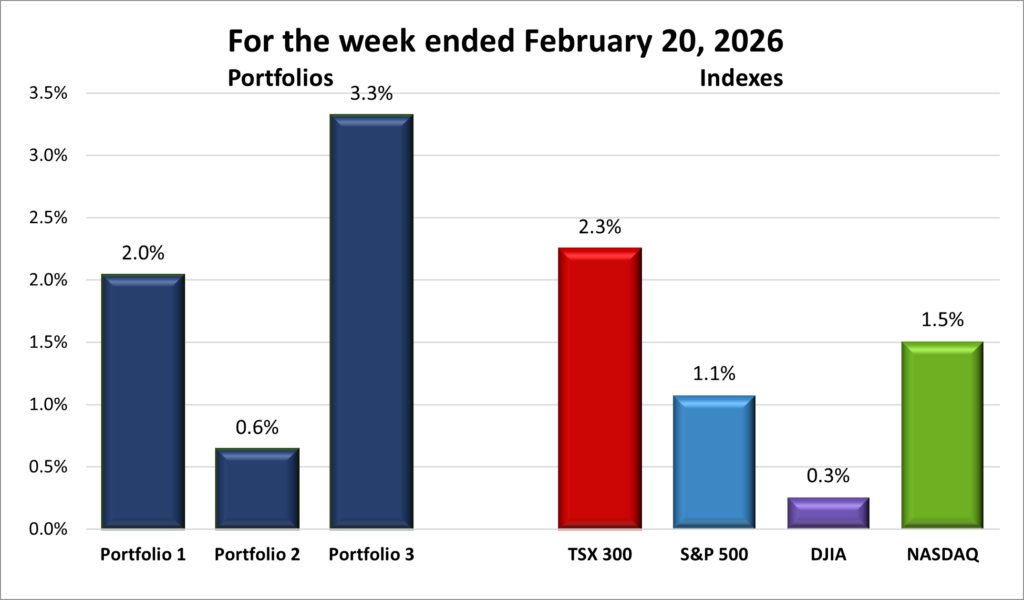

For the week, the TSX (SPTSX) surged 2.3%, the S&P 500 (SPX) gained 1.1%, the DJIA (INDU) rose 0.3% and the Nasdaq (CCMP) advanced 1.5%.

| Index | Weekly Streak |

| TSX: | 3 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() After a holiday-shortened week, markets turned in a mixed performance. The Toronto Stock Exchange Composite Index (TSX) stumbled early but went on to post three straight record-high closes, finishing as the top performer among the four major indexes. The S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all managed modest gains, but that was enough to snap each of their respective losing streaks and join the TSX in the win column.

After a holiday-shortened week, markets turned in a mixed performance. The Toronto Stock Exchange Composite Index (TSX) stumbled early but went on to post three straight record-high closes, finishing as the top performer among the four major indexes. The S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all managed modest gains, but that was enough to snap each of their respective losing streaks and join the TSX in the win column.

While it was a short week, there was plenty to move markets. For most of the week, three big themes drove trading: lingering AI uncertainty, the Fed’s January meeting minutes, and rising geopolitical tensions. On Friday, new economic data and the US Supreme Court ruling on President Trump’s tariffs, nudging investor sentiment higher even if they didn’t shape the week as a whole.

Investors continued to wrestle with big-picture AI questions. How disruptive will it be to existing business models? Will massive corporate AI spending translate into long-term profits? As those fears eased, AI-related stocks rebounded, including direct beneficiaries like Nvidia and companies that had previously sold off on concerns they could be disrupted.

Sentiment improved further after Nvidia (NASD: NVDA) announced a long-term agreement to supply Meta Platforms (NASD: META) with millions of AI chips and related infrastructure for its data centres. Given Nvidia’s outsized influence on market direction, the news reassured investors that AI spending remains very real. Still, the volatility beneath the surface suggested the market isn’t fully convinced the story is settled.

Midweek, the Fed’s January meeting minutes reminded investors that rate cuts are not imminent. While no hike was signalled, the decision to hold rates steady was not unanimous. Some were open to cuts if inflation continues to ease, while others want clearer proof that price pressures are firmly under control. A few sounded more hawkish than expected, noting that labour market concerns have faded and the Fed should focus on lowering inflation to their 2% target.

Just as markets regained their footing, geopolitical tensions resurfaced. Reports of rising tension between the US and Iran, along with a buildup of US forces in the region, pushed oil prices higher and nudged investors toward safe haven assets like gold.

Adding to the cautious tone, Walmart (NASD: WMT) delivered a guarded outlook during its earnings release. As America’s largest brick-and-mortar retailer, its results often serve as a read on consumer health. The softer guidance raised fresh questions about economic momentum and prompted another rotation away from higher-risk growth stocks.

To close out the week, economic data reinforced the idea that the economy is cooling but not cracking. Together, the data indicated economic growth is moderating, inflation is still sticky, and consumers are cautious. That combination strengthens the case for patience from the Fed, with rate cuts possible later in the year but far from guaranteed.

Trade policy briefly stole the spotlight as the Supreme Court struck down President Trump’s broad global tariffs, ruling that he overstepped his authority under emergency powers law. The decision reduced one near-term trade risk for investors, but uncertainty lingered as markets waited to see how the administration would respond.

In Canada, the TSX followed a similar early-week path as US markets, dipping as investors wrestled with AI uncertainty. As those fears eased, rising tensions between the US and Iran pushed gold and oil prices higher, giving Canada’s resource-heavy index a timely boost. Strength in energy and gold stocks helped propel the TSX to three consecutive record-high closes to end the week.

The index also benefited from its composition. With heavier weightings in financials, natural resources, and energy rather than high-growth technology, the TSX tends to hold up better when investors rotate toward more defensive or value-oriented sectors. This week was another clear example of that dynamic at work.

Meanwhile, the US Supreme Court’s decision to strike down President Trump’s broad global tariffs had limited direct impact on Canada, since most exports already fall under CUSMA protections. Still, it adds another layer of uncertainty to the evolving trade relationship between the two countries – something investors will continue to keep an eye on.

All told, the week reinforced a familiar story: growth is moderating, inflation remains sticky, and investors are navigating a mix of opportunity and uncertainty. While AI fears eased and the TSX set new highs, geopolitical developments, the Supreme Court ruling on tariffs, and interest rate guidance serve as reminders that markets can change quickly.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 3 – week winning streak |

| Portfolio 3: | 2 – week winning streak |

![]() I was relieved to see all three major indexes finish the week higher – especially the tech-heavy Nasdaq. Because all three portfolios lean into technology, a strong week for the Nasdaq usually bodes well for them too. After a stretch of volatility, it was encouraging to see all three back in the win column, with Nvidia’s gain helping lift Portfolios 1 and 3 by 2% or more.

I was relieved to see all three major indexes finish the week higher – especially the tech-heavy Nasdaq. Because all three portfolios lean into technology, a strong week for the Nasdaq usually bodes well for them too. After a stretch of volatility, it was encouraging to see all three back in the win column, with Nvidia’s gain helping lift Portfolios 1 and 3 by 2% or more.

Portfolio 1 snapped its five-week losing streak with a 2.0% gain. About 63% of its holdings finished the week higher, including standout moves from Shopify (TSE: SHOP), up 17%, and Kraken Robotics (TSXV: PNG), up 15%. It was a broad recovery across much of the portfolio.

Portfolio 2 trailed the others with a modest 0.5% gain, even though 60% of its holdings rose. Strength in oil prices helped lift energy names like South Bow (TSE: SOBO), which reached a new record high. This is a good reminder that even when most positions move higher, the size of those moves matters just as much as the percentage of winners.

Portfolio 3 delivered the strongest overall return of the three with a weekly increase in value of 3.3%, despite having the lowest percentage of weekly winners at 59% (not much lower than the others, I’ll admit 😊). The difference came down to position size – its two largest holdings, Nvidia advance and Shopify’s impressive 17% gain. When your biggest positions rise, they can carry the entire portfolio.

Next week will be an important one for the broader market – and for at least two of the three portfolios. Nvidia reports earnings, and expectations are elevated. Investors will be watching revenue growth and forward guidance closely, particularly around AI-driven data centre demand. A strong report could add momentum to both the technology sector and the overall market – not to mention give the portfolios a solid boost. A disappointing one, however, could quickly bring volatility back and pull those portfolios into the red. With Nvidia representing a significant position in two portfolios, I’m definitely hoping for a stellar report and outlook. 😊

Companies on the Radar

No new companies landed on my Radar List this week, which gave me time to revisit two of the smallest names I’m tracking: Napco Security Technologies, Inc. (NASD: NSSC), a small-cap (under US$2 billion), and Dutch Bros Inc. (NYSE: BROS), a mid-cap (under US$10 billion).

No new companies landed on my Radar List this week, which gave me time to revisit two of the smallest names I’m tracking: Napco Security Technologies, Inc. (NASD: NSSC), a small-cap (under US$2 billion), and Dutch Bros Inc. (NYSE: BROS), a mid-cap (under US$10 billion).

Going in, I assumed Napco would be the one to drop. Dutch Bros has been growing quickly, and expansion stories tend to be exciting. But the Deep Dive told a more balanced story.

First, the overall scores were closer than I expected. Napco came in at 83%, compared to 79% for Dutch Bros. That’s not a big gap, but it shows both businesses have strengths.

Second, Dutch Bros raised additional capital through secondary offerings since late 2024. The cash helped fund expansion and reduce debt, which can be a smart move. The trade-off, however, is dilution. Shares outstanding have increased more than 60% since the IPO. In simple terms, dilution means your ownership slice of the company shrinks unless you buy more shares.

Napco, on the other hand, had issues with its 2023 financial statements tied to inventory and cost of goods sold. The SEC investigation closed in early 2026 without further action, but “material weaknesses” in internal controls and related lawsuits are governance yellow flags that can’t be ignored.

Then there’s recent performance. Over five years, both stocks are up. Over the past year, Napco is up 74% while Dutch Bros is down 37%. Price alone doesn’t determine quality, but it does reflect how the market currently views each business.

In the end, the dilution combined with the recent downtrend tipped the scale for me. I’ve decided to remove Dutch Bros from my Radar List for now.

Napco stays on the list for now. The financial reporting issues are something I’ll look into more deeply. Sometimes a yellow flag turns out to be a temporary stumble. Other times, it reveals deeper cracks. That’s exactly why I do my Deep Dive Analysis – to uncover any skeletons in the closet and focus only on the best companies, the ones I’d be proud to own.

- Xylem Inc. (NYSE: XYL): This is a large American company that develops water technology focused on moving, treating, and managing water. Its products and services are used by utilities, industrial customers, and municipalities for everything from clean drinking water and wastewater treatment to flood control and leak detection. With aging water infrastructure and more frequent climate challenges like droughts and flooding, demand for Xylem’s solutions is still strong. The business offers exposure to long-term, essential infrastructure spending tied to water scarcity, sustainability, and smarter cities.

- GE Aerospace (NYSE: GE): This is the large American aviation and defence business that remained after General Electric split into three separate companies in 2024. It has been on a strong run thanks to high demand for commercial jet engines as global air travel continues to recover. The company focuses on aircraft propulsion systems and services for both commercial and military customers, and it’s also moving into drones. As a global leader in jet engines and aircraft systems, GE Aerospace offers exposure to long-term trends in travel, defence spending, and emerging aviation technology.

- Broadcom (NASD: AVGO): A large cap American company that sells semiconductors and software globally. It designs critical chips used in data centres, networking equipment, and broadband infrastructure, playing a behind-the-scenes role in cloud computing and AI. Broadcom also owns a growing enterprise software business following its acquisition of VMware, giving it exposure to both hardware and software spending tied to AI and cloud growth.

- Napco Security Technologies, Inc.: A small US company that provides security hardware and systems like smart locks, intrusion alarms, fire alarms, and access control solutions. It sells through a network of distributors and installers, and has been increasing its recurring service revenue – something investors usually like to see. As demand for security and smart home products grows, Napco has multiple avenues for expansion.

- Corning (NYSE: GLW): A large cap American company that is a leader in specialty glass, optical fiber, environmental technology, life sciences, and other specialty glasses. They have been the supplier of the glass used in Apples iPhones since 2007, and they are riding the tailwind of an AI-driven fiber optic boom.

- Lumentum Holdings (NASD: LITE): A large cap US-based optical technology company that makes key components used to move data at extremely high speeds across cloud and data-centre networks. Products like electro-absorption modulated lasers (EMLs) are seeing rising demand as AI workloads require faster and more efficient connections between servers. As large cloud providers continue ramping up AI infrastructure spending, Lumentum has emerged as a key beneficiary of this next wave of data and connectivity growth.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated February 20, 2026.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!