Trade Uncertainty Returns

Last week, the United States Supreme Court ruled that many of President Trump’s global tariffs were illegal. Within days, the White House announced a new 10% tariff on imports from all countries, with plans to raise it to 15%.

Here’s a simplified recap of how we got here – and the uncertainty it has created.

How we got here

At the start of his second term, President Trump launched an aggressive trade strategy aimed at shrinking trade deficits and pressuring countries like Canada, Mexico, and China into renegotiating terms. To move quickly, the administration relied on emergency powers under the International Emergency Economic Powers Act (IEEPA) and imposed broad tariffs on imports.

Businesses challenged the move, arguing that only Congress has the authority to impose sweeping tariffs. The case ultimately reached the Supreme Court.

On February 20, 2026, the Court ruled that the emergency law did not give the president the power to impose those broad tariffs. Most of the global tariffs introduced under that authority were invalidated.

Collections stopped. Refunds may follow. And trade arrangements negotiated under tariff pressure are now in question.

What’s still in place

Not all tariffs disappeared. Duties imposed under other trade laws – including measures tied to national security and unfair trade practices – remain.

For Canadians, that means certain tariffs on steel, aluminum, and other goods can still apply. Goods that qualify under the Canada–United States–Mexico Agreement (CUSMA) generally remain protected, but products that don’t meet its rules of origin can still face duties.

In other words, tariff risk hasn’t gone away – it’s simply being applied under different legal authorities.

The new 10%–15% tariffs

Rather than stepping back, the administration pivoted to a different legal tool that allows temporary tariffs of up to 15%. A 10% global tariff is now in place, with the possibility of it rising to 15%.

These tariffs are temporary by design, but they reinforce a key point: trade policy remains highly fluid.

What this really means for markets

For investors, the key takeaway isn’t the legal technicalities. It’s the uncertainty.

Companies now face:

- Old tariffs that remain in effect

- Newly introduced temporary tariffs

- Potential refunds tied to invalidated tariffs

- And the possibility of further changes ahead

That kind of unpredictability makes planning harder. Businesses don’t know what their input costs will look like six months from now. Manufacturers don’t know whether supply chains will need to shift again. Exporters don’t know how competitive their pricing will remain.

And when uncertainty rises, companies often delay capital spending, hiring, and expansion plans.

For investors, uncertainty tends to show up in a few ways:

- Increased volatility

- Short-term swings tied to headlines

- Pressure on sectors exposed to global trade

- Currency fluctuations (including potential impacts on the Canadian dollar)

This doesn’t automatically mean markets fall. But it does mean investor sentiment can shift suddenly.

For us long-term investors, moments like this are a reminder that policy risk is real. It can change quickly, and it’s largely outside of any single company’s control.

Businesses with strong balance sheets, diversified supply chains, and pricing power are generally better positioned to navigate environments like this. Others may feel more pressure if uncertainty lingers.

That’s the bigger story – not just tariffs, but the renewed unpredictability around global trade.

Now that we’re up to speed on this latest round of tariffs and the uncertainty surrounding trade policy, let’s turn to the other forces that shaped the markets this week.

Items that may only interest or educate me ….

When great is not good enough, Canadian Economic news, US Economic news ….

When Great Is Not Good Enough

Once again, investors’ eyes were on Nvidia as the company reported its fourth-quarter earnings. Widely viewed as the bellwether of the artificial intelligence (AI) industry, Nvidia was expected to show that demand for its advanced AI chips is still strong – and that it continues to benefit from massive spending by the largest technology companies.

The company delivered another impressive quarter, beating expectations on both revenue and earnings while providing guidance that came in above forecasts. Shares jumped in after-hours trading as investors reacted to the continued strength in AI demand.

By the next day, however, some of that enthusiasm faded. When a company sits at the centre of both the AI trade and major market indexes, “great” doesn’t always move the needle as expected. The issue wasn’t Nvidia’s fundamentals – they were solid – but rather that expectations were sky-high, many investors had already bought shares ahead of the report (positioning), and short-term trading activity to capitalize on small gains can amplify swings (short-term dynamics).

At the same time, the broader AI narrative is shifting. Investors aren’t just cheering growth; they’re weighing the disruption AI may bring across industries, including to Nvidia itself. Even outstanding results can trigger profit-taking if they don’t meaningfully raise the long-term ceiling. The mixed reaction highlights how excitement over AI growth is now balanced by caution over sustainability, valuation, and ripple effects across the market.

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Gross Domestic Product (GDP)

According to Statistics Canada, the economy grew 0.2% in December after being flat in November. On a year-over-year basis, GDP rose 1.0%, an improvement from November’s 0.6% pace. Beneath the surface, goods-producing industries edged up 0.2% for the month, helped by a 2.7% jump in utilities, while mining, quarrying, and oil and gas extraction declined 0.9%. Services-producing industries also rose 0.2%, with arts, entertainment, and recreation leading the gains.

Zooming out, the fourth quarter tells a softer story. The economy contracted at an annualized rate of 0.6%, weaker than expectations for flat growth and a sharp slowdown from the previous quarter’s expansion. The main drag came from businesses drawing down inventories – selling existing stock rather than producing new goods – which reduced overall output.

There were some brighter spots. Household spending improved, government investment increased, and exports showed modest gains late in the year. Still, full-year growth for 2025 came in at 1.7%, marking the slowest annual expansion since 2016 outside the pandemic period. Trade uncertainty and softer business investment weighed on momentum, setting a cautious tone for 2026.

For investors, this mixed GDP report sends an important signal. Modest monthly growth shows the economy isn’t stalling, but the quarterly contraction reminds us momentum has cooled. Slower growth often prompts speculation about what the BoC might do next. Weaker data can increase the odds of interest rate cuts, which tend to push stock prices higher, especially for rate-sensitive sectors. At the same time, prolonged slower growth can weigh on corporate earnings, causing stock prices to fall.

This report also highlights the ongoing debate about a “soft landing” versus a slowdown. A soft landing means the economy slows just enough to cool inflation without tipping into a recession. A slowdown (or mild recession) would see the economy contract for a longer period, which could hurt corporate profits and stock prices. Investors will be watching upcoming data closely to see which path Canada is likely to take.

Canadian Market Volatility

Canada’s “fear gauge,” the VIXC (tracked under the symbol VIXI.TS on many platforms), opened Monday at 15.90. Despite uncertainty surrounding the latest US tariff developments, volatility in Canadian markets remained relatively contained. As the week progressed, the index drifted lower, dipping to 14.49 as investors grew more comfortable and the TSX pushed to record highs.

On Friday, the gauge climbed back above 16 following the release of weaker-than-expected GDP data showing the economy contracted in the fourth quarter. After investors digested the report, volatility eased again, with the VIXC settling at 15.75 by week’s end.

Readings in the mid- to high teens typically signal caution rather than panic. The brief spike reflected investors reacting to softer economic data, while the pullback suggested those concerns remained contained. Canadian volatility often stays lower than US volatility because the TSX is more heavily weighted toward banks, energy, and materials – sectors that tend to be less sensitive to the sharp swings seen in high-growth US technology stocks.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer Confidence Index (CCI)

In February, the CCI rose to 91.2, up from an upwardly revised 89.0 in January, beating expectations for a smaller rebound. It marks the first uptick after sentiment slid to multi-year lows earlier in January and suggests a modest improvement in optimism among American households.

The Present Situation Index, which reflects views on current business conditions and the labour market, came in at 120.0. While still well above the headline index, it edged lower, hinting that confidence in today’s economic backdrop may be softening at the margin.

Meanwhile, the Expectations Index, which tracks the outlook for the next six months, rose to 72.0. That’s its highest level since July 2025 (74.4), but it remains below the widely watched 80 level that has historically signalled elevated recession risk when sustained.

After January’s sharp drop, February delivered a modest rebound. Present conditions are still relatively firmer – reflecting a still-solid labour market – but forward-looking expectations continue to show caution beneath the surface.

American Market Volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” opened the week at 20.49 as uncertainty over new US tariffs and ongoing concerns about AI-driven disruption unsettled investors. Volatility gradually eased as the week progressed, with the VIX dipping as low as 17.50. However, following Nvidia’s fourth-quarter earnings release, concerns about the sustainability of AI spending resurfaced, pushing the index back above 20 before it settled at 19.86 by week’s end.

Think of the VIX as the market’s pulse. Readings above 20 typically signal elevated caution. This week was a reminder of how quickly sentiment can shift – trade uncertainty and AI concerns pushed volatility higher, only for it to cool again as investors digested the latest news.

Weekly Market and Portfolio Review

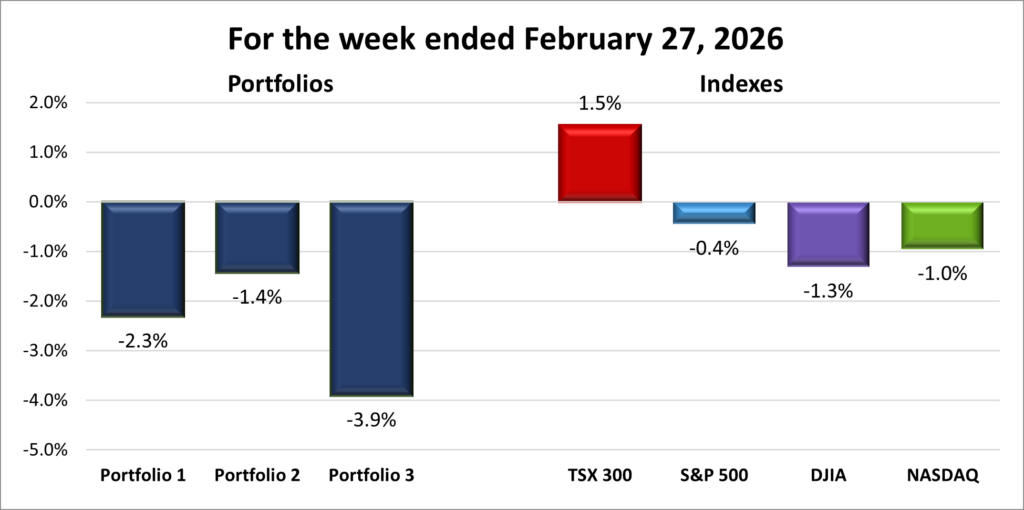

For the week, the TSX (SPTSX) rose 1.5%, the S&P 500 (SPX) fell 0.4%, the DJIA (INDU) dropped 1.3% and the Nasdaq (CCMP) lost 1.0%.

| Index | Weekly Streak |

| TSX: | 4 – week winning streak |

| S&P: | 1 – week losing streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 1 – week losing streak |

![]()

![]() The indexes stumbled out of the gate before finishing the week largely in the red. After a slow start, the Toronto Stock Exchange Composite Index (TSX) had a strong showing, stringing together three straight record-high closes before ending the week with a daily loss. South of the border, the three major US indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – took investors on a rollercoaster ride, swinging lower and higher throughout the week before ending in negative territory. For the blue-chip DJIA, it was its biggest weekly drop since mid-November 2025.

The indexes stumbled out of the gate before finishing the week largely in the red. After a slow start, the Toronto Stock Exchange Composite Index (TSX) had a strong showing, stringing together three straight record-high closes before ending the week with a daily loss. South of the border, the three major US indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – took investors on a rollercoaster ride, swinging lower and higher throughout the week before ending in negative territory. For the blue-chip DJIA, it was its biggest weekly drop since mid-November 2025.

Familiar forces drove the action: renewed trade uncertainty and shifting AI sentiment over costs and potential disruption. Earnings – particularly from Nvidia – and geopolitical tensions and economic news adding volatility to the markets.

The fallout from the Supreme Court’s decision striking down President Trump’s earlier tariffs didn’t calm markets; it simply introduced a new phase of uncertainty. Early in the week, US stocks fell sharply after the White House announced a temporary 15% tariff on all imports, despite recent trade agreements with several partners. For investors, it reinforced that trade policy remains fluid and unpredictable.

As the week progressed, attention shifted back to AI. Concerns initially resurfaced around disruption, with expensive consulting firms emerging as the latest potential casualties of automation. Increasingly, investors seem less focused on how much AI will cost and more on who it might displace.

Midweek, however, optimism returned. Technology and AI-related stocks rallied in the lead up Nvidia’s earnings, reflecting continued belief in Nvidia’s long-term opportunity.

Nvidia once again delivered impressive results and strong guidance. Shares initially surged in extended hour trading, but much of that enthusiasm faded the following day. The numbers weren’t the issue – expectations were. With so much capital flowing into AI infrastructure, investors are increasingly asking when that spending may slow and whether the broader AI investment cycle will ultimately justify current valuations.

To round out the week for the American indexes, add in higher-than-expected inflation data at the wholesale level, creating headwinds for those hoping for a rate cut in the near future. Not to mention, heightened tensions between Iran and the US after the two sides failed to reach an agreement on Iran’s nuclear capabilities.

In Canada, unlike US indexes, the TSX delivered a strong performance and pushed to record highs. After a modest dip to start the week, as investors reacted to trade uncertainty and pessimism toward technology stocks, buyers quickly stepped back in. Strong earnings from major Canadian banks, including better-than-expected results from TD Bank (TSE: TD) and Royal Bank of Canada (TSE: RY), helped fuel the advance and reinforced confidence in the domestic economy.

At the same time, commodity-linked sectors such as gold and oil provided additional support. Rising gold and other precious metal prices lifted mining stocks, while firmer crude oil prices helped energy producers. By week’s end, the TSX had bookended three straight record-high closes with losses to start and end the week. With financials, energy, and materials together representing roughly 60% of the index, strength in banks and commodities can have an outsized impact on overall performance and overcame AI disruption concerns. That dynamic was clearly on display this week, helping Canada’s benchmark post a weekly gain while its American counterparts took it on the chin.

Even with the week’s swings, AI remains at the centre of the market narrative – not just because demand for chips and infrastructure is strong, but because investors are debating who benefits and who gets disrupted. The opportunity is enormous, but so is the uncertainty. Volatility may dominate the headlines, but the larger structural themes are still unfolding. With that in mind, let’s see how this week’s moves impacted the three portfolios.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week losing streak |

| Portfolio 2: | 1 – week losing streak |

| Portfolio 3: | 1 – week losing streak |

![]() This wasn’t the kind of week you draw up when closing out a month. Trade headlines added noise, but it was AI fears – both around spending levels and disruption – that did most of the damage across my three portfolios. Midweek, things were still within striking distance of a positive finish. That changed quickly after Nvidia (NASD: NVDA) reported earnings. Even though the results were strong, the stock slid more than 8% for the week, and as the largest holding in Portfolios 1 and 3, that move alone had an outsized impact.

This wasn’t the kind of week you draw up when closing out a month. Trade headlines added noise, but it was AI fears – both around spending levels and disruption – that did most of the damage across my three portfolios. Midweek, things were still within striking distance of a positive finish. That changed quickly after Nvidia (NASD: NVDA) reported earnings. Even though the results were strong, the stock slid more than 8% for the week, and as the largest holding in Portfolios 1 and 3, that move alone had an outsized impact.

Portfolio 1 declined 2.3% on the week, despite 53% of its holdings finishing in positive territory. There were some bright spots – Magnite (NASD: MGNI) surged 13% – but weakness across several technology names, led by Nvidia, outweighed those gains.

Portfolio 2 saw its 3-week winning streak end with a loss of 1.4%, which in most weeks would be disappointing. This time, it was the “winner” by losing the least. About 57% of holdings posted gains. Strength in energy helped cushion the blow, with South Bow (TSE: SOBO) and TC Energy (TSE: TRP) both hitting all-time highs. Mitek Systems (NASD: MITK) also contributed with a solid 13% gain.

Portfolio 3 had the toughest week, sliding 3.9%, with only 36% of holdings advancing. Along with Nvidia’s pullback, Shopify (TSE: SHOP), the second largest holding, also lost ground, amplifying the pressure. On the positive side, Lithium Americas (TSE: LAC) and Magnite posted strong gains of 13% each, and Vertiv Holdings reached an all-time high.

It was a reminder of how quickly a portfolio can shift when a heavyweight like Nvidia moves. Even in weeks where more than half of holdings rise, concentration in a few key names can drive the overall result. AI disruption has been rattling the broader market – and this week, my portfolios were clearly disrupted. ☹

Companies on the Radar

This week, there were two changes to my Radar List. The first was the departure of Lumentum Holdings (NASD: LITE), the company that makes key components used to move data at extremely high speeds across cloud and data-centre networks. While I still find the business interesting, I simply like the other companies on the list better right now when weighing the risk-reward trade-off.

This week, there were two changes to my Radar List. The first was the departure of Lumentum Holdings (NASD: LITE), the company that makes key components used to move data at extremely high speeds across cloud and data-centre networks. While I still find the business interesting, I simply like the other companies on the list better right now when weighing the risk-reward trade-off.

The second change was the addition of 5N Plus Inc. (TSX: VNP). It’s a small-cap Canadian company that produces high-purity specialty metals and semiconductor materials used in space solar power, renewable energy, medical imaging, and electronics. Many of its products are mission-critical, requiring consistent quality and long-term supply. With exposure to space programs, clean energy, and strategic materials, 5N Plus operates in several niche but expanding markets where technical expertise creates competitive advantages.

It operates across several long-term growth themes, and that type of optionality – generating revenue from different industries – is something I like to see and has definitely piqued my interest.

After these changes, my radar list remains at six, including the five below:

- Xylem Inc. (NYSE: XYL): This is a large American company that develops water technology focused on moving, treating, and managing water. Its products and services are used by utilities, industrial customers, and municipalities for everything from clean drinking water and wastewater treatment to flood control and leak detection. With aging water infrastructure and more frequent climate challenges like droughts and flooding, demand for Xylem’s solutions is still strong. The business offers exposure to long-term, essential infrastructure spending tied to water scarcity, sustainability, and smarter cities.

- GE Aerospace (NYSE: GE): This is the large American aviation and defence business that remained after General Electric split into three separate companies in 2024. It has been on a strong run thanks to high demand for commercial jet engines as global air travel continues to recover. The company focuses on aircraft propulsion systems and services for both commercial and military customers, and it’s also moving into drones. As a global leader in jet engines and aircraft systems, GE Aerospace offers exposure to long-term trends in travel, defence spending, and emerging aviation technology.

- Broadcom (NASD: AVGO): A large cap American company that sells semiconductors and software globally. It designs critical chips used in data centres, networking equipment, and broadband infrastructure, playing a behind-the-scenes role in cloud computing and AI. Broadcom also owns a growing enterprise software business following its acquisition of VMware, giving it exposure to both hardware and software spending tied to AI and cloud growth.

- Napco Security Technologies, Inc. (NASD: NSSC): A small US company that provides security hardware and systems like smart locks, intrusion alarms, fire alarms, and access control solutions. It sells through a network of distributors and installers, and has been increasing its recurring service revenue – something investors usually like to see. As demand for security and smart home products grows, Napco has multiple avenues for expansion.

- Corning (NYSE: GLW): A large cap American company that is a leader in specialty glass, optical fiber, environmental technology, life sciences, and other specialty glasses. They have been the supplier of the glass used in Apples iPhones since 2007, and they are riding the tailwind of an AI-driven fiber optic boom.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated February 27, 2026.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!